Study of Macro (Part VI)

- 05/16/2026 – (1) ⁿᵉʷˢ Barron Trump 🇺🇸 on X: “President Trump gave Iran chance after chance to make a deal peacefully, but they keep playing games, saying one thing privately and doing the opposite publicly while dragging everything out hoping America backs down. Now reports say the US military already has another wave of https://t.co/1sJdBSrdyP” / X

- 05/08/2026 – The AI reality distortion field has engulfed more than the Mag-7. Intel stock recently surpassed the all-time high set during the dot-com bubble in 2000. This isn’t because the company has overcome its strategic problems; it is floundering against Nvidia in graphical processing units, which drive AI, and against Taiwan Semiconductor Manufacturing Co. in making chips for outside customers. Rather, the central processing units in which Intel specializes are in big demand by data centers. A similar halo effect has lifted the entire chip sector, including Advanced Micro Devices, Micron Technology and Sandisk.

AI Is Distorting Practically Everything About the Economy – WSJ

- 04/22/2026 – Kevin Warsh Pitched a Case for Fed Interest-Rate Cuts. His Future Colleagues Are Skeptical. – WSJ

the upcoming Fed Chair probably will lower the rate

- 03/13/2026 – Israeli Officials Think Iran’s Regime Isn’t Likely to Fall Soon – WSJ the war on Iran might last a bit longer – Despite constant military pressure, security services have a strong grip on the streets, and protesters are afraid

- 02/01/2026 – How Fed Pick Warsh Survived Trump’s Ultimate Reality Show – WSJ

Wall Street Can’t Decide Whether Kevin Warsh Will Be a Friend or Foe – WSJ

Exclusive | Trump Jokes About Suing Warsh if He Doesn’t Lower Interest Rates – WSJ

Who Is Kevin Warsh, Trump’s Fed Chair Pick? – WSJ

Kevin Warsh Is the Right Choice for the Fed – WSJ

- 01/31/2026 – “The Dollar is Collapsing”……Is It? – ValuePlays

“Davidson” submits:

With panic in streets at some parts of the country, with massive fraud being committed and overlooked perhaps protected by politicians and global relationships in flux there are many forecast that the US$ is no longer the reserve currency it has been for many years. By my analysis this is all self-interested fluff designed to game politicly and personally.

“Davidson” submits:

Taking out the volatile Aircraft orders, Durable Goods continues to reflect decent economic expansion. This is as expected and investors should maintain a positive equities outlook.

Industrial Capacity continues to rise as does industrial Production, both revised higher. The standout is the PMI remaining below 50, now ~40mos mostly below 50, reflecting an intractable period of market pessimism. Even with the rises we have seen in selected industrial issues, I see a remarkable period still ahead of heady price movement once market pessimism converts to recognition of economic expansion.

- 01/25/2026 – Subs: Momentum vs Value – ValuePlays

You need to be a Value Investor at market lows but think like a Momentum Investor once a Bull Market moves to full swing. I use comparable market Pr/Sales levels as a guide to how far I may let any issue progress before suggesting cutting a position. Transdigm(TDG) hit 9x Pr/Sales a couple of years ago and appeared to have stalled. I suggested a full sale 2yrs+ ago.

Investing is always a balance of Momentum vs Value at any point in time. The art is to know your economic timeframes, know the limitations of management to produce financials, constantly keep track of what management says “they will do” vs what they in fact do, diversify and use your best judgement.

Thus far, all is good with at least 3yrs of economic expansion ahead of us. But, always be cognizant that market prices always reflect Momentum vs future value expectations and we need to be alert at all times.

- 01/20/2026 – ‘Big Short’ legend Michael Burry says AI bubble is doomed and Buffett proves it

- 01/13/2026 – Subs: Tariffs Explained

Subs: Tariffs Explained – ValuePlays

Howard Lutnick: How America Can Hit 6% GDP Growth in 2026 – YouTube

- 01/06/2026 – ‘The Big Short’ investor who predicted 2008 crisis reveals how Venezuela raid can shape markets

The seizure was a “shot across China’s bow,” Burry wrote, pointing to the loans worth billions of dollars China has made to Venezuela under its Belt and Road Initiative (BRI). The money was collateralized using future oil output, which is “now in U.S. hands,” Burry noted. The veteran investor wrote that Chinese stocks now strike him as “somewhat riskier. He listed Alibaba, Baidu, and other potential sanction targets “could be in for some volatility” if Beijing tries to escalate aggression in the South China Sea or Taiwan.

Burry also took note of the impact on Russia and its oil as well. “Putin’s jaw has to be on the floor,” he wrote after seeing what the U.S. did in “practically seconds” that Russia has been trying to do in Ukraine for years. Burry estimated that while it may take five to seven years, if the U.S. manages to increase oil output from Venezuela, it would undercut Russia’s income and influence. “Russia’s oil just became less important in the intermediate and long-term,” he wrote.

Industrial Production revised higher as was Manufacturing Capacity. The Dallas Fed continues to roll out revised economic series some with long-term revisions others ranging from a few months to several years. Even so, the economic picture remains one of expansion in the face of continued “Doubting-Thomases”. The opposite messages of Industrial Production(INDPRO) vs PMI continue with the former very positive and the latter devoid of hope. Capacity and Capacity Utilization are very positive with Utilization showing signs of an upturn in line with what is visible in Durable Goods.

- 11/24/2025 – watch out the warnings from Burry

Cassandra Unchained | Michael Burry | Substack

- 11/18/2025 – Davidson’s comment on macro

Construction Spending Rises – ValuePlays

“Davidson” submits:

Total Construction Spending turns higher in August as St Louis Fed releases begin to come out once again. The pop came from Public spend and Residential with Power related holding steady and Manufacturing down a little from its record highs but not weak.

- 11/13/2025 – watch out the move from Burry

- Management’s SEC registration.

- Burry posted on X that he’s “on to much better things” after betting against Nvidia and Palantir.

- The contrarian investor foreshadowed the decision, writing the “only winning move is not to play.”

Michael Burry of “The Big Short” fame has terminated Scion Asset

So, I bought 50,000 of these things for $1.84. Each of those things is 100 doodads. So I spent $9,200,000, Not $912,000,000.

Each of those doodads let me sell $PLTR at $50 in 2027. That was done last month. On to much better things Nov 25th.

- 11/10/2025 – My latest thoughts on artificial intelligence (part 1) | Stansberry Research – Tilson’s viewpoint on AI and economy

Some of the largest companies in the world are betting on this. Alphabet, Microsoft (MSFT), Amazon (AMZN), and Meta Platforms (META) are investing massive sums in AI. Take a look at these Bloomberg charts shared on social platform X, which show the explosion in their capital expenditure (“capex”) spending:

At first glance, such spending appears to be wildly excessive. But keep in mind that these four companies – and the U.S. tech sector overall – generate gobs of free cash flow (“FCF”).

Across the sector, capex as a percentage of FCF is much lower than it was at the peak of the Internet bubble a quarter century ago:

The level of spending as a percentage of GDP is also modest relative to other tech build-out booms:

Another reason the current boom is different from the telecom one in the late 1990s is that the infrastructure today – mainly consisting of Nvidia (NVDA) chips – is “fully utilized,” as market strategist Shay Boloor explains:

Here’s my friend and former colleague Enrique Abeyta’s response to this:

So will businesses pay up for AI, warranting the massive amounts – trending toward trillions of dollars in the coming years – being spent on it?

The answer will largely depend on the extent to which AI can replace humans. In other words, if businesses can use AI to reduce headcount – or grow without having to increase headcount – then they will pay a lot of money for AI.

- 11/04/2025 – ‘Big Short’ trader makes $1bn bet against AI boom

A US investor depicted in the film The Big Short has placed a significant bet against artificial intelligence (AI).

Michael Burry, who bet on a US housing market crash in the run-up to the 2007 crisis, has wagered $1.1bn (£840m) on falls in shares of chip-maker Nvidia and software company Palantir.

On Monday, he posted a chart titled “US tech capex [capital expenditure] growth is matching the tech bubble of 1999-2000” and another showing how growth in demand for cloud computing at major tech companies is slowing.

Mr Burry’s investment firm Scion Asset Management has bought “put” contracts covering $912m of shares in software company Palantir and $187m of shares in chip-maker Nvidia, according to analysis of the fund’s portfolio update by investment research platform Quiver Quantitative.

- 10/17/2025 – Davidson on current thoughts of macro

Subs: Current Thoughts – ValuePlays

The only thing I’d add to this is “crypto risk”. If you watch each of the last selloffs, Bitcoin get hits the first and the hardest. This is because it has 24/7/365 liquidity and in times of panic, is the first thing sold. Shorts sellers also know this and add to the drama.

A largest panic and selloff in crypto that lasts could easily bleed into stocks given the vast number of crypto holders out there now.

The US economy is in the early stages of a massive uplift due to the current government tariff policy. Capital is being returned into the US economy for manufacturing and basic industries i.e., steel, aluminum, energy and etc. This leads to building the necessary infrastructure and employment funded by those foreign businesses with a desire to sell their goods with their specific innovation in the US. Tariffs used this way are forcing every manufacturer to fall into merit-based production rather than rely on local tariff protection. This is a revolutionary process that forces individual innovation into the forefront of every addition to every country’s GDP.

For the US this process is likely to take at least 5yrs, likely longer, to garner the productive capacity that we have shifted overseas in past many decades. It is a rebalancing of individual country unique talents to use the tariff system in this fashion. Eventually tariffs will fall back to very low levels once trade balance is achieved based on merit-based compensation rather than selective government subsidy. Meanwhile, the US will regain the GDP associated with its own intellectual innovation that had been shipped overseas and lost to other nations basically for low labor and environmental costs.

Some of our suggested issues have already responded with significant price appreciation reflecting surprise revenue and profit growth. Some selling to rebalance the portfolios for issues yet to respond has been recommended. Yet, some with decent gains today, have such upside potential, i.e., Astronics(ATRO) , Cooper-Standard(CPS) and etc. that they make sense to continue to hold in the face of compelling price potential. ATRO and CPS each have decent potential to rise well over $100shr.

The eventual market top is very likely to be cut short by consumer delinquencies exceeding past thresholds signaling instability in consumer debt. Currently this is in my estimation at least 4yrts+ ahead.

Meanwhile very significant gains are yet ahead as retail sales rise to record levels.

“Davidson” submits:

The primary lead up to recessions has been consumer delinquencies rising to identifiable thresholds. The next Fed report is not till late Nov 2025. Meanwhile, the market in general has focused on the debt level and not the consumer’s ability to handle this debt. Delinquencies at all levels have been near historically comfortable levels for consumer. This report by JPMorgan confirms that over-leveraged consumers are not a threat to the economy. That is: No Recession In Sight!

Resilient consumers and small businesses lead to improved charge-off outlook, JPMorgan CFO says

Oct. 14, 2025 9:41 AM ETJPMorgan Chase & Co. (JPM) StockBy: Liz Kiesche, SA News Editor

“Consumer and small businesses remain resilient,” JPMorganChase (NYSE:JPM) Chief Financial Officer Jeremy Barnum said on the company’s Q3 earnings call.

Due to that resilience, the bank lowered its 2025 outlook for card charge-offs to ~3.3% from its prior guidance of ~3.6% as delinquency rates are coming in lower than the bank expected.

- 10/10/2025 – Trump Threatens Higher Tariffs on China Citing Restrictions on Rare-Earth Elements – WSJ President signals other possible economic countermeasures, adding there is no reason to meet with Xi at APEC summit

Stock Market Today: Trump Threatens ‘Massive’ China Tariffs; Dow Falls — Live Updates

U.S. stocks gave up their gains for the week Friday after President Trump posted on Truth Social that he may cancel a planned meeting with China’s president and that he is considering “a massive increase in tariffs” on Chinese products.

The Nasdaq was down around 2% and the Dow 1% after earlier rising fractionally. Trump wrote:

Some very strange things are happening in China! They are becoming very hostile, and sending letters to Countries throughout the World, that they want to impose Export Controls on each and every element of production having to do with Rare Earths, and virtually anything else they can think of, even if it’s not manufactured in China. Nobody has ever seen anything like this but, essentially, it would “clog” the Markets, and make life difficult for virtually every Country in the World, especially for China.

U.S. chip stocks were hit hard, with AMD falling 6% and Broadcom dropping 3%.

- 10/08/2025 – Tilson’s viewpoint on the stock market

Below is a new one – courtesy of the latest Week in Charts blog post from Creative Planning’s Charlie Bilello…

It shows that the dividend yield of the S&P 500 Index is close to the all-time low it reached in early 2000, at the peak of the dot-com bubble:

This looks ominous. But having lived (and run a hedge fund) through that period of total madness a quarter-century ago, I don’t think it’s the same today…

Yes, valuations are high… so investors should have modest expectations for stocks over the next five years

But there’s a huge difference: Earnings growth has supported the current run-up in the tech sector.

Take a look at the chart shared in this recent post on social platform X:

As the post notes regarding these charts:

Back in the late 1990s, the IT sector price shot up way faster than the earnings. Prices jumped almost 600%, while earnings only grew around 30%. That’s what people called the “irrational exuberance” period – prices disconnected completely from company fundamentals.

Now look at the current cycle on the right. Since the ChatGPT launch in late 2022, both the price and earnings curves have moved up together. Prices are up about 97%, but earnings have also climbed sharply, nearly 87%.

I’ve said it time and time again… If you own quality stocks or index/mutual funds, stay the course.

- 09/23/2025 – Powell speaks Tuesday to the Greater Providence Chamber of Commerce 2025 Economic Outlook Luncheon

Federal Reserve Chair Jerome Powell speaks on interest rates and the economy — 9/23/2025 – YouTube

Powell Describes Rates as ‘Modestly Restrictive,’ Keeping Door Open to Cuts – WSJ Fed chair warns ‘there is no risk-free path’ after officials cut rates last week

-

Chair Jerome Powell stated the Fed’s interest-rate stance remains “modestly restrictive” after a recent rate cut.

-

Powell noted that tariff increases are likely to cause one-time price increases, but added “a ‘one-time’ increase does not mean ‘all at once’”—saying the effect will likely be spread over several quarters.

-

A narrow majority of Fed officials projected at least two additional rate cuts this year, implying moves in October and December.

Fed Chief Powell says stock prices appear ‘fairly highly valued’ Federal Reserve Chair Jerome Powell on Tuesday noted that asset prices, a category that typically includes stocks and other risk instruments, are at elevated levels. Though Powell noted the lofty equity values, he said this is “not a time of elevated financial stability risks.”

Watch Fed Chair Jerome Powell speak live on interest rates and the economy

In his post-meeting news conference, Powell characterized the reduction as “risk management” as officials become more concerned with weakness in the labor market than the threat from inflation. Meeting participants indicated a likelihood of two more cuts this year followed by additional reductions in the next two years.

- 09/18/2025 – Trump’s Team Explores Government-Backed Manufacturing Boost – WSJ Discussions center on how to use money from a $550 billion fund to spur construction of factories and other infrastructure

- 09/17/2025 – FOMC meeting

LIVE | US Fed FOMC meeting: Watch Jerome Powell announce the US Fed rate decision | Trump – YouTube

- 09/10/2025 – Employment Flat – ValuePlays

“Davidson” submits:

The Establishment Survey rose 22,000 and the Household Survey rose 288,000. As illegal alien deportations, self or government induced, are numbered between 1-2mil individuals, employment has stalled. This can be clearly visualized in the chart. Government employment is declining as policy changes shrink the total DC govt employment. The rise in native-born employment is reported as rising but is hidden by the decreasing non-native exits. This should prove a multi-year impact and make these series by themselves unreliable regarding historical measures of economic activity.

The S&P 500 has never been this expensive, or more concentrated in fewer companies

- 08/31/2025 – (1) Joseph 💎✌️🪑🇺🇸 Tesla Long Term Investor on X: “It’s probably nothing. https://t.co/qDay7lQs8T” / X

The image shared by @ShrimpTeslaLong, featuring Donald Trump with a globe and the text “THE WORLD WILL SOON UNDERSTAND” and “NOTHING CAN STOP WHAT IS COMING,” aligns with a surge in cryptic political messaging, possibly tied to recent global tensions, as indicated by the Pentagon Pizza Index hitting DEFCON 1 on August 30, 2025, suggesting heightened military activity.

- 08/22/2025 – Fed Chair Powell Opens Path for Interest-Rate Cuts in Jackson Hole Speech – WSJ During his annual speech in Jackson Hole, Wyo., Fed Chair Jerome Powell discussed the potential for the central bank to cut interest rates.

- 08/22/2025 – be careful of the inflated market due to margin debt (2) StockMarket.News on X: “🚨 Margin debt just hit a fresh all-time high: $1.022 trillion. The market is on fire, but so is the leverage behind it. This is one of the most dangerous signals in the markets right now. ( a thread) https://t.co/DKdONd8QKD” / X

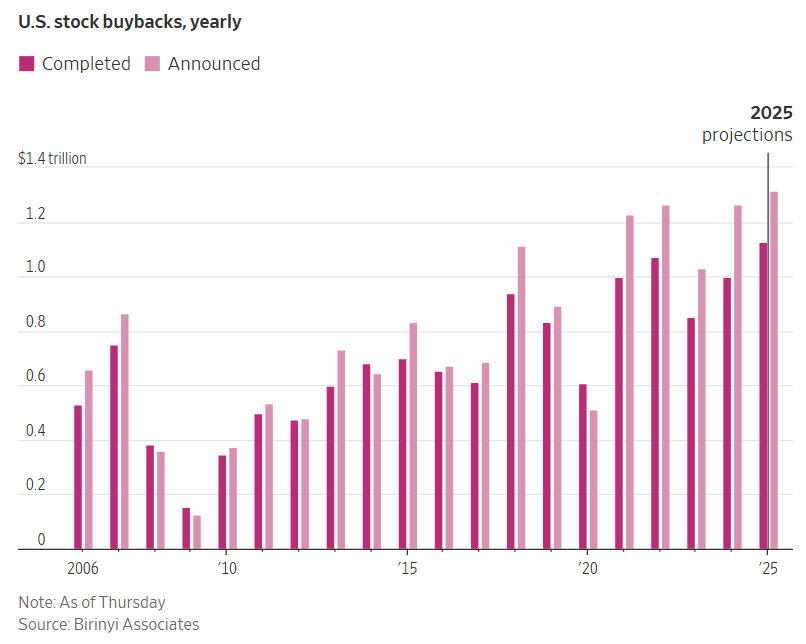

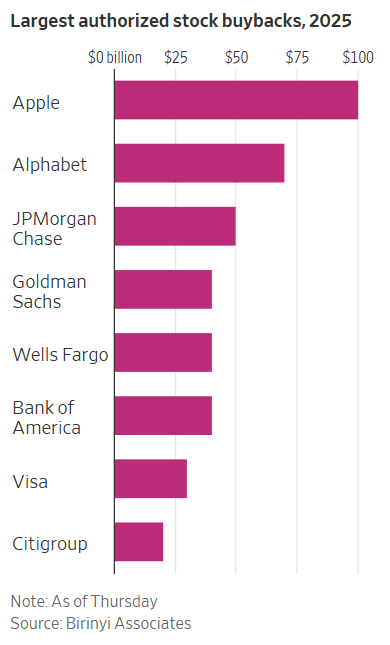

- 08/11/2025 – Corporate America’s Stock Buyback Spree: A Sign of Strength or a Red Flag? – WSJ Buybacks are expected to top $1.1 trillion in 2025, led by big banks and tech firms

-

American companies are on pace to repurchase over $1.1 trillion of their shares in 2025, an all-time high.

-

Tech giants such as Apple and Alphabet, plus big banks such as JPMorgan Chase, are leading the buyback charge.

-

Strong earnings and tax cuts are helping companies repurchase shares, while trade confusion stalls investments.

Strong earnings growth and tax cuts have helped fill corporate coffers, while powering stocks out of their tariff-driven April rout and lifting the S&P 500 and Nasdaq composite to fresh records. At the same time, the confusion around trade has stalled many businesses’ investment plans, making buybacks a more appealing use of incoming cash.

“Things are better than everyone makes them seem,” said Jeffrey Yale Rubin, president of Birinyi Associates. “Companies are flush with cash. They were in healthy shape even before the better earnings.”

- 08/08/2025 – Exclusive | Trump’s Team Expands Search for Fed Chair, Adding New Names to List – WSJ The president’s advisers are reviewing new contenders, including former St. Louis Fed President James Bullard and Marc Sumerlin, a former George W. Bush adviser

- 08/03/2025 – what could go wrong

- 08/02/2025 – it seems like Buffett is cautious on the current market

Berkshire’s Quarterly Earnings Drop on Insurance Results, Currency Moves – WSJ Warren Buffett’s conglomerate continued to stockpile cash and refrain from buybacks during market’s climb to record highs

- 08/01/2025 – Stock Market Today: Dow Falls 600 Points on Weak Jobs Report, New Trump Tariffs — Live Updates traders saw an 83% chance the Fed will cut rates at its next meeting in September

A weak jobs report and President Trump’s revamped tariff plan weighed on markets Friday, with investors ramping up bets that the Federal Reserve will now be more inclined to cut rates to support the economy.

Futures pricing Friday afternoon suggested traders saw an 83% chance the Fed will cut rates at its next meeting, according to CME Group data, up from 38% on Thursday.

- 07/31/2025 – Jobs Report Shows Hiring Slowed in July, With 73,000 New Jobs; Unemployment Ticks Up to 4.2% – WSJ

-

U.S. job growth slowed to 73,000 in July, below expectations, signaling potential labor market weakness.

-

The unemployment rate edged up to 4.2%, while revisions showed 258,000 fewer jobs added in prior months.

-

Economists debate the economy’s direction amid tariffs, immigration changes, and shifting consumer behavior.

- 07/30/2025 – The Fed – July 30-31, 2024 FOMC Meeting

Transcript of Chair Powell’s Press Conference — July 31, 2024

Fed Holds Rates Steady, but Two Officials Back a Cut – WSJ

Ahead of Wednesday’s decision, Trump said he thought the Fed would cut rates in September. Mr Trump had told reporters shortly before the Fed announcement that “I hear they’re going to do it in September.” However, Mr Powell said: “We have made no decisions about September. We don’t do that in advance.”

Powell deflected such speculation, leaving the Fed’s options wide open. He made no effort to tee up a September cut, even though he also wouldn’t rule it out. Expectations of a rate cut declined modestly on Wednesday. After the meeting, investors in interest-rate futures markets saw a roughly 45% chance of a September cut.

Powell and his colleagues are studying how tariffs filter through inflation data in the midst of anxiety that higher goods prices will keep inflation above the Fed’s 2% goal for a fifth year. Inflation has declined notably from 2021-23 highs without the recession many economists had predicted, but officials are cautious about declaring victory and possibly reigniting price pressures by cutting rates prematurely.

On the fiscal front, Trump signed a major tax cut package this month. Some Republican lawmakers are discussing consumer rebates that could add stimulus to an economy the central bank views as near full capacity—raising the odds Fed officials would regret cutting rates if the labor market remains steady.

The July meeting represented an initial fracturing of a Fed consensus to hold steady that emerged six months ago. The question that could further divide policymakers in the coming months is whether tariffs will damage the economy faster than they fuel inflation, and whether waiting for answers risks misjudging any course correction on either front.

The September decision could prove straightforward if the data breaks decisively in either direction. Sticky inflation readings alongside solid growth would make it easier to defer rate cuts, while clear economic deterioration would justify cutting. But if the current muddle persists, Powell faces more agonizing decisions.

- 07/29/2025 – Secretary Lutnick: Trade deals for ‘the world’ will be ‘done by Friday,’ but China will take longer | Watch – August 01 is the day for deal with the whole world, except China

- 07/27/2025 – Five Signs of a Market Bubble Investors Are Tracking – WSJ

- Speculative stocks like Opendoor and Kohl’s are surging, reminiscent of 2021’s meme stock frenzy.

- Crypto prices are rising, fueled by Trump administration policies and companies adding bitcoin to their balance sheets.

- Market breadth is improving and the economy remains strong, but stock valuations are stretched and the job market shows signs of weakening.

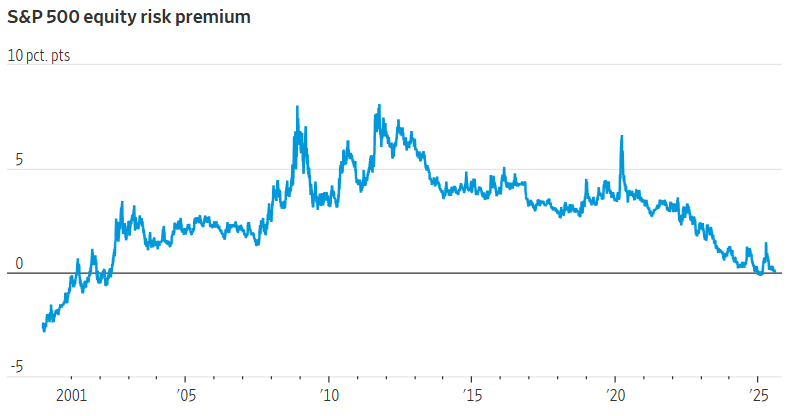

- stock valuations are stretched. The equity risk premium, defined as the gap between the S&P 500’s projected earnings yield and the yield on 10-year Treasurys, is close to zero. That means that the extra return for owning stocks over lower-risk bonds has nearly vanished, which investors consider an unhealthy sign.

- 04/16/2025 – Bessent on Trade Talks, Powell Future, Argentina, Dollar – YouTube – to look at whole picture tariff, tax and deregulation, do not only look at tariff

‘A UFC Battle Between China & US’ says Dan Ives

- 04/14/2025 – to be read The U.S. and China Are Going to Economic War—and Everyone Will Suffer – WSJ

Trump’s Trade Math Ignores a Major Export: American Services – WSJ

Nvidia to Produce Entirely U.S.-Made AI Supercomputers in Texas – WSJ

Humanoid Robots Are Lousy Co-Workers. China Wants to Be First to Change That. – WSJ

- 04/13/2025 – Trump Exempts Smartphones, Other Electronics From Chinese Tariffs – WSJ Announced in a filing late Friday, the move is a big reprieve for Apple and other tech companies

Smartphones, laptop computers, memory chips and other electronics will be exempt from President Trump’s so-called reciprocal tariffs, another step back that could ease some consumer concerns about an immediate jump in costs for tech products imported from China.

New guidance published late Friday by U.S. Customs and Border Protection also exempts machines used to create semiconductors, plus products including computer monitors, tablets, Apple watches and computers from the tariffs Trump imposed in his April 2 executive order, which mandated levies of 10% of the value of almost all U.S. imports, and set higher rates on imports from some countries. Trump later boosted the level of these reciprocal tariffs on China to 125%, and issued a 90-day pause on tariffs above 10% for other countries.

In all, 20 categories of products are affected. The biggest impact is on imports from China, because of the heights to which tariff rates had risen in recent days. In addition to the reciprocal tariffs, the Trump administration has imposed tariffs of 20% on Chinese imports over that nation’s role in the fentanyl trade, which the White House said aren’t subject to the exemptions.

“This represents a small step by the U.S. in correcting its erroneous unilateral approach,” said a statement from China’s ministry of commerce.

The exempted tech products accounted for roughly $100 billion in U.S. imports from China in 2024, according to Census Bureau data, or 23% of total imports from the country. Last year, 26% of all imports of the excluded products were from China—but 81% of smartphones and 78% of computer monitors came from there.

- 04/12/2025 – Buffett’s thought on tarriff from May 2018

Warren Buffett: There are levels of trade deficit that bother me “when you are, in effect, buying more from other countries than they’re buying from you, you are handing them investment funds” “we don’t want it to be a question of where we import 20% of our GDP and we export nothing. Now, we could all quit working, and we could handle little pieces of paper to the rest of the world. They could keep sending us food, they could send us autos, they could send us all kinds of things. But eventually, they have claims on all our wealth” Trust the process: short-term pain for long-term gain.

- 04/12/2025 – Wall Street’s Best Hope to End Trump’s Global Trade War Is One of Its Own – WSJ Treasury Secretary Scott Bessent, a former hedge-fund manager, is trying to execute one of highest-stakes gambles in modern political and economic history

Bessent gave a speech to the American Bankers Association telegraphing the Trump team’s new strategy. “We can probably reach a deal with our allies,” Bessent said. “And then we can approach China as a group.”

- 04/11/2025 – Ackman’s thought experiment

A thought experiment. Imagine if: Within the next 89 days, the US, Europe, and Japan agree to go zero/zero on tariffs and remove all trade barriers. Then Europe and Japan join the US in raising tariffs on China to 145%. Then the US, Europe and Japan as a united front negotiate with China to remove tariffs and trade barriers, and put in place strong structural protections for IP.

- 04/11/2025 – I need to fully understand the bond market and Trump’s decision

The Simple Explanation for This Week’s Treasury Market Mayhem – WSJ

We shouldn’t rely on markets to tame Trump – by Nate Silver

The Simple Explanation for This Week’s Treasury Market Mayhem – WSJ

The Death of US-China Trade || Peter Zeihan

- 04/11/2025 – Grannis’s take on Tariffs Calafia Beach Pundit To repeat what I said months ago, tariffs don’t cause inflation. Only monetary policy causes inflation.

I agree with what Bill Ackman said yesterday. By waiting until panic set in before announcing a reprieve, Trump forced the world to see first-hand what the results of a global tariff war would lead to. And he also put tremendous pressure on China, the biggest bad actor of global trade, to change its ways. It was a master-stroke of persuasion. Until yesterday I had begun to fear that Trump was making a huge mistake. Now my fears have been assuaged. We’re not out of the tariff woods yet, but the prospects for a favorable resolution have improved dramatically. Maybe those tariffs Trump threatened weren’t so bad after all, if they help the world understand how bad they can be.

Now let me comment briefly on today’s CPI release, which was a pleasant surprise. The chart below says it all:

Chart #1 compares the year over year change in the CPI index with the same change in the CPI index ex-shelter. The ex-shelter version of the CPI has increased by 2.3% or less for the past 23 months (since May 2023), and it has averaged a mere 1.7% per year for almost two years. In the past year, ex-shelter inflation was only 1.5%. Only shelter costs have kept the broader CPI from long ago meeting the Fed’s objective, and their impact is continuing to fade away. To repeat what I said months ago, tariffs don’t cause inflation. Only monetary policy causes inflation. So far the Fed has been doing a pretty good job of neutralizing the monetary excesses of 2020 and 2021.

- 04/11/2025 – Tilson’s take on Tariff I’m waiting for my ‘spidey sense’ to start tingling; President Trump is more concerned about interest rates and the bond market than the stock market; Nate Silver on why relying on the markets to ‘tame Trump’ is a mistake; Nobody seems to care much about the March inflation report | Stansberry Research

Most stock investors aren’t aware of this…

But the bond markets are much larger than stock markets – and bond investors are less tolerant of volatility and losses. So major financial crises (like the global financial crisis) generally occur when bond markets rather than stock markets break down.

This risk – and the rise in interest rates – is likely why President Donald Trump announced his 90-day tariff pause on Wednesday. Barry Ritholtz of Ritholtz Wealth Management posted this summary on social platform X yesterday:

And a thread on X from The Kobeissi Letter has more details. As it begins:

And as it continues:

Finally, as the thread concluded:

I will continue to follow interest rates and the bond market more closely than usual – and share it with my readers – because I think it will tell us what Trump is likely to do.

3) Meanwhile, statistician Nate Silver does a good job of analyzing why investors are still very much on edge in yesterday’s post in his Silver Bulletin blog: We shouldn’t rely on markets to tame Trump.

As Silver says, it comes down to investors trying to account for multiple degrees of uncertainty all at the same time:

1. The immediate effect of tariffs;

2. Second-order effects on consumer, business, and investor confidence;

3. Potential spillovers into broader financial markets – particularly the bond market, which had apparently spooked Trump, and

4. What the tariffs imply about Trump’s future actions and the United States’ overall state capacity.

As he puts it:

Investors are relying on a lot of implicit assumptions about an economic world order led by a relatively rational superpower – the United States – that may no longer hold.

And as Silver continues:

True, you’d rather have seen Trump capitulate [on Wednesday] than not. One remarkable feature of markets is that they provide a scoreboard – real-time feedback that even notoriously stubborn Silicon Valley types tend to take seriously. But considering those four buckets above, how secure should investors be feeling? Even with the 90-day pause, consumers and businesses will still be spooked by this and will experience higher prices from the tariffs that remain in place. The long-term effects on the United States’ cultural and financial hegemony are harder to quantify but potentially significant.

Markets and elites “got through” to Trump this time, but what if he wakes up on the wrong side of the bed 90 days from now and isn’t in such a generous mood? Not that I think headline writers should be catering to Trump’s mood swings, but triumphant headlines from Democrats about how Trump “surrendered” might give him second thoughts about doing the same thing next time around if he’s worried about looking like a loser.

In summary, fasten your seat belt… prepare for more volatility… and don’t obsess over the chaotic short-term news flow. Keep your eyes on the horizon.

4) Lost amid all the volatility in the stock market was the March inflation report the government released yesterday…

It showed lower-than-expected price gains, which normally would have made for bigger news. In fact, a month-over-month decline happened for the first time in nearly five years. Meanwhile, year-over-year inflation cooled to 2.4%.

But nobody really cares because of fears that tariffs will spike inflation going forward. Here’s the Wall Street Journal with more on this point: Inflation Eased in March, but Tariffs Threaten to Stoke Price Pressures. Excerpt:

Normally, a slowdown in year-over-year price increases would be welcome news for consumers, who have faced years of high inflation, and the Federal Reserve, which has been struggling to bring down price pressures. But this time, it will be hard for investors, policymakers and businesses to read too much into the March data.

President Trump’s “Liberation Day” announcement of sweeping new tariffs didn’t happen until April 2, which means their direct effects won’t show up until the next consumer-price report a month from now.

The article also cited this point from U.S. Bank Chief Economist Beth Ann Bovino: “It’s good news for the Fed, but the data seems stale.”

While the recent inflation numbers are indeed “stale,” the fact that both overall and core inflation are now below 3% gives the Fed more flexibility to cut rates to offset or at least mitigate a tariff-induced recession.

As a former hedge-fund-manager friend of mine – who posts anonymously on X under the handle BeenThereDoneThat Capital – posted yesterday:

On the plus side, my friend is right that the Fed now has room to cut rates to stimulate the economy if needed. (Investors are now expecting four rate cuts this year, up from one just a couple of months ago.)

But there’s a risk that if tariffs lead to higher inflation and an economic slowdown, the Fed’s cuts could fuel even greater inflation. This is yet another risk factor to monitor…

- 04/10/2025 – (1) Herbert Ong (@herbertong) / X(1) Herbert Ong on X: “🚨 NEWS: The E.U. Will Put Tariff Retaliation on Hold for 90 Days to Match Trump’s Pause European Commission President Ursula von der Leyen said that the commission, which handles trade for the bloc’s 27 member countries, “took note of the announcement by President Trump.” New https://t.co/5zg8FXQRUl” / X

The E.U. Will Put Tariff Retaliation on Hold for 90 Days | TIME

BRUSSELS — The European Union’s executive commission said Thursday it will put trade retaliation measures on hold for 90 days to match President Donald Trump’s pause on his sweeping new tariffs and leave room for a negotiated solution.

European Commission President Ursula von der Leyen said that the commission, which handles trade for the bloc’s 27 member countries, “took note of the announcement by President Trump.”

New tariffs on 20.9 billion euros ($23 billion) of US goods will be put on hold for 90 days because “we want to give negotiations a chance,” she said in a statement.

But she warned: “If negotiations are not satisfactory, our countermeasures will kick in.”

Trump imposed a 20% levy on goods from the EU as part of his onslaught of tariffs of 10% and upward against global trading partners but said Wednesday he will pause them for 90 days to give countries a chance to negotiate solutions to U.S. trade concerns.

Countries subject to the pause will face Trump’s 10% baseline tariff.

Before Trump’s announcement, EU member countries voted to approve a set of retaliatory tariffs on $23 billion in goods in response to his 25% tariffs on imported steel and aluminum that took effect in March. The EU, the largest trading partner of the U.S., described them as “unjustified and damaging.”

The EU tariffs were set to go into effect in stages, some on April 15 and others on May 15 and Dec. 1. The EU commission didn’t immediately provide a list of the goods.

Members of the EU — the world’s largest trading bloc — have said they prefer a negotiated deal to resolve a trade war that damages the economies on both sides. The bloc’s top trade official has shuttled between Brussels and Washington for weeks trying to head off a conflict. The EU has offered Trump a “zero for zero” deal in which both sides would eliminate tariffs on industrial goods including autos. Trump has said that’s not enough to answer U.S. concerns and raised the possibility of Europe buying large additional amounts of U.S. liquefied natural gas.

The EU has targeted smaller lists of goods in hopes of exerting political pressure and avoiding economic damage from a wider escalation of tit-for-tat tariffs.

The EU is also working on a further set of countermeasures in response to Trump’s blanket 20% tariff on all European goods, now suspended. That could include measures aimed at U.S. tech companies and the services sector as well as trade in goods.

Still, von der Leyen said that Europe intends to diversify its trade partnerships.

She said that the EU will continue “engaging with countries that account for 87% of global trade and share our commitment to a free and open exchange of goods, services, and ideas,” and to lift barriers to commerce inside its own single market.

BRUSSELS — The European Union’s executive commission said Thursday it will put trade retaliation measures on hold for 90 days to match President Donald Trump’s pause on his sweeping new tariffs and leave room for a negotiated solution.

European Commission President Ursula von der Leyen said that the commission, which handles trade for the bloc’s 27 member countries, “took note of the announcement by President Trump.”

New tariffs on 20.9 billion euros ($23 billion) of US goods will be put on hold for 90 days because “we want to give negotiations a chance,” she said in a statement.

- President Donald Trump announced a 90-day pause on the full effect of his new tariffs for at least some countries.

- Trump also said that he was raising the tariffs imposed on imports from China to 125% “effective immediately” due to the “lack of respect that China has shown to the World’s Markets.”

President Donald Trump on Wednesday announced a 90-day pause on the full effect of his new tariffs for at least some countries.

Trump also said that he was raising the tariffs imposed on imports from China to 125% “effective immediately” due to the “lack of respect that China has shown to the World’s Markets.”

Trump credited his decision to pause the full effect of tariffs on the fact that “more than 75 Countries” have contacted U.S. officials “to negotiate solution” to trade concerns that he raised in imposing the new duties.

- China is losing the trade war, should come to the table and talk with US

- Tax cut and deregulation are coming by May and June

- business leaders should feel certain by knowing tax cut and deregulation are coming