Recent learning from Michael Burry invest in anything he can have hand on – bio, REIT, banks (junked), AAPL, solar, retails. I should not be afraid to learn from anything that worth invest.

recent Burry’s portfolio return

Dr. Michael Burry surprised investors this year when he reported his first investment portfolio to the SEC since folding his previous fund in 2008 after he correctly predicted and made a large sum of money off the housing crisis, as portrayed in the movie The Big Short. He further surprised investors when that portfolio listed several of the banks that almost fell apart during the crisis, and even further when he sold all of the banks in the first quarter. Perhaps unsurprising is that almost every stock in his portfolio as of the first quarter is performing exceptionally.

As of March 31, Burry’s firm Scion Asset Management, junked positions in Citigroup (NYSE:C), Bank of New York Mellon (NYSE:BK), PNC Financial Services Group (NYSE:PNC) and Bank of American (NYSE:BAC) – the bank stocks he disclosed owning at the end of the fourth quarter. Burry founded the Cupertino, California-based firm in 2013, announcing ownership of 13 stocks at the end of 2015. He shrunk that to eight by the end of the first quarter.

Each of Burry’s bank stocks declined year to date by double digits, though it is unknown how long he has had the positions. They could have dampened returns in the first quarter, but their performance has been better since the start of 2013. From Dec. 31, 2012 to March 31, 2016, Bank of America stock rose roughly 21% and Citigroup 8%.

Apple (NASDAQ:AAPL) became the largest position in Burry’s portfolio at the end of the first quarter, though he had purchased no additional shares. He also started three new stock positions: health care provider NCA Holdings (NYSE:HCA), biotech Amgen (NASDAQ:AMGN) and auto Gentherm (NASDAQ:THRM).

Burry kept five stocks in his portfolio from the fourth to first quarter. Of those, three had sizable year-to-date gains, with Nexpoint Residential (NYSE:NXRT) posting the biggest return at 49%. NexPoint is a REIT with a $414.6 million market cap focused on multifamily properties in the Southeastern U.S. and Texas. It has a 4.2% forward dividend yield and pays a quarterly dividend of 20.6% per share. Burry at first quarter-end owned 609,905 shares of NexPoint, worth 15.6% of his portfolio.

The second best performer, Theravance Biopharma (NASDAQ:TBPH), returned 45% year to date. Burry owned 275,000 shares of the company, worth 10% of his portfolio. He also reduced the position by 37% in the first quarter.

Burry’s worst performer was First Solar (NASDAQ:FSLR), squeezed 26% year to date. He held 100,000 shares of the solar energy company, worth 13.4% of his portfolio at quarter-end.

Stocks Burry purchased in the second quarter have had weaker performance. From first quarter-end to date, Amgen’s stock price rose 11.7%. Gentherm declined 7.8% and Tailored Brands 17%, though Gentherm is a smaller holding at only 4% of the portfolio.

Returns for Burry’s portfolio stocks 2016:

Dr. Burry will release his portfolio showing his activity for the second quarter in the next several weeks.

Why Burry’s investment in Nexpoint Residential is good:

http://www.gurufocus.com/news/404672/michael-burry-bets-big-on-reit

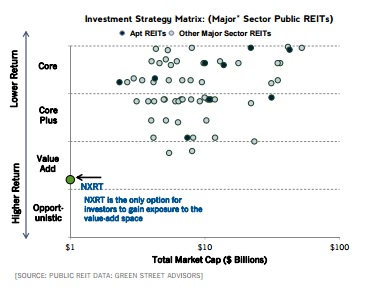

Curious what attracted Burry to the company, I went digging through the company’s materials on its investor relations site. Nexpoint is the only REIT in Burry’s portfolio, and Nexpoints claims to be the only REIT with a value-added strategy, which it claims generated ROI north of 20%.

The company focuses on residential real estate because declining home ownership and increasing student debt support the strong current demand for residential rentals. Meanwhile, new supply is only very slowly being added. According to the company, completions add under 2% per year to the existing stock until 2019 at least.

To achieve its ambitious return targets, management buys underperforming, under-capitalized properties and upgrades them in order to be able to raise the rents and extract market rates. The strategy probably doesn’t scale up without limitations, but given the company’s tiny market cap, it could have some runway left. Most of the value creation hasn’t taken place yet, to quote from the company’s presentation:

Current and Planned Value-Add: As of March 31, 2015, NXRT has planned to upgrade a total of 7,797 units of the 11,816 units owned* As of March 31, 2015, we have upgraded a total of 610 units Average cost per upgraded unit is $4,014 Average rent premium per upgraded unit: $83 Average return on investment: 24.6% (range: 13.9% – 41.1%)

One reason the company could be valued below its intrinsic value is because investors are overly fearful of the impact of the oil bust on the company’s risk profile. The company is associated with the Houston market, but the city actually makes up less than 2% of the company’s number of properties and contributes below 3% to NOI. The company actually views the oil bust as a net positive because it reduces risk as most of its tenants effectively received a tax cut.

From a valuation perspective, the company is a screaming buy if it is able to achieve anywhere near its ambitious return on investment goals. A company with such capable and ambitious management would deserve to trade at a multiple well-above book value, but in fact Nexpoint trades at a discount to net asset value, which the company estimates to be somewhere between $15.71 and $19.61 per share.

More materials in Burry,

https://apauperinthemidstofwealth.com/2015/10/26/dr-michael-burry-tips-tricks-and-case-studies/

http://streetcapitalist.com/2010/03/24/learning-from-michael-burry/

http://www.blogarama.com/blogs/578221-michael-burry-blog

Lessons learned from the above video,

- something seems unpredictable is meant to be, just need to think clear

- always ask questions when you are abnormalities, and always try to find the answers

- learn to work smart, not only work hard