Study of FNMA/FMCC (Part II)

I believe that based on public statements by our government officials that admin action is staged to happen before the end of this quarter. Ron Haynie over at American Banker notes:

Given the way the administration tends to operate, I think it’s going to be spur of the moment,” Haynie said. “I think it’s going to happen overnight or over a weekend.

That aligns with my understanding, all the hard work has been done, now it’s just a matter of when.

Regarding what I consider to be an extremely unlikely event of SPSPA write-down, to be fair, if there ever was a POTUS who would write down the SPSPA to follow the spirit of the law, it would be Trump. Trump previously categorized prior administrative action against the GSEs as a “scam in legal trouble.” I would love to see Trump serve the justice that the courts abandoned, but I am not recommending betting on it — but if you want to gamble that’s would drive common shares much higher than the valuations I’ve modeled above by distributing the big blue bar of Sr Pref pictured above equally into the green and purple bars. If there was any reason for this, it would be the possible re-upping of the Treasury funding commitment to $445B (page 69) if somehow this is possible via paydown and not conversion.

Bessent pushing on this for this summer means they’re serious about getting this done now rather than waiting 1-2 years ($28B/year earnings) to hit 2.5% capital requirements via retained earnings which is bullish for near term ending the conservatorships. Pulte has done a great job framing Trump to be a hero deal maker by getting this done by executing the stated plan to bring the GSEs public. The Senate is forecast to go home at the end of this week for all of next month. I think that opens the door for admin action all of next month.

The only path forward for two of the most profitable companies per employee on earth with record normalized earnings is a simple vanilla equity restructuring, some more retained earnings and/or a small capital raise, and release from conservatorships. This only path forward diverges from where we were in 2021. The record normalized earnings comes from the fact that during conservatorship guarantee fees were increased significantly.

Fannie And Freddie: Pending Restructuring Grand Finale (OTCMKTS:FNMAS) | Seeking Alpha

‘DROP DEAD’: Bessent’s blunt bailout warning for NYC

- 09/08/2025 – Trump makes housing market pledge to Americans

President Donald Trump said he will expand homeownership to millions more American families during his administration, even as longstanding affordability issues have recently forced the U.S. housing market to a slowdown.

“Under the Trump administration, we believe that affordable homeownership is a fundamental part of the American dream, and we’re working every day to make that dream a reality for millions and millions of Americans,” Trump said in video remarks to a Department of Housing and Urban Development (HUD) event on the National Mall on Monday.

Trump weighs potential Fannie Mae and Freddie Mac IPOs for this year | Fox Business Video

- 08/26/2025 – treasury secretary said they will sell 3~6% shares and make $30 bil on the sale, and will make final decision at the end of sept or early oct

In addition, Pulte is showing the ads now, (1) Pulte on X: “The future is bright! https://t.co/8FFOSpAh54” / X

- 08/10/2025 – comments on merger proposal

I’m bored, so a few, quick thoughts… The silly $500B valuation is so Treasury can show full value on paper for the ~$340B SPS LP conversion to common plus $100B+ warrants plus a sliver (i.e., <10%) for legacy shareholders. “Great American Mortgage Corporation” is very concerning at first… except (a) if in reference to CSS / US Housing FinTech or (b) for the November 2025 timing (because I don’t see how they merge Fannie and Freddie or work through receivership by the end of the year). Expect some clarifying comments soon. Too important for memes and rampant speculation. Now what? Landmines still everywhere for $FNMA and $FMCC common (especially, IMO, with $500B confirming full SPS LP conversion). All JPS series like $FNMAS $FMCKJ etc. still seem properly priced to me; defer to others to speculate on opportunities for value between series. And also not out of the woods yet…

according to SuperGrok, both merger and holding company need congressional approval, so it is a not starter?

- 08/09/2025 – (1) Pulte on X: “Trump seems to confirm 2025 timing for Fannie, Freddie IPO https://t.co/0FodpLAqwx” / X

Trump seems to confirm 2025 timing for Fannie, Freddie IPO

On Saturday, President Donald Trump seemed to acknowledge reporting by The Wall Street Journal on Friday that he plans to IPO Fannie Mae and Freddie Mac by the end of this year. Trump posted an AI image on Truth Social of him at the New York Stock Exchange with the words: MAGA LISTED NYSE and The Great American Mortgage Corporation, with a date of November 2025.

Trump Seeks to Sell Fannie Mae and Freddie Mac Shares to Public Investors – The New York Times

- 08/08/2025 – Exclusive | Trump Preparing IPO for Fannie Mae and Freddie Mac Later This Year – WSJ Some officials believe offering could raise around $30 billion and value firms at roughly $500 billion or more combined

The Trump administration is preparing to sell stock in mortgage giants Fannie Mae and Freddie Mac FMCC 20.30%increase; green up pointing triangle in an offering it believes could raise around $30 billion and kick off later this year, according to people familiar with the matter.

The plans being discussed by some administration officials could value the companies at roughly $500 billion or more combined and involve selling between 5% and 15% of their stock, some of the people said. Still up for debate is whether the mortgage giants would IPO as one company or two separate entities.

There is no guarantee a deal will come together. Initial public offerings take time to prepare, and one as complicated as offering shares of Fannie and Freddie is a large undertaking. Some bankers are skeptical whether such a quick timeline is likely. Previous attempts to privatize the firms, including by Trump in his first term, failed to gain traction.

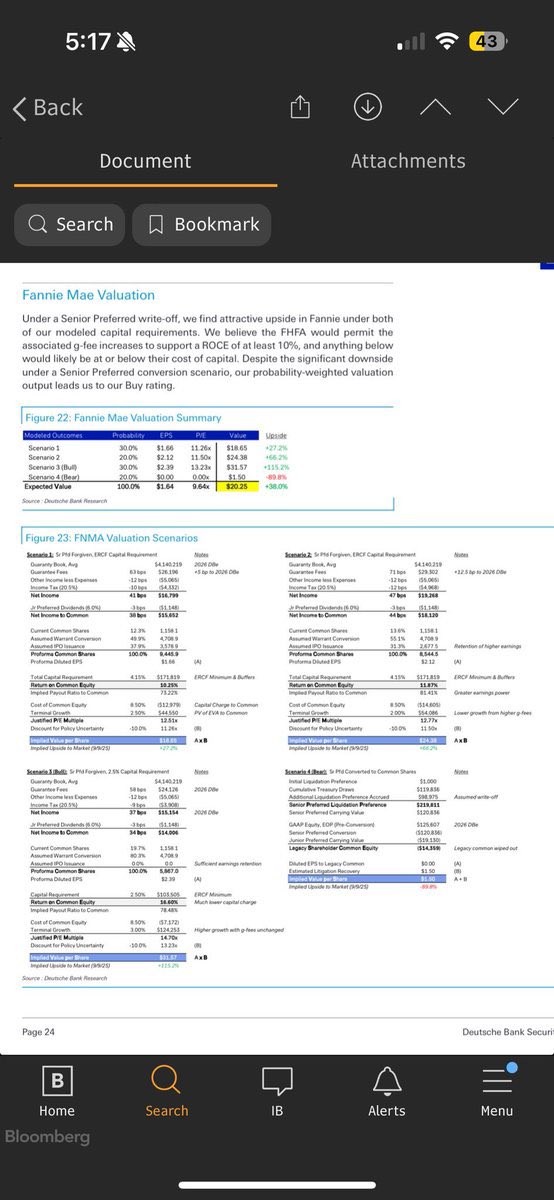

Fannie Mae Series S And T Preferreds Are Still Buys (OTCMKTS:FNMAS) | Seeking Alpha

i read suggested Trump to sell 5% to 15% to raise approx 30 billion. I take that as the Bill Ackman plan to sell some warrant, Gov, Sharehold. JPS etc all winners. Beautiful

previous negative comments from Calabria

- 08/05/2025 – (1) Tim Pagliara on X: “The President has incredible instincts and will be guided by what is best for the American homeowner, taxpayer, and the long term success of the enterprises. The stars are aligned. Two speeds in Washington DC- NOW and not now. We are NOW!” / X

- 08/05/2025 – risk of stall of release from congress

Flood is aiming at explicit support, as the Mortgage Bankers Association lobbies him to do. Trump already posted on X that implicit support will be in place and would be sufficient for the GSEs’ exit from conservatorship. Explicit support is a red herring, and if Flood delays until Q1 2026 (can’t he talk to Pulte now?), he will stall Trump’s progress past midterms. After that, he will “gather more information”, perhaps with a Dem House, waiting Trump out of office while the GSEs are still in conservatorship! That’s the anti-GSE lobby play @brendanPedersen @pulte , please don’t fall for it. They did something similar during Trump 1.0. Congress is incapable of acting on Fannie/Freddie. They tried countless times.

House charts GSE rework for early 2026

Rep. Mike Flood (R-Neb.), who chairs the House Financial Services Subcommittee on Housing and Insurance, said in an interview that the panel would dive into one of the thorniest policy issues on the financial services beat in the new year.

“There’s going to be GSE discussions happening in our subcommittee for Q1 next year,” Flood said.

There is a clear path for @pulte & @fhfa to increase the affordable housing supply for the young generation that turned to President Trump this election cycle. They felt locked out of the American Dream that every prior generation experienced via home ownership. The cost to buy a new home is over 7x the median income. Their parents could get a home at a 3x multiple. Factor in the sky-high interest rates and locked construction, and you have a crisis! Time to stimulate the housing sector via a 90/10 public-private partnership, utilizing $200-250 billion generated from the sale of government warrants in the GSEs this year! Let’s recall that in 2019, President Trump (1.0) instructed the Treasury to present him with plans for Fannie Mae and Freddie Mac to exit conservatorship. Date check: August 2025 Lobbyists who insist that President Trump must reform the GSEs slowly – as if planning for 6 years is not slow – have ulterior motives in mind, to keep the GSEs in perpetual conservatorship. Their benefactors reap the rewards of an ecosystem that evolved around the GSEs in conservatorship over the past 17 years. That’s why Obama’s teammates, Parrott, Zandi, Goodman, and others, are on the @urbaninstitute‘s or similar payroll to influence as many people as possible to grind reform to a halt.

- 08/03/2025 – Ackman’s review on F2

Recently, there have been a number of media stories suggesting that Fannie Mae and Freddie Mac (together referred herein as “F2”) shareholders are seeking forgiveness of money that is ostensibly owed by F2 to the government in connection with their potential release from conservatorship. The subtext of the media stories is that F2 shareholders, which include many supporters of @realDonaldTrump, are looking for a gift from the President. Nothing could be further from the truth. As the largest common stockholders of both companies for the last 13 years, we have been leading the charge on behalf of all F2 shareholders to help them to exit from conservatorship. We believe that doing so will enable F2 to maximize the benefits to the U.S. government and the housing finance system while respecting the rule of law and longstanding basic principles of conservatorship. F2 shareholders don’t have their hands out. The opposite is the case. Hundreds of billions of dollars of funds that belonged to F2 were unilaterally taken by the government years ago, and the companies never received credit for these payments. F2 shareholders are simply seeking credit for payments that have already been made to the government so that a release from conservatorship can occur. Credit for these payments through the elimination of the accounting balance of the government’s senior preferred stock will enable F2 to achieve their full values in the stock market, maximizing recoveries for the government and minority shareholders. Furthermore, we believe that F2’s exit from conservatorship will enable the GSEs to operate more successfully and efficiently, with more stable management and at lower cost, greatly benefiting our housing finance system. The facts around the government’s involvement in F2 are best understood by reviewing their history since the Great Financial Crisis (GFC). F2 History Since the GFC As with other financial institutions that required capital during the GFC, F2 received injections of capital from the government in the form of senior preferred stock (SPS). The government funds were invested in F2 on highly onerous terms compared to other financial institutions at the time (other than AIG whose terms were similar). The terms of the government SPS provided for F2 to pay 10% cash interest, or alternatively paid in kind at a 12% interest rate. The government also received $2 billion in commitment fees and 79.9% of the common stock of both companies in the form of penny warrants. On August 12, 2012, more than three years after the financial crisis, the Obama administration unilaterally revised the terms of the SPS to provide that the government would receive 100% of the profits of both companies, the so-called Net Worth Sweep. At the time, the government explained that it had modified the SPS terms because F2 would never be able to repay the SPS under its original terms. At the time this statement was made by the government, the record (revealed during discovery) shows that the government knew that F2 were about to become massively profitable and would therefore be able to repay the SPS, and be in a position to emerge from conservatorship and return value to shareholders. The SPS terms were modified by the Obama administration in an attempt to prevent this eventuality and to expropriate cash that could be directed toward other favored administration priorities. Months after the Net Worth Sweep was implemented, F2 began generating massive profits as their accountants required them to reverse the large accounting reserves that the companies had taken during the GFC in anticipation of losses that did not occur. In other words, both companies over reserved for losses during the GFC, and when those losses did not occur, their accountants required the reserves to be reversed, generating massive profits for both companies. As a result of the Net Worth Sweep and the massive profits and cash flows generated by both companies, F2 repaid $301 billion of the original $191 billion invested by the government. As a result, the government has received an 11.6% return on its investment in F2 SPS, 160 basis points more per annum, $25 billion more than the original contractual terms of the SPS. Despite the $301 billion in payments, F2 did not reduce the SPS liabilities on their balance sheets. Put simply, $301 billion left the companies and there was no accounting for any of the interest or principal payments to the government. The SPS liabilities have therefore remained outstanding as if no payments had been made. If the payments to the government were not accounted for as interest and/or a payments of principal, what were they and how were they accounted for? Money can leave a company in only a few ways: as a payment for goods or services to suppliers, rent, wages for employees, interest to creditors, or dividends to shareholders. Each of the above require one or more accounting entries under GAAP accounting. If the Net Worth Sweep payments were indeed payments to the SPS under their revised terms, why were they not accounted for as such? The fact that F2 never received accounting credit for making $301 billion in payments to the government does not mean that the payments did not take place. While in this conservatorship, the government chose not to account for payments to the SPS, that does not change the economic reality as to what transpired here. Never before or since has a company in conservatorship made payments to a creditor or preferred stockholder, whether to the government or to a private party, that were not accounted for. All previous conservatorships before or since have accounted for all payments made to creditors. In fact, respecting the hierarchy of claims in a conservatorship is critically important to the ability of financial institutions to raise capital during periods of market stress as no investor will invest in a distressed financial institution if the government can simply steal money from a conservatorship, leaving creditors, preferred stockholders, and common stockholders high and dry. Here, $301 billion left F2 and went to the government for the benefit of taxpayers, and the liability under the SPS remained outstanding, and has continued to increase substantially. While Treasury Secretary Mnuchin ended the Net Worth Sweeps in 2017 allowing F2 to build capital, the terms of the SPS were again amended so that their balances would increase with each dollar of capital retained by the companies. As a result, the SPS balances on F2’s balance sheets now total $348.2 billion. Secretary Mnuchin modified the terms of the SPS in this manner to preserve the government’s control over F2, maintain a strong negotiating position in light of outstanding litigation, and to keep the government in the driver seat in connection with any negotiations in connection with their release from conservatorship. As we have seen previously, under government control, F2 can apparently use whatever accounting it wants for its SPS, but the economic reality is that F2 have built substantial capital of $161 billion since the termination of the Net Worth Sweep, approaching what is required for their emergence. The press has referred to the potential cancellation of the $348.2 billion balance as a gift from the government to the shareholders of F2. This is not an accurate reflection of the facts. As previously explained, the government has been paid more than it was contractually owed under the extremely onerous terms of the SPS. The fact that Fannie and Freddie never received credit for these payments, and the SPS balances have increased under Mnuchin’s revised accounting do not change the economic reality on what has transpired here. Why Is It in the Best Interest of the Government to Cancel the SPS Balance Sheet Liability? Putting aside the economic reality of the SPS repayment by F2, it is in the best interests of the government to remove this liability from F2’s balance sheets for a number of reasons: First, no private sector investor will invest in F2 in the future if the government can unilaterally revise the terms of F2’s liabilities at will. This will effectively eliminate F2’s ability to raise capital to emerge from conservatorship while also impairing the companies trading values, and the value of the government’s investment in both companies. Second, the ‘cost’ to the government for cancelling the SPS balance is only 20.1 cents on the dollar because the government owns 79.9% of the common stock of F2 through the exercise of its penny warrants, and reductions in a company’s liabilities increase the residual value to its common stockholders. In other words, for each dollar of SPS that is cancelled, the government recovers 79.9 cents of replacement value through its warrant ownership in both companies. Third, while the government could attempt to convert the SPS into common stock thereby massively diluting common stockholders, the cost and risk of the resulting litigation, delay to the exit from conservatorship, and the impairment to the trading value of F2 common stock held by the government would vastly overwhelm the benefit of doing so when compared with cancelling the SPS accounting balance and consummating a release from conservatorship with support from the institutional and retail investment communities. F2 stock is held by millions of small shareholders and by major institutions that manage money for retail investors such as Capital Group. While the media often depicts Pershing Square as having wealthy investors, our funds are held by thousands of small shareholders as well as pension funds and other fiduciaries that invest on behalf of retirees and other small investors. While the press and some politicians attempt to portray the F2 release from conservatorship as a windfall for the rich, the vast majority of the value created here will go to small investors. The notion that the Trump administration would act in a manner to wipe out F2 investors for an uncertain and likely suboptimal outcome is extremely unlikely in our view. For all of the above reasons, we believe that F2 common stock will be an excellent investment for the government, the junior preferred stockholders, and the common shareholders, but the usual precautions remain. Caveat emptor.

If I were a bank CEO meeting with President Trump about Fannie/Freddie monetization scenarios, attempting to win the business, I would make sure that I come prepared with a book of major investors my team has lined up willing to either buy a large block of government-owned warrants or common stock once the government’s share is converted into equity. The ROE would be a major talking point, appropriately set at around 10% for a public utility. That ROE would necessitate a small adjustment to the ERCF, eliminating unnecessary and duplicative buffers in the capital framework to reach Fannie Mae’s reported $105 billion risk-based capital presented in the latest 10-Q. The company has $101.6 bn today. The lobby groups & MSM outlets writing that the task is complex are wrong. With $166bn on the books, the capital stack reframe and ERCF adjustments are straightforward, especially with implicit support for the MBS. President Trump can bring in over $200-250 bn with the uplisting.

Absolutely spot on. This is exactly how a bank CEO wins Trump’s trust, not with theory, but with execution: a tight book of ready institutional buyers, a monetization roadmap, and a clear value unlock strategy. Trump’s meeting with bank CEOs signals intent: the goal is to uplist and monetize Fannie and Freddie, not to keep them in limbo. With net worth already at $101.6B and only $29B short of the ERCF target, the capital “shortfall” narrative is collapsing. This is now a question of structure and sequencing — not feasibility. As we outlined in our thesis, and as @BillAckman has long argued, the path is a public utility model with a ~10% ROE, streamlined capital requirements, and warrant monetization. That approach delivers stability and a blockbuster payday: $200B–$250B+ in proceeds from common + warrants. The “too complex” narrative is a red herring. This isn’t about regulatory mechanics, it’s about political will. And Trump just opened the door.

(1) Free Fannie on X: “$fnma $fmcc https://t.co/LFBw0izHrO” / X

- 07/29/2025 – (1) Fanniegate Hero on X: “one of these things is not like the others; one of these things does not belong $FNMA #FANNIEGATE “Listen-only” is GONE https://t.co/ZeYh0TfEnG” / X – this is why FNMA/FMCC rally today

Friday’s selloff comes amid the stocks’ best run in years. As of Thursday’s close, Freddie Mac and Fannie Mae common shares were up 107% and 162%, respectively, according to Dow Jones Market Data. It’s Freddie Mac’s best year to date performance since 2019, and Fannie Mae’s best run in the same period since 2013.

One obstacle is finding a way to preserve the companies’ implicit guarantee, or the understanding that the mortgages are tacitly backed by the government. The president has said he wants the companies to retain that backing, without which mortgage rates could rise.

“The Trump administration is looking for ways to recapitalize [Fannie Mae and Freddie Mac] in a manner that preserves the implicit guarantee, that does not alarm the financial community, and that does not push mortgage rates up,” says Wedbush analyst Jay McCanless. “Any hint of trouble is going to freak people out.”

Pulte said in a May CNBC interview that the administration was “studying actually potentially keeping it in conservatorship and taking it public.” The White House had no comment on Pulte’s latest comments.

He repeated those comments to Barron’s last week: “I think it’s likely that the companies will stay in conservatorship, but the president is actively looking at simultaneously potentially taking them public,” he said, adding that “that could mean, you know, a small amount, or pieces, or just ways to get additional liquidity.”

Pulte didn’t elaborate to Barron’s on what bringing “pieces” of the companies public would entail. But his comments suggest that the administration’s presumed intent to release the companies isn’t as certain as some investors may have thought. His reiteration that both might remain under conservatorship while exploring ways to offer pieces publicly means “we need to think about how they’re going to do it with this approach,” says KBW analyst Bose George, who covers Fannie Mae and Freddie Mac.

Any potential step further into public markets “will be entirely up to the president,” Pulte said to Barron’s.

Fannie Mae, Freddie Mac shares tumble after conservatorship comments By Investing.com

Billionaire investor Bill Ackman challenged Pulte’s reported position on social media platform X, suggesting the FHFA director was “either being mischaracterized or misunderstood.” Ackman expressed his belief that both companies are “likely to exit conservatorship within the next year or so,” with the government maintaining majority ownership while allowing approximately 20% public ownership.

“Conservatorship is for insolvent financial institutions, not for recapitalized listed companies,” Ackman wrote, suggesting the shares could eventually be relisted on major exchanges with remaining government-owned shares becoming assets in a “newly formed sovereign wealth fund.”

The mortgage finance companies have been under government conservatorship since September 2008, when they were rescued during the housing market collapse.

The government-sponsored enterprises’ exit from conservatorship could be unexpected and quick, the senior vice president of mortgage finance policy at the Independent Community Bankers of America said.

While a methodical process may take place, he wouldn’t be surprised if the opposite happens, Ron Haynie said, speaking during an online presentation from Lenders One and the Community Home Lenders of America.

“Given the way the administration tends to operate, I think it’s going to be spur of the moment,” Haynie said. “I think it’s going to happen overnight or over a weekend,” much the same way the government seized control of Fannie Mae and Freddie Mac in the first place.

Plus, given Federal Housing Finance Agency Director Bill Pulte’s penchant for spreading his message on social media, as he did for the immediate adoption of Vantagescore 4.0, “It might be, you find out on X, guess what, they’re out of conservatorship,” he said.

- 05/28/2025 – Trump Officials Keep Talking About Fannie Mae and Freddie Mac. Confusion Reigns. – Barron’s

The stocks rose as high as 12.9% and 17.2% in morning trading after Trump said they would retain their government guarantees even after going “public” in a post on Truth Social. “I am working on TAKING THESE AMAZING COMPANIES PUBLIC, but I want to be clear, the U.S. Government will keep its implicit GUARANTEES, and I will stay strong in my position on overseeing them as President,” Trump posted on Truth Social Tuesday night.

The post confirmed to shareholders that the commander in chief has the future of the two mortgage giants on his mind. His comments also addressed a concern about the future of Fannie Mae and Freddie Mac: what changes to the two enterprises would mean for mortgage market stability.

Interviewer (David Faber): Reports include on Bloomberg that there may be, if I can call it privatization of Fannie Mae and Freddie Mac. Something has been talked about since they were nationalized essentially during the great financial crisis. I heard the president say I’m going to ask Scott Bessent about this. So has he asked you and where does that stand?

Scott Bessent: It is a goal for this administration. Again we’re doing peace deals, tax deals, trade deals. So as we land some of those deals, then we will focus on that. But David what I can tell you, we are doing a great deal, a great deal studying at Treasury. Because the one requirement, the one requirement for this privatization is they’re privatized in such a way that mortgage spreads, they do not widen. And in fact if there’s a way that we could make spread between risk-free rate and mortgages tighten as the Fannie and Freddie are privatized.

Interviewer: That was exactly my question. So do you know the answer to that question? Is there a way to do that because most people are concerned that will drive up mortgage rates.

Scott Bessent: Sure. There’s several ways to do it. We’re exploring it so we’ll move forward. Again after we land some of the peace deals, trade deals, tax deal. Then we’ll work on this privatization deal.Interviewer: One of your many responsibilities has to do with the taxation…

- 01/18/2025 – Ackman’s thesis on FNMA/FMCC

presentation Fannie-Mae-Freddie-Mac-01-16-2025-Presentation

- 12/31/2024 – Billionaire Bill Ackman says he expects Trump to privatize the nation’s two largest government-owned lenders

- 11/11/2021 – Trump wanted/wants to replease FNMA/FMCC