Study of TSLA and TSLL (Part IV)

Here Grok’s take: – liability protection and risk isolation (similar to Google / Waymo) – regulatory and compliance flexibility (state-specific regulations, data privacy rules, insurance requirements, …) – fundraising and investment attraction (? doubt that) – operational and financial separation (distinct revenue stream, tax optimization, performance metrics) for focused management – antitrust and political considerations (could enable revenue sharing models and partnerships to avoid perceptions of monopoly)

- 08/08/2025 – Musk does not address when robotaxi will remove the safety monitors

(1) Cern Basher on X: “Could this be the version that allows the safety monitors to come out?” / X

- 08/08/2025 – Tesla Stock: Dojo Supercomputer Is No More As Elon Musk Shifts Chips Strategy| Investor’s Business Daily

Grok 4’s answer: If Tesla’s AI6 chip proves successful—meaning it meets or exceeds performance expectations for both inference (real-time AI processing in vehicles, robots, and edge devices) and training (model development in data centers)—the company could potentially reduce or eliminate its need for Nvidia chips over time. However, this outcome depends on several factors, including scalability, cost-effectiveness, and comparative efficiency against Nvidia’s offerings.Key Reasoning:

- Current Dependency on Nvidia: Tesla has historically relied heavily on Nvidia GPUs (e.g., H100 and H200 series) for AI training, spending billions annually to build massive compute clusters for Full Self-Driving (FSD) and Optimus robot development. This reliance grew after Tesla scrapped its in-house Dojo supercomputer project, which was originally designed to handle training workloads independently and reduce external chip needs. The pivot away from Dojo involves leaning more on Nvidia (and AMD) for immediate compute power, as the custom wafer-scale processors faced challenges like memory limitations, production delays, and high costs.

5 sources

This short-term increase in dependency is evident in recent reports, where Tesla is reallocating resources and staff from Dojo to other projects while sourcing external hardware.

- AI6’s Design and Potential Role: AI6 is Tesla’s next-generation custom AI chip, manufactured by Samsung under a $16.5 billion deal running through 2033, with production starting in Texas fabs using advanced 2nm processes.

5 sources

It builds on predecessors like AI4 (Samsung-made) and AI5 (TSMC-made, design recently completed), focusing primarily on inference for applications like autonomous driving, robotaxis, and humanoid robots (e.g., Optimus).

2 sourcesElon Musk has stated that AI5, AI6, and future iterations will be “excellent for inference and at least pretty good for training,” with all development efforts concentrated there.

2 sourcesThis converged architecture allows the same chip to serve edge devices (e.g., 1-2 chips per car) and data centers (e.g., 5-12 chips per server board).

- Path to Independence if Successful: Musk has suggested clustering multiple AI5/AI6 chips on boards to create supercomputer-like setups for training or inference, potentially dubbing it “Dojo 3.”2 sources

This could enable Tesla to build in-house training infrastructure, addressing Dojo’s original goal of reducing reliance on suppliers like Nvidia.3 sources

If AI6 delivers strong training performance (beyond “pretty good”) and scales efficiently—leveraging optimizations like frugal memory use, high parameter counts, and multimodal capabilities—Tesla could transition fully to its own ecosystem.2 sources

Musk’s emphasis on in-house chips aligns with broader aims to cut costs, avoid supply constraints, and control AI destiny, especially as inference demand grows industry-wide.2 sources - Caveats and Uncertainties: Success isn’t guaranteed; AI6 rollout is projected for 2027-2028, and timelines for FSD integration (e.g., by 2026) are aggressive.

2 sources

Even if effective, Tesla might retain Nvidia for specialized or overflow training needs, as “pretty good” implies it may not outperform Nvidia’s top-tier GPUs in all scenarios.

2 sourcesBroader market dynamics, like Nvidia’s dominance in AI training, could influence this.

Musk has noted that competitors’ reliance on Nvidia hardware alone won’t suffice for advanced autonomy, positioning Tesla’s integrated approach as superior.

In summary, AI6’s success could enable Tesla to become self-sufficient in AI hardware, phasing out Nvidia chips, but this would likely unfold gradually rather than immediately, starting with inference and extending to training via clustered deployments.

Grok4 explaination,

- The post suggests Tesla’s AI6 chip may prioritize low power consumption for use in cars and robots, limiting its training performance compared to NVIDIA’s B200, which benefits from higher power budgets in data centers; this aligns with a 2023 study in IEEE Transactions on Computers showing power constraints reduce AI chip training efficiency by up to 40% in mobile applications.

- Tesla’s shift from Dojo to AI5/AI6 chips, as noted by Elon Musk, reflects a strategic focus on inference optimization over in-house training solutions, supported by industry trends where companies like SiMa.ai raised $85 million in August 2025 to develop specialized edge AI chips.

- The claim of AI6 being underpowered for training challenges the narrative of Tesla’s self-sufficiency in AI hardware, with evidence from NVIDIA’s DGX B200 specs indicating a 15x inference and 3x training performance edge, highlighting a potential reliance on external compute providers.

[단독] 테슬라, 슈퍼컴 ‘도조’ 공급망 삼성·인텔 낙점 – ZDNet korea

Dojo didn’t flop. There would not be a tape out planned for Dojo 2 otherwise. There’s been a major paradigm shift in chip design and packaging driven by use of chiplets (think smaller chips integrated inside a package like Lego pieces). With this, a single chiplet could be used for inference with smaller memory – capable of running in a car. Multiple copies of the same chiplet slapped with high bandwidth memory and networking interfaces could be used for training, saving cost and complexity. Ultimately it’s the performance per dollar that needs to be maximized. In the dollar portion comes the design and tapeout costs. By reusing the same design for both, @Tesla is significantly reducing these costs. The cost of the inference chiplet is now amortized across the millions of cars running inference plus the hundreds of thousands of training nodes. So this is a smart move to reduce the TCO (total cost of ownership) for all necessary hardware. Btw – with this model, it’s quite possible that Dojo3 will be ahead on perf/$ versus NVidia even if raw training perf is slightly behind.

- 08/07/2025 – (1) Herbert Ong on X: “Morgan Stanley’s Adam Jonas says Tesla’s humanoid bots could replace 2 workers for $5/hour and drive robotaxi costs below $0.20/mile 🤯 “We estimate 1 humanoid robot at $5/hour can do the work of 2 humans at $25/hour, generating an NPV of ~$200k/humanoid. 1 robot car can” / X

- 08/07/2025 – (2) Pejjy on X: “Holy sheesh! Massive Robotaxi expansion is coming! $TSLA” / X

- 08/07/2025 – (2) Sawyer Merritt on X: “Trump tonight on Elon Musk: “I think he’s a good person; I believe that.” https://t.co/LRhPdF8ZvJ” / X

- 08/06/2025 – (1) Sawyer Merritt on X: “Elon on if investing $150k right now into $TSLA will make your millionaire in the future: “I think this is probably correct.” That would equate to a 566% return and make Tesla a $6.67 trillion company.” / X

(1) Elon Musk on X: “@GrindeOptions I think this is probably correct” / X

Uber CEO today on @Tesla: “They could be a competitor, they could be a partner. When you’re talking about trillion dollar TAMS, there will be no winner take all in this market place. It’s great to see Tesla in the market. They’re taking their time and making sure they are expanding in a safe way; All of this competition in autonomous is going to create safer streets and we’re going to be a big part of that.”

- 08/06/2025 – (1) Elon Musk on X: “Tesla is training a new FSD model with ~10X params and a big improvement to video compression loss. Probably ready for public release end of next month if testing goes well.” / X

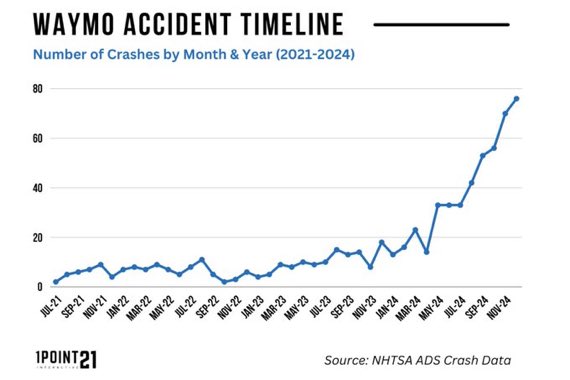

- 08/05/2025 – (1) *Walter Bloomberg on X: “$TSLA – TESLA, MUSK SUED OVER ROBOTAXI SAFETY RISKS Shareholders filed a lawsuit accusing Elon Musk and Tesla of securities fraud for hiding safety risks of Tesla’s self-driving tech, including the Robotaxi. The suit follows a late June test where Robotaxis were seen speeding,” / X

$TSLA – TESLA, MUSK SUED OVER ROBOTAXI SAFETY RISKS Shareholders filed a lawsuit accusing Elon Musk and Tesla of securities fraud for hiding safety risks of Tesla’s self-driving tech, including the Robotaxi. The suit follows a late June test where Robotaxis were seen speeding, braking suddenly, and making dangerous maneuvers. Tesla shares fell 6.1% after the test. Investors claim Tesla exaggerated the tech’s abilities, misleading the public and inflating its stock. The class action covers shareholders from April 2023 to June 2025.

PomLaw (Pomerantz LLP) filed this securities fraud class action lawsuit in the District Court for the Western District of Texas. – As this is not a derivative action lawsuit, they can ignore the 3% of outstanding shares requirement. – They have been active on other social media for weeks looking for “victims”, so this is no surprise. I so despise these organized money grabs. – PomLaw is the “master” (?) of class action law suits and their website shows currently more than 100 ongoing cases, including Apple (2x), Meta, Coinbase, Sanofi, Boeing, Zeekr, Hims & Hers, … Did the press make any fuss about any of these? Or is it just the Tesla name that triggers this sudden coverage?

- 08/05/2025 – 20T market valuation could be the comp package incoming (1) Ale𝕏andra Merz 🇺🇲 on X: “BREAKING: TESLA Pays Elon $29B – Here’s Why https://t.co/uswnLopsW8” / X

- 08/05/2025 – (1) Pejjy on X: “Question: Can another cunt with 9 shares sue Tesla for giving Elon 1/3 of his well deserved compensation since there is a case on this already?” / X

Why is the interim share grant not the full amount of shares that Elon Musk is 2018 Incentive plan? This is an interim measure and a first good faith step. – Tesla and shareholders are still fighting for the entirety of the 2018 plan owed and twice approved via shareholder votes. – The 96 million restricted shares are being issued under the 2019 Equity Inventive plan. (The 2019 Equity Incentive plan established a pool of authorized shares to incentive Tesla employees at the board’s sole discretion. It was voted on and approved by shareholders then. It replaced a 2010 plan). This plan had a maximum share limit and this is the max amount the Special Committee felt comfortable recommending allowing shares to be left for other employees too. => Expect another very important shareholder vote on the Proxy—a 2025 Equity Incentive Plan to authorize more Equity Incentive shares to attract and retain the best of the best talent for Tesla. And remember, a vote authorizing more employee equity as an incentive would likely be necessary even without this interim restricted share grant to Elon. There is an AI talent race and Tesla needs to maintain its position as the Real World AI leader. Please, all, ensure you can vote, this is going to be another historic shareholder meeting.

- 08/05/2025 – (1) Ale𝕏andra Merz 🇺🇲 on X: “my preferred SEC filing in a long time ❤️ https://t.co/wfxA0SJoC8” / X

- 08/04/2025 – this award as a first step, “good faith” payment to Elon. he Board (with Elon and Kimbal Musk recusing themselves), has unanimously approved a recommendation from the Special Committee of the Board to grant Elon an award of restricted stock equal to approximately one-third of the compensation he earned under the 2018 CEO Performance Award. In addition, The Special Committee continues our work to address a longer-term CEO compensation strategy, which we plan to put to a shareholder vote at the November 6 annual meeting.

Summary by Grok: Tesla’s Board approved a 2025 CEO Interim Award for Elon Musk: 96 million restricted stock shares (valued at ~$29-30B based on recent prices), vesting after 2 years if he stays in a leadership role. He must pay $23.34/share upon vesting and hold for 5 years. It’s a “good faith” partial payment tied to the disputed 2018 package, with no double-dipping if litigation resolves favorably. Aims to retain Musk amid AI/robotics push; accounting expense uncertain but potentially up to $23.7B. Impact on TSLA Stock Positive short-term: Removes compensation overhang, reinforces Musk’s commitment, lifting shares ~2.7% pre-market to $310.80. Long-term mixed: Boosts confidence in leadership stability, but ~3% share dilution and potential expense could pressure if growth stalls. Market sentiment upbeat, per analysts and X reactions.

related form 8-K sec.gov/Archives/edgar/data/1318605/000110465925073263/tm2522385d1_8k.htm

A Letter to Our Shareholders on the 2025 CEO Interim Award Dear Fellow Tesla Shareholders, Today we announce an important first step in compensating Elon Musk for his extraordinary work at Tesla. As you know, Elon has not received meaningful compensation for eight years since the 2012 CEO Performance Award was last earned in 2017. Despite overwhelming support from you in 2018 and again in 2024, our legal efforts continue in the Delaware courts to reinstate the 2018 CEO Performance Award. Despite these legal challenges, we can all agree that Elon has delivered the transformative and unprecedented growth that was required to earn all milestones of the 2018 CEO Performance Award. This growth has translated into immense value generated for Tesla and all our shareholders. To recognize what Elon has accomplished and the extraordinary value he delivered to Tesla and our shareholders, we believe we must take action to honor the bargain that was struck in 2018. After all, “a deal is a deal.” Thus, as evidence that Tesla is committed to honoring its promises in the 2018 CEO Performance Award and intends to compensate its CEO for his future services commensurate with his contributions to our company and shareholders, we have recommended this award as a first step, “good faith” payment to Elon. Delaware litigation continues to loom over us after seven years. As we told you last year, the 2018 CEO Performance Award resulted in a $2.3 billion stock-based compensation charge to Tesla but brought about $735 billion of increased market capitalization. Despite delivering such extraordinary returns, that award continues to be in legal limbo despite two separate shareholder votes supporting it by large margins. Furthermore, we have no clear timeline for resolution, as we are still waiting not only for a ruling, but a hearing date to be heard in front of the Delaware Supreme Court. Rewarding Elon for what he has done and continues to do for Tesla is the right thing to do. Retaining Elon Is More Important Than Ever Before Today, Tesla is at a critical inflection point that has the potential to create continued extraordinary value for you, the shareholders. Through Elon’s unique vision and leadership, Tesla is transitioning from its role as a leader in the electric vehicle and renewable energy industries to grow towards becoming a leader in AI, robotics and related services. To succeed, it requires a leader who combines strategic foresight, adaptability, and relentless execution to outperform competition and inspire the team. Elon has demonstrated these unmatched leadership abilities time and time again with his unparalleled track record of delivering shareholder value since he joined as a founding figure and spearheaded the transformation of our extraordinary company. And while these impending changes are exciting, the outcomes are not guaranteed. It is imperative to retain and motivate our extraordinary talent, beginning with Elon. The war for AI talent is intensifying, with recent months including multi-billion-dollar acquisitions of companies and nine-figure cash compensation packages for non-founder, individual AI engineers. Even among this group of highly talented individuals, no one matches Elon’s remarkable combination of leadership experience, technical expertise, and, arguably most importantly, decades-long proven track record of building the most revolutionary and profitable businesses across different industries. While we recognize that Elon’s business ventures, interests and other potential demands on his time and attention are extensive and wide-ranging, including his leadership roles at xAI, SpaceX, Neuralink, X Corp., and The Boring Company as well as his other interests, we are confident that this award will incentivize Elon to remain at Tesla and focus his unmatched leadership abilities on further creating shareholder value for Tesla shareholders and attracting and retaining talent at Tesla. To be clear, losing Elon would not only mean the loss of his talents but also the loss of a leader who is a magnet for hiring and retaining talent at Tesla. The Special Committee believes now is the right time to take decisive action to recognize the extraordinary value that Elon created for Tesla shareholders. As such, the Board (with Elon and Kimbal Musk recusing themselves), has unanimously approved a recommendation from the Special Committee of the Board to grant Elon an award of restricted stock equal to approximately one-third of the compensation he earned under the 2018 CEO Performance Award. The award provides the following provisions: • 96 million restricted shares of stock, subject to Elon paying a purchase price upon meeting a two-year vesting term, to be delivered after receipt of antitrust regulatory approval; • The purchase price will be equal to the split adjusted exercise price of the stock options awarded to Elon under the 2018 CEO Performance Award ($23.34 per share); • A requirement that Elon serve continuously in a senior leadership role at Tesla during the two-year vesting term; • A pledging allowance to cover tax payments or the purchase price; • A mandatory holding period of five years from the grant date, except to cover tax payments or the purchase price (with any sales for such purposes to be conducted through an orderly disposition in coordination with Tesla); and • If the Delaware courts fully reinstate the 2018 CEO Performance Award, this interim award will be forfeited or returned or a portion of the 2018 CEO Performance Award will be forfeited. To put it simply, there cannot be any “double dip.” Elon will not be able to keep this new award in addition to the options he will be awarded under the 2018 CEO Performance Award should the courts rule in our favor. The Special Committee, consisting of the two of us, was formed earlier this year to consider how best to retain and incentivize Elon in a manner that aligned with the best interests of the Company. The Special Committee and the Board deliberated carefully over the decision to grant this interim award against the backdrop of the ever-intensifying AI talent war and Tesla’s position at a critical inflection point. We believe it directly addresses a top concern and priority for shareholders and the Board alike: energizing and focusing Elon on Tesla so he can propel Tesla into its next era of growth, while we continue the legal campaign to have the 2018 CEO Performance Award reinstated. This interim award is structured to incrementally increase his voting rights upon grant, which he has repeatedly told us—and shareholders have confirmed—is an important part of incentivizing him to stay focused on the critical work we are doing here at Tesla. We believe this is a vital consideration, and we used the tools currently available to us—our existing equity incentive plan—to grant this award. We would also like to stress that prior to recommending this award, we reviewed your letters, read your X posts, and considered the direct feedback we have received from many of you in order to align our recommendation with your expressed views. From those communications, we know that one of your top concerns is keeping Elon’s energies focused on Tesla. This award is a critical first step toward achieving that goal, although it is limited by the capacity of our current equity incentive plan. As such, we are also working on next steps to address that issue. Still, while our work remains ongoing, we feel it is important to communicate directly and transparently with you all, our shareholders and Tesla’s owners. The Special Committee continues our work to address a longer-term CEO compensation strategy, which we plan to put to a shareholder vote at the November 6 annual meeting. Thank you for your continued support of Tesla and stay tuned for more information as we get closer to our shareholder meeting. Very truly yours, Robyn Denholm & Kathleen Wilson-Thompson Members of the Special Committee of the Board of Directors

- 08/03/2025 – good to know Musk is very cautious on roll out of robotaxi

Elon Musk on X: “@WholeMarsBlog One step at a time. Safety is paramount.” / X

(2) Elon Musk on X: “True” / X

E153 of The Cyber Bulls

00:00 Robotaxi Launch in CA 00:55 Ride-Hailing Analysis 03:04 Pricing & Competition 08:40 Tesla vs. Competitors 12:34 Autonomy Milestones 30:57 Stock & Market Impact 41:06 Samsung & LG Deals 50:09 Shareholder Meeting & xAI 54:40 Elon’s Compensation Plan 01:03:26 Rapid Fire: Cyber Cab & Stock

- 08/03/2025 – Tesla has quietly expanded its geofence territory in Austin!

- 08/03/2025 – Elon Musk Makes Tesla Investors SPEECHLESS AGAIN

Good discussion from Pejjy

Tesla might mix stock buyback, issue class A/B, etc methods to get 25% voting right for Elon Musk, otherwise, it becomes a big problem

- 08/02/2025 – here come the implication for tsla

25% of voting power to Elon? I doubt you can comment on this, @elonmusk, but trying anyway. After hours and days debating with Grok4 Heavy on options to get you asap to 25% of voting power, the conclusion is that Nasdaq rules (i.e. Rule 5640 below) will prevent Tesla from issuing super-voting shares (either by using the preferred shares we already have in the Texas Cert of Formation or by introducing Class B shares), as the IPO bylaws did not include them from the start. So our options are very limited: – negotiate with Nasdaq an exception (very unlikely to succeed) – tie everything to your next performance-based equity grants for the common stock we all hold (with the dilution that comes with it) – share buybacks to counter dilution (I don’t even dare write this, lol) – you purchasing Tesla stock (same) I feel we are stuck and this is very frustrating. Nasdaq text on the bottom here: listingcenter.nasdaq.com/rulebook/nasda

- 08/02/2025 – Royden D’Souza on X: “🧵1/2 🚨 ELON HEARD US!! @Tesla’s Optimus team is finally consulting hand surgeons – just like Gustav Andersson and Scott Walter said they should. Why the robot hand is half the problem… and maybe the whole answer. A masterclass with @anatomyumea and @GoingBallistic5 https://t.co/1AAohBxvOe” / X

- 08/02/2025 – Tesla will appeal

Sawyer Merritt on X: “Elon Musk says Tesla will appeal the ruling: https://t.co/fOjlC4KNUQ” / X

- 08/01/2025 – Elon Musk Gave Millions to Help Trump After His Epstein Bombshell. It seems like Elon Musk briefly tried to patch up his on again, off again bromance with President Donald Trump with $15 million in political donations following the pair’s spectacularly messy public divorce

- 08/01/2025 – (1) Sawyer Merritt on X: “NEWS: A jury has found Tesla partially liable for a fatal 2019 crash in Key Largo, Florida, and has ordered the company to pay $200 million in punitive damages. https://t.co/HeEr3nypyl” / X – Tesla probably will repeal

- 08/01/2025 – (2) Tesla Owners Silicon Valley on X: “Optimus robot is getting better at an insane rate. https://t.co/zBffECGbIy” / X

- 07/31/2025 – (2) Elon Musk on X: “@TeslaBoomerMama @teslaownersSV Just fyi I don’t have personal loans at this time against Tesla stock. Also, the taxes on the options are ~45%, so net gain in voting control is more like 4%. It is worrying in that I don’t want to build millions of robots and then potentially be ousted by activists and” / X

Breaking! .@robotaxi tests expanding to the following cities!! – Palo Alto, California – Brooklyn, New York – Houston, Texas – Farmer’s Branch, Texas – Tempe, Arizona – Henderson, Nevada – Tampa, Florida – Clermont, Florida – Miami, Florida

- 07/30/2025 – there is a consensus that Elon Musk might intend to talk down the stock price due to the coming of comp package and November vote

(1) Herbert Ong on X: “Elon’s Latest Moves Change Everything https://t.co/krROB46fAz” / X

- 07/30/2025 – (1) Joseph 💎✌️🪑🇺🇸 Tesla Long Term Investor on X: ““Launching Cybercab in Austin anytime in 2025” is a big big deal. Because it means no steering wheel and no safety monitor!! Extremely bullish.” / X

- 07/29/2025 – (1) 郭明錤 (Ming-Chi Kuo) on X: “For Elon Musk and Tesla, this represents a valuable opportunity to gain real-world foundry experience at an exceptionally low cost — something TSMC would never allow. It enables Tesla to enhance its chip design capabilities, particularly in manufacturability, while also gaining” / X

For Elon Musk and Tesla, this represents a valuable opportunity to gain real-world foundry experience at an exceptionally low cost — something TSMC would never allow. It enables Tesla to enhance its chip design capabilities, particularly in manufacturability, while also gaining deeper manufacturing knowledge, which will give them more leverage in future negotiations with foundries. In the long run, Elon Musk’s businesses will only demand more advanced chips, so acquiring core manufacturing expertise becomes a strategic advantage. Tesla’s AI6 chip is currently scheduled for mass production in 2027, using Samsung’s 2nm node (SF2). SF2 currently has a yield of 40–45%, lower than TSMC’s N2 (over 70%) and Intel’s 18A (50–55%). Elon Musk’s execution is proven, and SF2’s adoption of the same GAA technology as SF3 should facilitate mass production. Even so, it’s still difficult to predict whether Samsung can successfully ramp AI6 on SF2 as scheduled. If production falls short of expectations, the worst-case scenario for Tesla would be to shift the order back to TSMC and absorb the resulting delays to AI6.. However, Tesla’s edge in real-world AI could significantly reduce the risk of AI6 delays. Regardless, Tesla still gains from enhanced design capabilities and deeper chip manufacturing know-how. As for Samsung — with nothing to lose, why not give it a try? This partnership presents manageable downside and strong upside potential for both sides. If AI6 reaches mass production smoothly, chip design and manufacturing could become a core competitive advantage across Elon Musk’s businesses — enabling greater flexibility and lower costs. While Samsung may not fully catch up with TSMC in advanced nodes, it has at least discovered a new business model that actively involves customers in the manufacturing process.

- 07/29/2025 – (1) Mario Nawfal on X: “🇺🇸ELON “HAS A PHENOMENAL POSITION IN AI” Nvidia CEO Jensen Huang: “Elon has a great advantage because his AI factory for his cars is fantastic. He has a very large fleet of cars on the road… and he’s been working on this for a long time. Tesla is working on autonomous https://t.co/Yp5gzcAsHF” / X

- 07/29/205 – (1) Ben X on X: “特斯拉2季度业绩非常拉跨,纯的电动车,已经卷不动了。好在,马斯克早就决定要转型成现实世界的AI公司,做自动驾驶Robotaxi和机器人Optimus。基于10年的积累➕持续的盈利➕360亿美元的现金储备➕马斯克的执行力,这个转型在理论上没有悬念。但,还有一个重大卡点要解决,那就是马斯克的控制权。这个问 https://t.co/mh8VorqCTi” / X

- 07/28/2025 – Trump and Musk’s relationship is improving

President Trump’s State Department has announced it is coming to the defense of Elon Musk’s X after France labeled it an organized crime group and opened a criminal investigation. The State Department’s DLR stated, “As part of a criminal investigation, an activist French prosecutor is requesting information on X’s proprietary algorithm and has classified X as an “organized crime group.” Democratic governments should allow all voices to be heard, not silence speech they dislike. The United States will defend the free speech of all Americans against acts of foreign censorship.”

- 07/28/2025 – (2) Brett Winton on X: “every moving machine will require an inference chip, and the capability of that machine will be governed by the integrated capability of that chip” / X

- 07/28/2025 – (2) Elon Musk on X: “Samsung’s giant new Texas fab will be dedicated to making Tesla’s next-generation AI6 chip. The strategic importance of this is hard to overstate. Samsung currently makes AI4. TSMC will make AI5, which just finished design, initially in Taiwan and then Arizona.” / X

- 07/28/2025 – Tesla has signed a $16.5 billion deal with Samsung to produce Tesla’s AI6 (HW6) chips in Texas

Samsung will dedicate the Texas fab for Tesla’s AI6. This signals big volumes. AI6 is the convergence architecture: -AI6 for the data center for training and inference -AI6 for Robotaxi/FSD inference -AI6 for Optimus inference AI6 will likely be produced in two configurations: a system-on-wafer variant for Dojo (e.g., 5×5 tile array), and single-die versions for inference at the edge, powering FSD and Optimus.

Musk replied: Likely much more than that

This is Samsung’s new $25 billion semiconductor fabrication facility in Texas that will produce @Tesla ‘s future AI6 (HW6) chip. The facility is a 40 minute drive from Tesla’s Giga Texas factory. Tesla just signed a new $16.5B deal with Samsung to produce these chips, but Elon Musk says that number is “just the bare minimum. Actual output is likely to be several times higher.” Various Tesla products such as their cars and their Optimus robot will use this AI6 chip. This new Samsung facility is expected to be operational in 2026. Note: This drone footage is from August 2024, which is the most recent I could find (from Central Texas Aerials).

Grok interpolation of the above post –

- The post speculates that Tesla’s collaboration with Samsung on the AI6 chip could mark the beginning of Tesla developing a general-purpose AI chip line, similar to NVIDIA’s evolution from graphics to AI, potentially expanding Tesla’s influence in the semiconductor industry beyond automotive applications.

- This speculation is informed by the context of Samsung’s new $25 billion semiconductor facility in Texas, dedicated to producing Tesla’s AI6 chips, which are intended for various Tesla products including cars and the Optimus robot, indicating a strategic move towards broader AI capabilities.

- The idea is supported by the historical precedent of NVIDIA’s transition, suggesting that Tesla’s involvement in chip design and manufacturing efficiency, as mentioned by Elon Musk, could lead to innovative advancements in AI technology, challenging existing market dynamics and potentially reshaping the landscape of AI computing.

Tesla’s strategic move towards broader AI capabilities is a multifaceted approach aimed at leveraging artificial intelligence across its product ecosystem, particularly in autonomous driving, robotics, and energy solutions. This strategy is evident in several key areas:

1. Development of Full Self-Driving (FSD) Technology

- Tesla has been aggressively pursuing autonomous driving technology, with its FSD software being a cornerstone of its AI strategy. The company collects vast amounts of data from its fleet of vehicles, which are equipped with cameras and sensors, to train its neural networks. This data-driven approach allows Tesla to continuously improve its FSD capabilities.

- The recent announcement of the AI6 chip, to be produced by Samsung, is a critical component of this strategy. The AI6 chip, designed for enhanced AI processing, will power Tesla’s vehicles, enabling more sophisticated autonomous driving features.

2. Collaboration with Samsung for Semiconductor Production

- Tesla’s partnership with Samsung to produce the AI6 chip at a new $25 billion facility in Texas is a significant strategic move. This collaboration not only ensures a steady supply of advanced semiconductors but also positions Tesla to influence the design and efficiency of these chips.

- Elon Musk’s involvement in maximizing manufacturing efficiency at the Samsung facility suggests a deeper integration of Tesla’s AI expertise into the production process, potentially leading to innovations that benefit Tesla’s broader AI initiatives.

3. Expansion into Robotics with Optimus

- Tesla’s development of the Optimus robot, a general-purpose humanoid robot, is another facet of its AI strategy. Optimus is intended to perform a wide range of tasks, from factory work to household chores, and will utilize the AI6 chip for its operations.

- This move into robotics expands Tesla’s AI applications beyond vehicles, tapping into new markets and reinforcing its position as a leader in AI technology.

4. Integration of AI Across Product Lines

- Tesla is not limiting its AI capabilities to just vehicles and robots. The company is also integrating AI into its energy solutions, such as the Powerwall and Megapack, to optimize energy storage and distribution.

- This holistic approach ensures that AI is a unifying technology across Tesla’s diverse product offerings, enhancing efficiency and functionality in each area.

5. Data Collection and Neural Network Training

- Tesla’s strategy heavily relies on its ability to collect and process large datasets. The company’s vehicles act as mobile data centers, gathering real-world driving data that is used to train its AI models.

- This continuous learning loop is crucial for improving the performance of Tesla’s AI systems, making them more adaptive and capable over time.

6. Strategic Positioning in the AI Market

- By investing in its own AI hardware (AI6 chip) and software (FSD, Optimus), Tesla is positioning itself as a competitor in the broader AI market, similar to how NVIDIA transitioned from graphics to AI.

- This move could lead to Tesla developing a general-purpose AI chip line, potentially challenging established players and opening new revenue streams.

7. Geographic and Operational Synergies

- The proximity of the Samsung facility to Tesla’s Giga Texas factory (a 40-minute drive) facilitates logistical and operational synergies, reducing latency in chip supply and integration.

- This strategic location also aligns with Tesla’s goal of scaling production efficiently, ensuring that AI capabilities can be rapidly deployed across its manufacturing and product development processes.

Conclusion – Tesla’s strategic move towards broader AI capabilities is characterized by a combination of hardware development (AI6 chip), software advancement (FSD, Optimus), and data-driven innovation. By collaborating with Samsung and expanding into robotics and energy solutions, Tesla is not only enhancing its current products but also positioning itself as a key player in the future of AI technology. This approach mirrors NVIDIA’s successful transition, suggesting that Tesla aims to become a leader in AI across multiple domains, potentially reshaping the technological landscape.

Challenge NVIDIA: Tesla’s strategic move towards broader AI capabilities, particularly through its collaboration with Samsung on the AI6 chip, could potentially challenge NVIDIA (NVDA) in several ways. Here’s a detailed analysis:

1. Competition in the AI Chip Market

- NVIDIA currently dominates the AI chip market, with its GPUs being the industry standard for training and deploying AI models. Tesla’s development of the AI6 chip, specifically designed for its autonomous driving and robotics applications, introduces a new player into this space.

- If Tesla’s AI6 chip proves to be competitive in terms of performance, efficiency, and cost, it could capture market share from NVIDIA, especially in sectors where Tesla has a strong presence, such as autonomous vehicles and robotics.

2. Vertical Integration and Supply Chain Control

- Tesla’s partnership with Samsung allows it to control a significant portion of its AI hardware supply chain. This vertical integration reduces dependency on external suppliers like NVIDIA and mitigates risks associated with supply chain disruptions.

- By having a dedicated facility for AI chip production, Tesla can scale production to meet its specific needs, potentially offering a more tailored and responsive solution compared to NVIDIA’s broader market approach.

3. Innovation in AI Hardware

- Elon Musk’s hands-on approach to optimizing the manufacturing process at the Samsung facility could lead to innovations that enhance the AI6 chip’s capabilities. If these innovations result in superior performance or lower costs, Tesla could challenge NVIDIA’s technological leadership.

- The AI6 chip’s design, optimized for Tesla’s specific AI workloads (e.g., neural network training for FSD and Optimus), might offer advantages in certain applications, making it a viable alternative to NVIDIA’s offerings.

4. Market Expansion and Diversification

- Tesla’s expansion into robotics with Optimus and its integration of AI into energy solutions broaden the potential applications of the AI6 chip. This diversification could attract new customers and markets, indirectly competing with NVIDIA’s expanding portfolio, which includes AI for data centers, healthcare, and more.

- If Tesla’s AI capabilities prove successful in these new domains, it could draw interest from industries currently reliant on NVIDIA, thus challenging NVIDIA’s market dominance.

5. Price and Accessibility

- NVIDIA’s GPUs are often expensive, which can be a barrier for some customers. If Tesla can produce the AI6 chip at a lower cost due to economies of scale or strategic partnerships, it could offer a more accessible option for AI development, particularly for startups or smaller companies.

- This could disrupt NVIDIA’s pricing strategy and force it to adapt, potentially impacting its profit margins.

6. Long-Term Strategic Implications

- Tesla’s move could signal the beginning of a trend where automakers and tech companies develop their own AI hardware, reducing reliance on traditional semiconductor giants like NVIDIA. This shift could lead to a more fragmented market, where NVIDIA faces increased competition from multiple fronts.

- The historical precedent of NVIDIA’s transition from graphics to AI suggests that Tesla’s strategy could evolve further, potentially leading to a general-purpose AI chip line that competes directly with NVIDIA across various applications.

7. Current Market Dynamics (2025 Context)

- As of 2025, NVIDIA controls more than 80% of the market for GPUs used in AI training and deployment, and its chips power over 75% of the world’s TOP500 supercomputers. However, Tesla’s entry into this space, backed by a $16.5 billion deal with Samsung, indicates a significant investment in challenging this dominance.

- The proximity of the Samsung facility to Tesla’s operations and the strategic involvement of Elon Musk suggest that Tesla is committed to making this a long-term competitive effort.

ConclusionWhile NVIDIA’s established position and technological leadership present formidable barriers, Tesla’s strategic move towards broader AI capabilities, supported by its collaboration with Samsung, could indeed challenge NVIDIA. The success of this challenge will depend on the performance and cost-effectiveness of the AI6 chip, Tesla’s ability to scale production, and its capacity to innovate in AI hardware and software. If Tesla can replicate NVIDIA’s success in repurposing technology for new applications, it could significantly alter the competitive landscape of the AI chip market.

Background knowledge of NVDA: NVIDIA’s transition from a company primarily focused on graphics processing units (GPUs) for gaming to a leader in artificial intelligence (AI) and high-performance computing is a significant historical precedent. This evolution can be broken down into several key phases:

- Early Focus on Graphics (1990s-2000s):

- NVIDIA was founded in 1993 with a focus on developing GPUs for the gaming industry. Their early success came from creating powerful graphics cards that enhanced visual quality in video games.

- The company introduced the GeForce series, which became synonymous with high-performance gaming graphics.

- Introduction of CUDA (2006):

- A pivotal moment in NVIDIA’s history was the introduction of CUDA (Compute Unified Device Architecture) in 2006. CUDA is a parallel computing platform and programming model that leverages the power of GPUs for general-purpose computing.

- This allowed developers to use GPUs not just for graphics but for a wide range of computational tasks, significantly expanding the applicability of NVIDIA’s hardware.

- Expansion into Scientific Computing and AI (2000s-2010s):

- NVIDIA began to penetrate markets beyond gaming, including scientific research, data centers, and AI. The ability to perform parallel computations made GPUs ideal for training complex AI models, which require significant computational power.

- The company started to market its GPUs for deep learning and AI applications, positioning itself as a key player in these emerging fields.

- Dominance in AI and Data Centers (2010s-Present):

- By the 2010s, NVIDIA had become a dominant force in AI, with its GPUs being used extensively for training and deploying AI models. The company’s hardware was crucial for advancements in areas like autonomous vehicles, healthcare, and financial services.

- NVIDIA’s Data Center business, which includes AI and high-performance computing, became a major revenue driver, often surpassing its gaming segment in profitability.

- Acquisition and Innovation (2020s):

- NVIDIA continued to innovate and expand its influence through acquisitions like Mellanox Technologies in 2020, which strengthened its position in networking and data center infrastructure.

- The company also introduced new architectures like Ampere and Hopper, specifically designed for AI workloads, further solidifying its lead in the market.

- Market Leadership (2025):

- As of 2025, NVIDIA controls more than 80% of the market for GPUs used in training and deploying AI models and provides chips for over 75% of the world’s TOP500 supercomputers. This dominance is a direct result of its strategic shift towards AI and high-performance computing.

NVIDIA’s transition is characterized by its ability to repurpose existing technology (GPUs) for new, high-demand applications (AI and scientific computing), coupled with significant investments in software (CUDA) and strategic acquisitions. This precedent is relevant to the discussion of Tesla potentially developing a general-purpose AI chip line, as it illustrates how a company can pivot and expand its market influence by leveraging existing capabilities in new domains.

If I have to use ONE word to describe the purpose of Tesla AI6 chip, it’s gonna be “CONVERGENCE”. AI6 will converge to a unified architecture that serves as the foundational HW for Tesla’s entire AI stack. I.e.: 1. Data Centers (Cortex 1,2,3 & beyond) 2. Autonomous vehicles (FSD, Robotaxi, Semi, partner vehicles) 3. Optimus bots (humanoid + other form factors) Basically, it draws from Dojo’s chip design principles (e.g., high parallel compute power and low latency) but adapts them for way broader use. For internal & external use. AIaaS type of services will be enabled. Tesla will likely use variants of the same core chip across domains, eliminating the need for entirely separate R&D dev pipelines. Lower customization means faster time-to-market for all product lines. If I remember correctly, Elon has emphasized the “strategic importance” of this approach, highlighting how it positions Tesla to compete more effectively in AI hardware against giants (like Nvidia). IMO, Tesla will no longer build isolated chipset & toolset for specific tasks but creating a cohesive HW/SW platform that leverages shared development, much like how smartphones converged cameras, GPS, and computers into one device. This is why I think “CONVERGENCE“ is the real purpose of AI6 chip development. Let me know what you think.

- 20:35 Optimus timestamp – Musk mentioned that there are two options for Optimus, one with few thousands of version2, the other with few hundreds version3, by the end of 2025. version3 is way better than v2. He prefer to choose option2.

- @40 min. Elon is talking about Sci Fi series Westworld.

- @1:02:00 Telegram is much more potent than X! It has many features that X hopes to have some day. Elon should open up to collaborate with Durov!

- Tesla’s valuation could hit $25 trillion to $30 trillion if we execute well.

Lars Moravy Interview | Inside Tesla’s Engineering Future | X Takeover 2025

Tesla’s stock not moving doesn’t mean the company sucks or that we won’t ever make money again. Tesla is truly between two waves now. We are in the middle of it. After the Austin Robotaxi launch, my confidence in this company has increased. If the San Francisco launch happens this weekend, the pace of expansion is real. That’s all that matters for the eventual stock pop. Near-term, all that matters is the 2nd wave. Robotaxi revenues will fund the third wave. The 3rd wave is the most important: Optimus (aka: real-world AI). This is the rogue wave. This is still a dream too far out of reach for most people. We won’t truly understand how profound this will become until it starts performing useful tasks and frees us from daily grinds. Remember, the TAM (total addressable market) is the human labor force. This is not an opportunity I want to miss, no matter how many ups and downs I have to endure with this stock. It’s the ultimate prize that matters. NFA $TSLA

- 07/27/2025 –(1) Yahoo Finance on X: “”My view is that Musk is going to be a part of the AI future in the US,” Wedbush Securities managing director @DivesTech told Yahoo Finance this week. Full interview: https://t.co/fxLEcDnJXx” / X Ives predicts that within 6-12 months, Tesla’s AI initiatives, particularly robo-taxis, could become more evident, potentially shifting perceptions and market dynamics significantly.

- Tesla’s AI Future: Ives believes Tesla is entering a “golden age” due to its focus on AI, autonomous robotics, and robo-taxis, which he sees as key to its long-term value.

- Short-Term Challenges: He acknowledges that Tesla might face “rough quarters” in terms of deliveries due to expiring U.S. incentives for EVs, but this is temporary.

- Long-Term Vision: Ives frames Tesla’s current period as a “golden buying opportunity,” predicting a $2 trillion market cap driven by AI and autonomous technologies.

- Competitive Landscape: Despite a competitive field in AI and autonomous driving, Ives is convinced Tesla will dominate, particularly in the automated market and humanoid robotics.

- Strategic Integration with xAI: The integration of xAI’s Grok into Tesla, as announced by Musk, is seen as a significant step that could enhance Tesla’s AI capabilities.

- Political Distractions: Ives discusses Musk’s political ambitions, including the formation of the “America Party,” but downplays its immediate impact on Tesla, suggesting Musk’s focus remains on AI.

- Board Accountability: He expresses concern about Tesla’s board needing more backbone, especially with Musk’s 25% voting rights, to ensure accountability during this critical transformation.

- Market Volatility: Ives notes Tesla’s stock has been volatile, down 24% in 2025, but sees this as part of a broader transition from EV to AI, likening it to missing broader potential by focusing only on current offerings.

- Fourth Industrial Revolution: He positions Tesla within the fourth industrial revolution, emphasizing AI’s role in physical applications like robo-taxis and humanoids, alongside other tech giants like NVIDIA.

- Future Timeline: Ives predicts that within 6-12 months, Tesla’s AI initiatives, particularly robo-taxis, could become more evident, potentially shifting perceptions and market dynamics significantly.

- 07/26/2025 –

from 47:00 to 49:00, Alexandra Merz mentioned about the conspiracy theory of Musk intended to suppress the stock price before finalization of comp package, which is at the beginning or mid of sept, about 1.5 month away. I agree with her comments.

00:00 Intro and Overview 01:25 Tesla xAI 07:42 Earnings Call Recap 15:29 Tesla’s Growth Strategy 33:04 Robotaxi Discussion 39:52 Self-Driving Future 50:55 Robotaxis & Stock Impact 01:05:34 Master Plan 4 01:09:04 Shareholder Call to Action

- 07/26/2025 – Yun-Ta Tsai on X: “Hard problems feel more attainable when everyone is in the trenches, with you.” / X

FSD in Here on X: “@YunTaTsai1 Musk is that type of guy.” / X

Yun-Ta Tsai on X: “@1BigTeslaFan Yeah.” / X

- 07/25/2025 – (1) Elon Musk on X: “Extreme execution is needed, but a valuation of $20 trillion for Tesla is possible” / X

- 07/25/2025 – in depth review of FSD technology (1) phil beisel on X: “The Magic of Tesla FSD, part 6 (Robotaxi edition)” / X

Previous articles in this series include:

The Magic of FSD, part 5

The Magic of FSD, part 4

The Magic of FSD, part 3

The Magic of FSD, part 2

The Magic of FSD, part 1

- 07/24/2025 – (1) Dan Ives on X: “We would be buyers on any Tesla weakness. This is an AI story and the autonomous and robotics future is the future. Deliveries under near term pressure…but Musk is driving AI future and autonomous worth $1 trillion to the story. That’s our bull thesis and focus for Tesla🔥🏆🐂” / X

- 07/24/2025 – Pejjy on X: “Like I’ve said many times. Trump will not do anything to Elon’s companies. https://t.co/9qUQbd9uOb” / X

- 07/23/2025 – Tesla, Inc. 2025 Q2 – Results – Earnings Call Presentation (NASDAQ:TSLA) | Seeking Alpha

Here is a summary of the Tesla, Inc. (TSLA) Q2 2025 Earnings Call Transcript from Seeking Alpha in 10 bullet points:

- Financial Performance: Tesla reported Q2 2025 revenue of $22.5 billion, a 12% year-over-year decline, with an EPS of $0.40, meeting analyst expectations but slightly missing revenue forecasts. Automotive revenue grew 19% sequentially due to higher average selling prices and a 14% increase in deliveries.

- Robotaxi Launch: Tesla launched its first commercial robotaxi service in Austin, Texas, in June 2025, marking a significant step in its autonomous driving strategy. The service has driven over 7,000 miles with no safety-critical interventions.

- Autonomous Driving Progress: Full Self-Driving (FSD) subscription rates increased by 45%, with overall penetration up 25% since the release of FSD version 12 in North America. Tesla’s FSD is reported to be statistically ten times safer than human-driven vehicles.

- Tariff and Credit Challenges: Tariff costs rose by $300 million sequentially, impacting the automotive segment most heavily. The repeal of the $7,500 IRA EV credit and declining regulatory credit sales (from $890 million to $439 million year-over-year) are expected to pressure future revenues.

- Energy Business Growth: The energy segment achieved record power deployment and gross profit of $846 million in Q2 2025, with improved margins despite tariff and legislative headwinds affecting residential storage due to expiring consumer credits.

- Vehicle Production and Portfolio: Production of a more affordable vehicle model began in June 2025, with volume production planned for the second half of 2025. The ramp-up will be slower than expected to prioritize deliveries before EV credit expiration.

- AI and Infrastructure: Tesla scaled its AI infrastructure to 67,000 H100-equivalent GPUs, supporting advancements in autonomous driving and robotaxi services. Over 5 billion miles have been driven using FSD (Supervised).

- Bitcoin Impact: A $284 million mark-to-market gain from Bitcoin holdings (via Redcom Holdings) contributed to sequential growth in other income, contrasting with a $125 million loss in the prior quarter.

- Future Expansion Plans: Tesla aims to expand its robotaxi service to cover half the U.S. by year-end, with pending regulatory approvals for markets like San Francisco, Nevada, Arizona, and Florida. The Cybercab and Semi are slated for volume production in 2026.

- Stock and Market Reaction: Despite meeting EPS expectations, Tesla’s stock dipped approximately 4.5% in after-hours trading, reflecting cautious investor sentiment amid delivery declines and margin pressures (auto margins fell from 18% to 15%)

Here is a summary of Elon Musk’s key points from the Tesla, Inc. (TSLA) Q2 2025 Earnings Call, based on the Seeking Alpha transcript, in 10 bullet points:

- Robotaxi Milestone: Musk highlighted the June 2025 launch of Tesla’s first commercial robotaxi service in Austin, Texas, emphasizing its success with over 7,000 miles driven without safety-critical interventions.

- Autonomous Driving Focus: He stressed that Tesla’s core mission is to achieve full autonomy, with Full Self-Driving (FSD) version 12 showing a tenfold safety improvement over human drivers.

- FSD Adoption Growth: Musk noted a 45% increase in FSD subscription rates and a 25% rise in overall FSD penetration in North America, crediting improved performance and reliability.

- Affordable Vehicle Strategy: He discussed the start of production for a more affordable vehicle model in June 2025, with plans for volume production in late 2025 to counter EV credit expiration impacts.

- Energy Sector Strength: Musk praised the energy business’s record power deployment and $846 million gross profit, despite challenges from tariffs and expiring consumer credits.

- AI Infrastructure Expansion: He highlighted Tesla’s AI advancements, with 67,000 H100-equivalent GPUs supporting FSD and robotaxi development, and over 5 billion miles driven on FSD (Supervised).

- Regulatory Credit Decline: Musk acknowledged a drop in regulatory credit sales from $890 million to $439 million year-over-year, citing it as a headwind for future revenues.

- Bitcoin Gains: He briefly mentioned a $284 million mark-to-market gain from Bitcoin holdings via Redcom Holdings, boosting other income for the quarter.

- Future Robotaxi Expansion: Musk outlined plans to expand robotaxi services to half the U.S. by year-end, pending approvals in markets like San Francisco, Nevada, Arizona, and Florida.

- Cybercab and Semi Outlook: He confirmed volume production for the Cybercab and Tesla Semi is targeted for 2026, aligning with Tesla’s long-term autonomous and electric vehicle goals.

- 07/23/2025 – (1) Elon Musk on X: “@karpathy Andrej, my long lost brother, let us work together again!” / X

- 07/21/2025 – Elon’s compensation package. The Tesla board, particularly the Compensation Committee, would need to review and approve the compensation proposal well in advance of the proxy publication—likely in late August or early September 2025. Does Musk have the incentive to suppress the stock price in order to help with possible achievement of compensation package target?

Start Date: The market cap growth milestones began to be measured from the date of shareholder approval, which occurred on March 21, 2018, during Tesla’s annual shareholder meeting. The proxy statement specifies that the vesting of each tranche (1% of shares per milestone) was contingent on achieving specific market cap increases above a baseline, with the clock starting post-approval. The baseline market capitalization was set at $59.1 billion as of January 19, 2018 (the last trading day before the board’s approval), but the performance period officially commenced after the March 21, 2018 vote. could this timeline be the same for 2025 compensation package?

(1) Ale𝕏andra Merz 🇺🇲 on X: “Make sure – now – that you can vote!” / X

Based on the information available, including the X post by @TeslaBoomerMama and related web sources, there’s no explicit date specified for when the Tesla board will finalize its decision on Elon Musk’s compensation package. However, we can infer a timeline based on the shareholder meeting and voting process outlined:

- Shareholder Meeting Date: The next Tesla shareholder meeting is scheduled for November 6, 2025, as noted in the X post. This is when shareholders will vote on critical issues, including Musk’s $55.8 billion compensation package, which was struck down earlier this year by a Delaware court but is being put back to a vote.

- Proxy Publication and Record Date: The proxy statement, which will detail the compensation package and allow voting, is likely to be published between September 12–22, 2025, with a record date (to determine eligible voters) around September 8, 2025 (with a safe range of September 1–10, 2025). The board typically finalizes its recommendations for the compensation package before this proxy is released, as it will reflect their stance.

- Board Decision Timeline: The Tesla board, particularly the Compensation Committee, would need to review and approve the compensation proposal well in advance of the proxy publication—likely in late August or early September 2025. This allows time for legal and regulatory review, especially given the contentious history of Musk’s pay package and potential litigation risks noted in sources like Investopedia and Pearl Meyer.

Given that it’s currently 08:13 AM PDT on Monday, July 21, 2025, the board’s final decision is likely still weeks away, with preparations possibly intensifying in the coming month. The exact date isn’t public yet, but historical patterns (e.g., the 2018 plan approval) suggest the board aims to lock in its position by early fall, aligning with the September proxy release. For the most precise update, monitor Tesla’s official SEC filings or announcements, as the board’s decision will be detailed in the proxy statement.

2018 Compensation Package: The 2018 compensation package for Elon Musk, as detailed in Tesla’s SEC proxy statement and referenced in web sources like Investopedia and Pearl Meyer, was a performance-based stock option award designed to align Musk’s incentives with Tesla’s long-term growth. Here are the key components:

- Structure: A performance-based nonqualified stock option award, approved by the Tesla Board on January 21, 2018, with Musk and his brother Kimbal recusing themselves. It required shareholder approval (excluding Musk and Kimbal’s shares).

- Size: The package covered 12% of Tesla’s outstanding shares (approximately 20.3 million shares based on 168.9 million shares outstanding as of January 19, 2018), divided into 12 tranches, each representing 1% of shares.

- Performance Milestones: Vesting was tied to Tesla achieving specific market capitalization and operational targets over 10 years:

- Market Cap Growth: Total market capitalization increases in increments of $50 billion, starting from a base of $59.1 billion (e.g., $109.1 billion for the first tranche, up to $650.1 billion for the 12th).

- Operational Targets: Revenue growth (e.g., $20 billion annually) and adjusted EBITDA (e.g., $1.5 billion) thresholds, escalating with each tranche.

- Value: Initially valued at approximately $2.6 billion when granted, it ballooned to $55.8 billion by 2024 due to Tesla’s stock price surge, though the court later voided it in December 2024 over governance issues.

- Tax Implications: Tesla could only deduct up to $1 million of Musk’s compensation annually due to IRS Section 162(m) limits, regardless of the award’s realized value.

- Purpose: Aimed to retain Musk and drive transformative growth, though the Delaware court found no evidence it was necessary, citing Musk’s other ventures (e.g., SpaceX).

Potential 2025 Compensation PackageThe 2025 compensation package, likely to be proposed for the November 6, 2025 shareholder meeting, isn’t finalized yet, but we can speculate based on current context, the @TeslaBoomerMama X post, and recent developments:

- Structure: Expected to remain performance-based stock options, given its past success in aligning Musk’s interests with shareholders, though the board may adjust to address Delaware court concerns (e.g., independence of the Compensation Committee).

- Size and Value: Given Tesla’s current market cap (around $1 trillion as of mid-2025 estimates) and the voided $55.8 billion package’s escalation, a new package could range from $60–$100 billion, reflecting Tesla’s growth and Musk’s $418 billion net worth (per Investopedia, February 2025). The X post hints at a potential xAI investment vote, which might tie compensation to AI milestones.

- Performance Milestones: Likely to include:

- Market Cap Targets: Higher thresholds (e.g., $1.2 trillion to $2 trillion) to reflect Tesla’s scale.

- AI and xAI Integration: Metrics tied to xAI’s valuation or Tesla’s AI projects (e.g., Full Self-Driving revenue), especially with SpaceX’s rumored $2 billion xAI investment (Wall Street Journal, July 15, 2025).

- Operational Goals: Continued focus on revenue (e.g., $100 billion annually) and profitability, possibly with new energy or robotaxi targets.

- Governance Adjustments: Post-2024 ruling, the board may emphasize independence (e.g., no Musk family ties in decision-making) and justify the package’s necessity, countering the court’s finding that it wasn’t retention-driven.

- Contingencies: If the appeal of the 2018 package ruling fails (ongoing as of July 2025), a new plan might require stricter shareholder approval processes, potentially increasing its size to compensate for legal risks.

Key Differences

- The 2018 package was groundbreaking but lacked robust independence scrutiny, leading to its voidance. The 2025 version may prioritize governance to survive legal challenges.

- The 2025 package could integrate xAI and AI innovation, reflecting Musk’s broader vision, unlike the 2018 focus on automotive growth.

- Valuation will be higher due to Tesla’s stock performance, but the structure might include more granular milestones to appease shareholders and courts.

Elon Musk’s 2018 CEO Performance Award—the famously ambitious pay package tied to Tesla’s market cap and operational goals—was granted on January 21, 2018.

This grant date reflects the date when Tesla’s Board formally awarded Musk a performance-based stock option package. It was later approved by shareholders during a special meeting held on March 21, 2018, which made the award effective.

Tesla Announces New Long-Term Performance Award for Elon Musk | Tesla Investor Relations

edfcfa2e-bcb6-43ed-ab53-4b08b3bf21ca (3300×2550)

Since it’s 08:20 AM PDT on Monday, July 21, 2025, the 2025 package details will emerge in the proxy statement (expected September 12–22, 2025). Monitor Tesla’s SEC filings for confirmation, as the board’s late August/early September decision will shape the proposal.

- 07/20/2025 – Elon sent out lots of messages on TSLA today (1) Elon Musk on X: “Your Tesla self-driving capability will see a step change improvement as we integrate upgrades for the Austin robotaxi build into the general production release” / X

(1) Sawyer Merritt on X: “@elonmusk Can we expect this in Q3?” / X

(1) Elon Musk on X: “@SawyerMerritt Looking good so far” / X

(1) Elon Musk on X: “Tesla Semi Factory progress” / X

- 07/20/2025 – (1) Elon Musk on X: “Back to working 7 days a week and sleeping in the office if my little kids are away” / X

(1) SMX 🇺🇸 on X: “Wartime CEO Engaged. “7 days a week sleeping in the factory, No one should put these many hours into work, this is not good, this is very painful, it hurts my brain and my heart.” -Elon Musk https://t.co/Rl2g3Xdp94″ / X(1) Elon Musk on X: “Back to working 7 days a week and sleeping in the office if my little kids are away” / X

(1) Tetsuo on X: “For the love of the game. https://t.co/4GvIVGbmS8” / X

- 07/20/2025 – (1) Elon Musk on X: “I resisted AI for too long Living in denial Now it is game on @xAI @Tesla @SpaceX” / X

I resisted AI for too long Living in denial Now it is game on @xAI @Tesla @SpaceX

- 07/19/2025 – Exclusive | Trump Aides Discussed Killing Some of Elon Musk’s SpaceX Contracts. Here’s Why They Couldn’t. – WSJ

For the U.S. government, breaking up with Elon Musk is easier said than done.

Just days after President Trump in early June raised the prospect of cutting ties with Musk’s businesses, the Trump administration initiated a review of SpaceX’s contracts with the federal government, according to people familiar with the matter. The review was intended to identify potential waste in the multibillion-dollar agreements the company has with the government, the people said.

But administration officials determined that they couldn’t eliminate most of those contracts because they are critical to the Defense Department and NASA, the people said. The early assessment underscored the company’s dominance as the world’s pre-eminent rocket launcher and a major satellite-internet provider.

A White House official said the review of government contracts focused on a range of companies with lucrative government contracts.

Musk and SpaceX didn’t respond to requests for comment.

- 07/19/2025 – (1) Elon Musk on X: “Wow” / X

- 07/19/2025 – (1) Whole Mars Catalog on X: “Wow. They really are scaling https://t.co/QLtTz2umIj” / X

- 07/20/2025 – (1) Elon Musk on X: “@DimaZeniuk It’s so good” / X

Tesla Optimus V3 will have many improvements

Elon Musk: It’s so good