Study of DPST, KRE and FAS – part II

- 04/25/2024 – Main Street Banking Model Is Being Squeezed – WSJ, First-quarter results at regional banks show the uneven toll of higher interest rates

Higher-for-longer interest rates are continuing to weigh on Main Street banks.

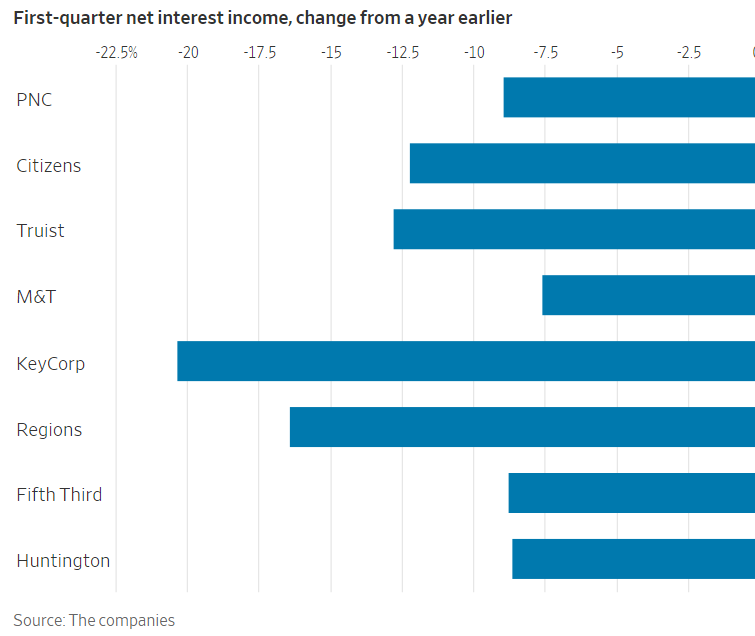

Regional banks posted steep profit declines in the first quarter and predicted more pain ahead. The results underscore the uneven toll that two years of higher interest rates have taken on regional banks, which tend to have plain-vanilla businesses taking in deposits and making loans. That model has become less profitable because of the pressure to pay up on deposits.

Profit fell by more than a fifth from a year earlier at U.S. Bancorp USB -1.78%decrease; red down pointing triangle, Truist Financial TFC -2.64%decrease; red down pointing triangle and M&T Bank MTB -0.93%decrease; red down pointing triangle and by around a third or more at Citizens Financial Group CFG -1.87%decrease; red down pointing triangle, KeyCorp KEY -2.75%decrease; red down pointing triangle and Huntington Bancshares HBAN -1.64%decrease; red down pointing triangle. At Comerica CMA -2.42%decrease; red down pointing triangle, profit declined by more than half.

At the biggest banks this quarter, rate pressure began to emerge, but profits were down much less overall.

One bright spot for some regional banks: a rebound in fee businesses such as wealth management, treasury management and investment banking. Noninterest income rose 8% at U.S. Bancorp, 7% at Citizens and 6% at Key. Even select smaller banks enjoyed a boost. At the holding company for First National Bank of Pennsylvania FNB -0.55%decrease; red down pointing triangle, F.N.B. FNB -0.55%decrease; red down pointing triangle, noninterest income rose 11%.

“The more diversified the revenue this quarter, the better the results,” said RBC analyst Gerard Cassidy.

Significant fee businesses are few and far between across the nation’s more than 4,500 regional and community banks. And compared with the giant fee businesses of megabanks such as JPMorgan Chase, those that exist are tiny.

The Federal Reserve recently signaled that stubborn inflation may force it to keep rates at their current high levels for longer than expected, a particular problem for banks without much diversity and scale. In the first quarter, most of the larger regional banks forecast that net interest income, the difference between what they earn on loans and pay out on deposits, would fall for the full year.

Bank shares have risen broadly this week. The KBW Nasdaq Bank Index and the SPDR S&P Regional Banking ETF are each around 3% higher. But many bank stocks have yet to fully recover from a year punctuated by selloffs.

“People are still on nervous footing,” Zach Wasserman, chief financial officer at Huntington, said. “But I think now there is a recognition that some firms really weathered that and proved the resilience of their models.”

Banks have in recent quarters piled away reserves for losses in commercial real estate books, especially for loans on offices that have emptied since the pandemic. Regulators, bankers and analysts have said those issues would play out over a number of quarters, without risks to the broader financial system.

“I’m sure there will be more surprises,” U.S. Bancorp Chief Financial Officer John Stern said, referring to commercial real estate across the industry. “There may be one-off banks here and there, but there won’t be a sector-wide thing.”

Commercial real estate losses in the fourth quarter at New York Community Bancorp NYCB -0.82%decrease; red down pointing triangle had sparked a moment of panic earlier this year. But those losses were tied to a uniquely large portfolio of loans for rent-stabilized New York apartments. NYCB, which got a rescue infusion from investors in March, hasn’t said when it will report first-quarter results.

At PNC Financial Services PNC -1.95%decrease; red down pointing triangle, net charge-offs in commercial real estate rose to more than $50 million in the first quarter from around $10 million a year earlier. The bank expects more stress in that space, especially for office loans.

“The problem you have in office is, in many instances, there is no cash flow at all,” PNC Chief Executive Bill Demchak said on a call with analysts. “It is really a unique animal at the moment.”

For signs that the turbulent commercial real-estate market is beginning to stabilize, look at Blackstone’s largest real-estate fund, known as Breit.

The firm was able to fulfill all investor redemption requests in February and March for the first time since late 2022, when a flurry of withdrawals compelled it to limit how much it could pay out.

“We believe commercial real estate is at an inflection point, with real estate values bottoming,” Blackstone said in an April letter to Breit shareholders, who are mostly individual investors.

But that is only part of the story. Breit fundraising hasn’t returned to its previous robust levels. Investor withdrawals continue to greatly exceed new cash coming in, a sign of lingering worries about the backdrop for commercial properties.

Breit turned a corner in one respect this year. In February and March, redemption requests declined to $961 million and $799 million, respectively, low enough for Breit to pay all of them. In January 2023, redemption requests exceeded $5 billion.

- 04/23/2024 – KRE | SPDR S&P Regional Banking ETF Stock Price, Quotes and News – WSJ to read the earning transcripts of these companies and understand their conditions (https://seekingalpha.com/account/people)

TOP 10 HOLDINGS KRE

| Name | % of Total Portfolio |

|---|---|

Regions Financial Corp. |

2.55% |

Western Alliance Bancorp. |

2.54% |

Citizens Financial Group Inc. |

2.53% |

Truist Financial Corp. |

2.49% |

Webster Financial Corp. |

2.48% |

Huntington Bancshares Inc. |

2.46% |

Bank OZK |

2.46% |

First Horizon Corp. |

2.46% |

East West Bancorp Inc. |

2.45% |

Zions Bancorp N.A. |

2.45% |

Regional banks have started to report first-quarter earnings, and investors are worried that more Warbasses will be revealed. Shares of these small and midsize banks, which are stuffed with loans for office buildings, apartment complexes and other commercial properties, are near their lowest level in five months.

My banking-expert friend, whom I quoted extensively in many e-mails in early February (archive here), thinks that what Schwab is doing is likely to catch up with it… which is one of the reasons his fund is short SCHW.

He sent me a detailed e-mail with his thoughts, which he kindly gave me permission to share with my readers here. As he says:

I saw your write-up on SCHW today and thought I’d pass along a few comments as I think the stock is incredibly overvalued – and one of the primary reasons is exactly the dynamic that you pointed out. Great job exposing this topic!

Schwab has $269.5 billion of deposits with an average cost of only 1.35%! I am dumbfounded at the fact they have kept the cost of these deposits so low given their customers should be of an investor mindset, and even if a customer is primarily trading stocks they should still be focused on what their cash is earning.

As you point out, I’ve heard from others that it isn’t so clear to see or know what your cash is earning (or not earning in this case!). My sister-in-law was getting hosed on a decent cash balance and said she couldn’t find the rate anywhere, so she eventually called to have her cash moved into a money market but, like you, it sat in their low-yielding product for way too long.

Now that we are in a “higher-for-longer” environment, it is just a matter of time before those deposit costs move meaningfully higher, particularly as more people like you start realizing you’ve been taken advantage of. The average cost of deposits in the banking industry is likely going to be near 2.5% after all the Q1 reports are filed, and I would say the banking industry should have a lower cost of deposits than Schwab given traditional banks have more non-interest bearing/transaction deposits.

To put this into perspective, Schwab – the entire company – is expected to earn around $6.2 billion in 2024. The management is very promotional and acts like their cost of deposits could potentially decline if there are rate cuts, which I strongly disagree with. You can easily do the math… if their cost of deposits only goes up by only 1%, that is a pre-tax cost of $2.7 billion! (And if the higher-for-longer environment persists for several years, it wouldn’t surprise me to see the Schwab deposits move materially higher than a 1% increase.)

Even if SCHW can achieve these earnings estimates, the stock is trading at over 21 times earnings. And analysts are expecting earnings to grow 28% in 2025 to $4.37/share. I really struggle to see how they can grow earnings at all amidst this dynamic.

As he continues, the cost of deposits is just one of the issues caused by the higher-for-longer environment: (The 10-Q filing deadline for The Charles Schwab Corporation is due on Monday, June 10, 2024. This report covers the quarterly period ended April 30, 2024 – watch out before this date)

Schwab’s bank is one of the worst in the industry when it comes to fair value marks. They have not filed their 10Q and bank call report yet for Q1, but I estimate that their held-to-maturity securities mark is roughly $14.6 billion and their loan portfolio mark is roughly $1.9 billion (both tax-adjusted), which would leave them with negative tangible common equity of over $3.7 billion (they currently have stated tangible common equity of only $12.8 billion)!

If the regulators (or investors) decide to refocus on the fair value issues that sunk Silicon Valley Bank and First Republic, then it would be impossible for Schwab to avoid scrutiny as it is the 11th largest bank in the country. If I were the regulator, I would force Schwab Bank to immediately raise a significant amount of capital.

If you are wondering why they have these massive interest rate marks, they basically took in large amounts of low-cost deposits that they thought would be cheap forever, so like most banks they went out and bought securities (primarily RMBS [residential mortgage-backed securities] and CMBS [commercial mortgage-backed securities]) to capture some spread. Schwab’s securities portfolio yields less than 2%, so as their deposit costs rise they could have a big portion of their balance sheet with a negative spread.

Here is the bank call report data from 12/31/23 (note that the $11.2 billion held-to-maturity loss was at 12/31). I am estimating the securities are worth 88 cents on the dollar in coming up with my current $14.6 billion mark.

In addition to buying the low-yielding securities, Schwab took on $9.35 billion of 1-4 family mortgages that are yielding in the 3% range! That is the driver of the nearly $2 billion tax-adjusted loan mark.

For sake of full disclosure, I am short the stock, but regardless thought you would find this summary interesting given I would say it is just a matter of time before more people like you wake up to the fact that as you put it: “Schwab is screwing you over in the same way banks are screwing their customers who are holding cash in their savings accounts.”

Not only will Schwab’s interest expense skyrocket, but I think they have reputational risk as customers could easily be soured after learning they’ve been burglarized by the company over the past couple of years.

I’d like to give a huge thank you to my friends and readers for taking the time to share your thoughts!

When it comes to Schwab’s stock, I agree that it looks like one to avoid.

- 04/16/2024 – Investment Banking Bounceback Powers Big U.S. Lenders – WSJ Top banks post better-than-expected results, helped by strong consumer spending and flurry of Wall Street activity

America’s biggest banks reported stronger-than-expected earnings in the first quarter, highlighting how a resilient economy is helping power everything from Main Street to Wall Street.

JPMorgan JPM 2.51%increase; green up pointing triangle Chase, Bank of America BAC 3.35%increase; green up pointing triangle, Citigroup C 1.41%increase; green up pointing triangle, Wells Fargo, Goldman Sachs GS 0.22%increase; green up pointing triangle and Morgan Stanley MS 0.44%increase; green up pointing triangle all reported revenue and earnings that beat or met analysts’ expectations. Consumer spending remained robust. Pent-up demand for dealmaking, stock and bond sales lifted earnings at the Wall Street-heavy banks. A market rally continued in early 2024, boosting fees the banks collect on money they manage for clients.

But the results were tempered by rising pressure from interest rates, which squeezed profit margins. Banks are warning that the recovery in capital markets is fragile. And many said they don’t expect much revenue and profit growth this year.

As a group, the six big banks reported $35.63 billion in profits, down 3% from a year ago, with half of the banks reporting a decrease in profit and half of them reporting an increase. Combined revenue rose 4% to $139.07 billion.

- Financial technology has already helped level the playing field for smaller banks competing against giants like Wells Fargo and Chase, and AI is being viewed as the next tech arms race for Main Street in keeping up with Wall Street.

- “The teller line, as we see it today, will eventually die,” says one community bank CEO, who tells CNBC that the future branch will look more like “a wall of screens.”

- JPMorgan CEO Jamie Dimon wrote in his annual letter to shareholders this week that AI will have vast implications for bank worker roles across its more than 300,000 employees.

- 04/12/2024 – High Rates Have Been a Profit Machine for Banks. Not Anymore. – WSJ JPMorgan, Wells Fargo and Citigroup post better-than-expected first-quarter results, but their forecasts are muted

But the still-strong economy is also keeping inflation higher than hoped, forcing the Fed to hold interest rates up. Data this week seemed to remove expectations of a Fed rate cut in June, and the markets are reconciling with the likelihood that elevated rates are here to stay. Bankers said Friday that customers are moving more money around to chase those rates, which is going to eat into margins for the year.

A key profitability metric called net interest income—which measures the difference between what banks pay out on deposits and charge on loans—shrank on a quarterly basis at JPMorgan for the first time since 2021. It also fell from the last quarter at both Wells Fargo and Citigroup.

For the full year, JPMorgan expects that measure to be roughly flat. Wells Fargo and Citi expect it to fall.

“Rates might be higher than what people expected a week ago,” Wells Fargo Chief Financial Officer Mike Santomassimo said on a call with analysts. “We do have to wait and see how clients are going to react.”

Commercial real estate continues to be a point of stress for the banking system, although it is a proportionally larger problem for some smaller banks, which have invested a lot more into office and retail loans than big banks. JPMorgan Chief Financial Officer Jeremy Barnum said that the bank’s book of commercial real-estate loans wasn’t getting significantly worse, but still faced challenges.

“There’s no light at the end of the tunnel yet,” Barnum said.

The scale and diversity of the megabanks help them navigate good times and bad. But regional and community banks could reveal a deeper toll from higher interest rates next week, when they start to report first-quarter results.

Smaller banks are highly dependent on interest income. They are also under more scrutiny after the high-profile failures of three regional banks last year. In the fourth quarter, surprise losses at New York Community Bancorp revived concerns that commercial real estate could kick up another crisis.

In the first quarter, the biggest U.S. banks were hit again with special fees owed to the Federal Deposit Insurance Corp. for their share of the government’s response to last year’s regional-bank crisis. The banks had paid large bills last quarter too.

- 04/08/2024 – Jamie Dimon Warns U.S. Might See Interest-Rate Spike – WSJ, The head of JPMorgan Chase questions the ‘soft landing’ talk but says his bank is ready no matter what

- 03/24/2024 – NYCB and Meridian Rode the Property Boom Together. Now They’re Struggling. – WSJ The bank got many of its loans from a broker now blacklisted by Fannie Mae and Freddie Mac

The turmoil at both companies comes at a difficult time for the commercial real-estate market and the banks that lend to it. Investors and regulators are wary of a coming crush of soured loans—and what it might do to the still-fragile regional banking system. Fannie Mae, Freddie Mac and federal housing regulators are launching wider looks into the opaque market, according to people familiar with the probes. Federal prosecutors are investigating landlords and suspected mortgage fraud, according to people familiar with those efforts.

Freddie Mac issued new guidelines effectively suspending Meridian. The lender has sent letters to other Meridian brokers telling them they are blacklisted even if they go to a different firm, according to people familiar with the matter. Fannie Mae told lenders it would no longer accept Meridian-brokered loans starting March 4, 2024.

The government-backed lenders are now starting to sift through the financials of numerous borrowers and brokers, looking to weed out fabricated numbers, according to people familiar with the matter. Freddie Mac recently told borrowers to submit their numbers directly, effectively going around brokers altogether.

Earlier this month, NYCB got a lifeline with an investment of more than $1 billion from former Treasury Secretary Steven Mnuchin and others. Carpenter and other longtime NYCB directors departed. Former Comptroller of the Currency Joseph Otting took over as CEO.

Life at Regional and Small Banks, One Year After SVB Failed – WSJ

The banking industry’s middle class is shrinking. It has been one year since Silicon Valley Bank failed and kicked off a crisis among the nation’s regional banks, and the recent disruption at NYCB shows they remain under pressure.

Most regional banks are too small to reap the benefits of scale, diversification and implicit government support enjoyed by megabanks such as JPMorgan Chase and Bank of America. Yet they are too big to escape the scrutiny of investors and regulators. They now face difficult questions on profitability, business models and even their traditional role as the intermediary between depositors and borrowers.

“It has been a year, but it feels a lot longer,” said Chris McGratty, an analyst with KBW.

A New York real-estate bind

At Valley National, Robbins believes his message will eventually click.

“Patience,” Robbins said, has emerged as the watchword for this most-unsettling year. “When they see our first-quarter results, then things will begin to shift.”

Regional lenders are each trying their own approaches to survive, changing business focus, getting bigger, staying smaller. One future most agree on: There are too many of them.

Investor and customer panic has eased significantly since then, but regional and community banks still have a confidence problem. Some customers remain hesitant to keep large uninsured balances anyplace other than the largest banks.

Banc of California made it through the crisis with a handful of wins and then acquired PacWest, a much larger competitor where Wolff used to work. The $1 billion deal, and capital raise that went along with it, allowed Banc of California to roughly quadruple in size.

“There certainly was the sense that the crisis is over because it was a recognition that there was an outcome for banks that might be unstable or perceived to be unstable,” Wolff said, referring to PacWest.

Soon after the announcement, Wolff watched rumors continue to spread on social media about his bank. Posters thought regulators or shareholders would reject the deal. “Both will head into FDIC receivership given their obvious solvency issues,” one Reddit user wrote in August. The rumors weren’t true. The deal won approval and closed in a matter of months.

“We focus on what we can control,” Wolff said. “And I think the results speak louder than anything.”

Private Equity Cautiously Steps In to Back Troubled Banks – WSJ Distress at regional banks has spurred some buyout firms to invest in a sector they typically ignore

Some of those deals worked out, while others ranged from mediocre to disastrous, investors and analysts say. The private equity-backed rescues of IndyMac and BankUnited

yielded strong returns and spurred other firms to go shopping for banks. Others, like TPG’s 2008 investment of $1.35 billion in Washington Mutual shortly before its collapse, showed the dangers of betting on troubled institutions.

“Most people stay away from the [banking] sector because they haven’t lived through the cycles, they don’t have the regulatory or sector expertise, and they don’t know how to achieve what they want,” Berlinski said.

The challenge is finding banks whose value is depressed enough to be bought inexpensively, but not so distressed they go bust. Private equity’s relatively high return targets are also a barrier to investment. Firms generally seek to generate at least a 20% profit on their deals, while the banking industry typically posts profit margins of around 13% to 15%.

“If you’re buying into a bank that’s reasonably healthy and looking for 20% [returns], that’s hard,” said Mike Brown, an analyst at research firm Keefe, Bruyette & Woods. The banking tremors of the past year have “created interesting opportunities for private equity to consider banks, a space that wasn’t traditionally the most attractive spot to deploy capital,” he added.

The scale of private-equity investment has so far been modest, and far below that of the last financial crisis. Investors are skeptical the post-SVB straits will yield much more in the way of private-equity deals unless conditions deteriorate.

The banking sector appears to be stabilizing after last year’s upheaval. The KBW Nasdaq Bank Index, which tracks bank stocks, has recovered to less than 10% below its peak prior to SVB’s collapse.

Adams of Wellington Management says he doesn’t expect to see mass-scale private-equity buying opportunities in banking unless interest rates remain at their current levels for a long spell or go even higher.

Warburg’s Zilberman expects to keep seeing one-off deals, but not a full-blown meltdown.

“I don’t believe we have a distressed sector on our hands,” he said. “I don’t think commercial real estate will blow up, but I think there will be idiosyncratic situations like SVB and NYCB. There will be banks that run into trouble, and when that happens private equity will certainly have opportunities.”

The Problem Isn’t Big Banks—It’s Banks Getting Bigger – WSJ Going from a midsize lender to a larger one comes with regulatory and other challenges

A Federal Reserve review of SVB’s supervision and regulation, published last April, noted that the bank’s “core risk-management capacity failed to keep up with rapid asset growth.” The bank’s growth also changed how it was supervised. The report noted that supervision of the company was “complicated by the transition” from what is known as a Regional Banking Organization, or RBO, to a Large and Foreign Banking Organization, or LFBO, as it crossed $100 billion in assets.

So how could you get to bigger banks without these problems? The Federal Reserve’s latest capital rule proposal would bring some standards to a wider range of banks, though regulatory approaches must also be “tailored” to a bank’s size under current laws. There could also be a preference for already giant banks buying smaller ones. But that can raise other thorny competition issues.

- 03/09/2024 – A Year After Silicon Valley Bank’s Collapse, the Rules Are Still Catching Up – WSJ, New proposed regulations won’t address some root causes of regional banking malaise

Last March, Silicon Valley Bank collapsed and kicked off the most significant U.S. banking crisis in years. A few months later, the Federal Reserve proposed a series of major changes to how big lenders are regulated. Those events are less related than you might think.

The Fed proposals are known as the “Basel III endgame,” in reference to completing the implementation of global banking reforms first outlined well over a decade ago, following the 2008 financial meltdown. These reforms have substantially raised banks’ capital levels and constrained many behaviors that were at the heart of that crisis, like bets on risky mortgages.

A larger group of banks would face some tougher standards under the proposal, including those the size of SVB SIVBQ 0.00%increase; green up pointing triangle. Yet this final batch of rules won’t directly address some of the most salient causes of the collapses of SVB, Signature Bank SBNY 15.67%increase; green up pointing triangle or First Republic. After all, some of SVB’s most troublesome assets were low-risk U.S. Treasurys. At First Republic, a big problem was mortgages for low-risk superprime borrowers—not shaky subprime ones.

And in all three cases, a problematic funding source was their deposits via core customer relationships. This was the exact sort of thing a lot of people said banks needed to refocus on after the 2008 crashes of trading firms like Bear Stearns and Lehman Brothers.

Here is a short recap of what sparked last year’s failures: During the pandemic, banks were flush with deposits and bought bonds, or made loans, at low, fixed interest rates. Then when the Fed started aggressively raising rates in 2022, the market value of those assets fell. That became a problem as banks faced higher deposit costs or increasing withdrawals as customers sought higher yields elsewhere.

But if that crisis was fundamentally about credit risk, then 2023 was about interest-rate risk. And addressing that may require some different ideas.

- 03/08/2024 – Moody’s review on New York Community Bancorp shifts to possible upgrade (NYSE:NYCB) | Seeking Alpha

Moody’s switched the direction of its review on New York Bancorp (NYSE:NYCB) to a possible upgrade from a possible downgrade, following the announcement that NYCB has secured $1.05B in capital commitments from several institutional investors, named a new CEO, and is reconstituting its board, the ratings firm said late Thursday.

The ratings under review include NYCB’s long-term issuer rating of B3, its lead bank, Flagstar Bank, NA’s long-term deposits of Ba3, Flagstar’s baseline credit assessment of b2, Flagstar Bancorp Inc.’s B3 subordinate debt rating, and New York Community Capital Trust V’s backed preferred stock rating of Caa1. All of the ratings are below investment grade.

The capital raise will increase NYCB’s common equity tier 1 ratio to 10.3% on a pro forma basis, assuming full conversion of the preferred equity to common, from 9.2% reported at Dec. 31, 2023.

“The involvement of private equity investors in the bank is helpful to stabilize its capital in the short-term, but creates long-term uncertainties around the bank’s governance and long-run strategy that now also will be explored during the ratings review,” Moody’s said.

The ratings firm also continues to believe that NYCB may have to increase its provisions for credit losses. The company had $992M allowance for credit losses, or 1.26% of total loans excluding loans with government guarantees and warehouse loans, as of Dec. 31, 2023.

Moody’s will pay particular attention to New York Community Bancorp’s (NYCB) Q1 results, noting that its weighted average coupon on its office portfolio is 4.7%; $313M of office loans are maturing in 2024 and $237M are maturing in 2025. NYCB’s reserve coverage is ~8% on its $3.4B of office loans. Meanwhile, ~54% of its office loans are in Manhattan, where office vacancy is ~15%, and its office loans are mostly class B properties, a lower quality than class A properties.

“The review will focus on the outlook for NYCB’s CRE portfolio, plans regarding its ACL, earnings, capitalization, liquid assets and use of wholesale funding,” Moody’s said.

- 03/07/2024 – NYCB lost 7% of deposits in past month, slashes dividend to 1 cent (cnbc.com) – great to view Steven Mnuchin’s interview

- New York Community Bank said Thursday it lost 7% of its deposits in the turbulent month before announcing a $1 billion-plus capital injection from investors led by former Treasury Secretary Steven Mnuchin’s Liberty Strategic Capital.

- The bank had $77.2 billion in deposits as of March 5, NYCB said in an investor presentation tied to the capital raise, down from $83 billion it had as of Feb. 5.

- NYCB also said it’s slashing its quarterly dividend for the second time this year, to 1 cent per share from 5 cents, an 80% drop.

New York Community Bank said Thursday it lost 7% of its deposits in the turbulent month before announcing a $1 billion-plus capital injection from investors led by former Treasury Secretary Steven Mnuchin’s Liberty Strategic Capital.

The bank had $77.2 billion in deposits as of March 5, NYCB said in an investor presentation tied to the capital raise. That was down from $83 billion it had as of Feb. 5, the day before Moody’s Investors Service cut the bank’s credit ratings to junk.

Before announcing a crucial lifeline Wednesday from a group of private equity investors led by Mnuchin’s Liberty Strategic Capital, NYCB’s stock was in a tailspin over concerns about the bank’s loan book and deposit base. In a little more than a month, the bank changed its CEO twice, saw two rounds of rating agency downgrades and announced deepening losses.

At its nadir, NYCB’s stock sank below $2 per share Wednesday, down more than 40%, before ultimately rebounding and ending the day higher. The shares climbed 10% in Thursday morning trading.

The capital injection announced Wednesday has raised hopes that the bank now has enough time to resolve lingering questions about its exposure to New York-area multifamily apartment loans, as well as the “material weaknesses” around loan review that the bank disclosed last week.

‘Very attractive’ bank

Mnuchin puts 15% of his fund into NYCB

- he started looking at NYCB “a long time ago. it is one of the 20 biggest banks in US

- buy of Signatures bank is a great deal. They left the bad loans to the government, smart deal

- 80% deposits are insured

- Joseph Otting be the CEO is good

- multifamily real estates are still cash flow even though are NYC regulated, suboptimal. He thinks it is one-off situation. Interest rate will be lower in the future. Work out the multifamily Real estate for the next two years. Rebuild the business

- rate B or lower of office loans are eliminated from balance sheet, 3.5 bil office loans in NYC is the problem, we will work out the quickest

- agree that the regional banks sector has problem and opportunities now, look for acquisition and merge opportunities

- TBV is $6.60, the price of stock is only $3.30

Mnuchin told CNBC in an interview Thursday that he started looking at NYCB “a long time ago.” “The issue was really around perceived risks in the loans, and with putting billion dollars of capital into the balance sheet, it really strengthens the franchise and whatever issues there are in the loans we’ll be able to work through,” Mnuchin told CNBC’s “Squawk on the Street.” “I think there’s a great opportunity to turn this into a very attractive regional commercial bank,” he added. Mnuchin said that he did “extensive diligence” on NYCB’s loan portfolio and that the “biggest problem” he found was its New York office loans, though he expected the bank to build reserves over time. “I don’t see the New York office working out or getting better in the future,” Mnuchin said.

is getting more than a $1 billion investment, according to people familiar with the matter.

Liberty Strategic, Citadel Securities and NYCB management are participating in the capital investment, the people said.

Former Secretary Steven Mnuchin, Joseph Otting, Allen Puwalski and Milton Berlinski to Join NYCB Board of Directors

Joseph Otting to Become CEO and Alessandro DiNello to be Named as Non-Executive Chairman

Investment is Strong Endorsement of New Management Team; Creates Strong Balance Sheet

Reconstituted Board and Management Team Positioned to Deliver Well Capitalized $100+ Billion National Bank with a Diversified, De-Risked Business Model

HICKSVILLE, N.Y., March 6, 2024 /PRNewswire/ — New York Community Bancorp, Inc. (NYCB) (“NYCB” or the “Company”) today announced that Liberty Strategic Capital (“Liberty”), Hudson Bay Capital (“Hudson Bay”), Reverence Capital Partners (“Reverence Capital”), Citadel Securities (“Citadel”), other institutional investors and certain members of the Company’s management (collectively, the “Investors”) will make a combined over $1 billion investment in the Company, subject to finalization of definitive documentation and receipt of applicable regulatory approvals. Liberty is expected to invest $450 million, Hudson Bay will invest $250 million, and Reverence will invest $200 million as part of the transaction.

Transaction Details

In connection with the equity capital raise transaction, NYCB will sell and issue, in the aggregate, to the Investors shares of common stock of the Company at a price per share of $2.00 and a series of convertible preferred stock with a conversion price of $2.00, for an aggregate investment amount of $1.05 billion. In addition, investors will receive 60% warrant coverage to purchase non-voting, common-equivalent stock with an exercise price of $2.50 per share, a 25% premium to the price paid on common stock.

Holders of the preferred stock will not have voting rights and will be entitled to quarterly non-cumulative cash dividends, as and if declared by the Board. Each share of preferred stock is convertible into common stock on a 1 preferred share – 1,000 common shares basis. Series B preferred stock will automatically convert upon certain transfers permitted by federal banking regulations and stockholder approval of a charter amendment to increase the Company’s authorized common stock, while Series C preferred stock will automatically convert upon the achievement of certain trigger events related to receipt of antitrust clearance under the Hart Scott Rodino Act and the charter amendment. The Company will provide customary shelf and piggyback registration rights to each of the Investors. Additionally, Liberty will also have the ability to request an underwritten shelf take-down and block trade rights.

Timing and Approvals

The transaction is expected to close on or around Monday, March 11, 2024, subject to the satisfaction of certain closing conditions, receipt of any regulatory approvals required in connection with the new roles of Mr. Otting and Mr. DiNello, and the filing of a supplemental listing application required to authorize for listing on the New York Stock Exchange the shares of common stock issued under each investment agreement and to be issued upon the conversion of shares of the preferred stock issued under the investment agreements.

New York Community Bancorp gets $1B investment from Mnuchin-led investor group NYCB) | Seeking Alpha

/C O R R E C T I O N — New York Community Bancorp, Inc./ | Seeking Alpha

- 03/06/2024 – Jerome Powell Says Fed on Track to Cut Interest Rates This Year – WSJ

Fed chair characterizes last year’s inflation slowdown as notable and widespread

Brisk inflation and hiring data in January haven’t altered the Federal Reserve’s expectation that it will be appropriate to cut interest rates later this year, but Chair Jerome Powell said officials want more evidence that inflation is slowing.

Rate cuts won’t be warranted until officials have “gained greater confidence that inflation is moving sustainably” toward the central bank’s 2% goal, Powell told the House Financial Services Committee on Wednesday during the start of two days of testimony on Capitol Hill.

“We want to see a little bit more data so that we can become confident,” Powell said. “We’re not looking for better inflation readings than we’ve had. We’re just looking for more of them.”

Powell told lawmakers the central bank was focused on supporting economic conditions that would keep bringing inflation down while maintaining solid growth and a healthy labor market, achieving what is called a soft landing.

“We are on a good path so far to be able to get there,” he said. Powell also said he saw “no reason to think” that the U.S. economy faces an immediate risk of falling into a recession.

On Wednesday, Powell characterized the recent slowdown in inflation as both notable and widespread, an indication the rise in January prices hadn’t changed the Fed’s outlook that inflation will continue to slow this year.

Soft Landing Achieved? Don’t Ask the Pilot (wsj.com)

If the Fed somehow lands this plane, don’t expect the captain to make an announcement.

“We’re just going to keep our heads down and do our jobs. We wouldn’t be declaring victory like that,” Fed Chair Jerome Powell said Wednesday under questioning from a Democratic lawmaker who encouraged the central bank to come out and say it had achieved a soft landing—if and when the economy might achieve such a state.

“Will there be some announcement at some point that we’ve had a soft landing?” said Rep. Al Green (D., Texas).

“I don’t think by us, no,” replied Powell, who waded through a delicate series of election-year questions during three hours of testimony before the House Financial Services Committee without making much news on monetary policy. Powell is set to return to Capitol Hill tomorrow to answer questions before the Senate Banking Committee.

Transcript: Fed Chief Jerome Powell’s Postmeeting Press Conference – WSJ

Transcript_ Fed Chief Jerome Powell’s Postmeeting Press Conference – WSJ- pdf file

- 03/05/2024 – The Problem Isn’t Big Banks—It’s Banks Getting Bigger – WSJ, Going from a midsize lender to a larger one comes with regulatory and other challenges

NYCB doesn’t share key characteristics of banks that were at the heart of last year’s crisis sparked by Silicon Valley Bank’s collapse, such as huge potential losses on bonds and reliance on uninsured, and thus more skittish, deposits. NYCB, as of the third quarter last year, reported no “held-to-maturity” securities in its portfolio, and as of an early February update, said nearly three-quarters of its deposits were insured or collateralized

But it did make recent jumps in asset size and is facing accompanying changes in its regulatory status. NYCB went from $90 billion in assets at the end of 2022 to over $110 billion as of its latest report. Last year it took on some of the assets and liabilities of seized Signature Bank from the Federal Deposit Insurance Corp.

With this growth, it crossed the threshold to become what is known in regulatory terms as a Category IV banking institution. Toward the end of 2022 it had completed its acquisition of Flagstar Bancorp, which brought its total assets up to $90 billion at the end of 2022 from $63 billion in the third quarter of that year.

NYCB said in January that a jump in loan-loss reserve levels in the fourth quarter of 2023 made it better aligned with “relevant bank peers, including Category IV banks.” The bank also said the cut to its dividend announced in January would “accelerate the building of capital to support our balance sheet as a Category IV bank.”

explanation on hold-to-maturity

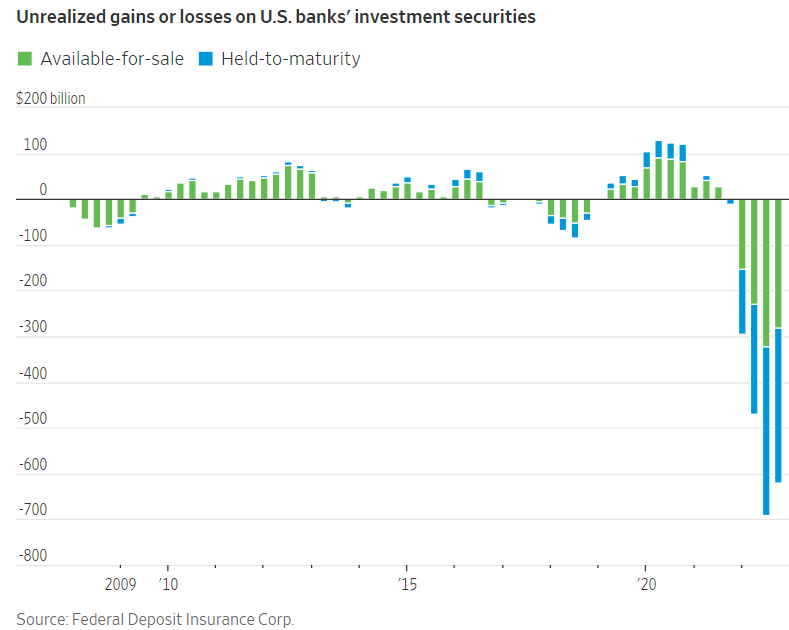

As Interest Rates Rose, Banks Did a Balance-Sheet Switcheroo – WSJ (Lenders pledged to hold on to money-losing bonds, allowing them to avoid reporting losses)

The Wall Street Journal identified six large U.S. banks including Charles Schwab Corp. SCHW 0.71%increase; green up pointing triangle and PNC Financial Services Group Inc. PNC 2.07%increase; green up pointing triangle that together switched the classifications on more than $500 billion of their bond investments last year. For some banks, excluding the unrealized losses from their balance sheets allowed them to report robust levels of capital when in reality their assets were worth much less.

- 03/05/2024 – These Are the 6 Bank Stocks in Warren Buffett’s Portfolio: Should You Invest? (msn.com)

Warren Buffett’s Berkshire Hathaway released its much-anticipated earnings and annual letter to shareholders on February 24. The conglomerate’s earnings were a record, reporting $37.4 billion full-year operating profit, and the conglomerate is now sitting on an all-time high of $167.6 billion in cash and equivalents.

Of note, Berkshire significantly increased its weighting in financial services stock, which could indicate a view that interest rates have hit their highs for this cycle and that the Federal Reserve will lower rates sooner rather than later, as GOBankingRates previously reported.

And Berkshire’s 10Q filing for the third quarter of 2023 indicated an unexplained purchase of $1.2 billion of “banks, insurance, finance” stocks, according to David Kass, Clinical Professor of Finance at University of Maryland, Robert H. Smith School of Business.

1. American Express: 20.6% stake

2. Ally Financial: 9.6% Stake

3. Bank of America: 13% Stake

4. Capital One: 3.3% Stake

5. Citigroup: 2.9% Stake

As we were sitting around the pool on Saturday, one of the guys said he thinks that banks adopting blockchain technology will lead to lower costs and higher margins over time.

That’s an interesting theory… so I immediately e-mailed my banking expert friend (about whom I wrote extensively recently – see my e-mails from January 30, January 31, February 1, February 2, February 6, February 7, and February 8) to ask for his opinion.

He was kind enough to allow me to share it – here’s what he e-mailed back to me:

I’d say there can be modest benefits in terms of operational efficiencies with record keeping, compliance/fraud prevention, and potentially benefits with the speed and cost of certain types of payments.

There are some industries related to banking where blockchain could be a massive disruptor – take title insurance for example. This is a large cost in a home purchase that could be virtually eliminated with blockchain record keeping and tracking of historical data. Auto purchases (and associated title transfers) are another area that could be significantly improved.

However, at the end of the day, margins in the banking sector are going to be predominantly driven by interest rates, credit losses, and competition. The more efficient technology makes the banking sector, the more competitive it could get. For example, think how easy it is now to move money from one bank to the next – this has led to the massive increase in deposit competition which is likely to continue, causing bank funding costs to go higher.

As he concluded:

There are definitely some benefits of blockchain and related technologies, but I’m not sure it is a significant game changer for the banking sector given the competitive dynamics and other major factors (like interest rates) that will drive the sector’s performance.

The downgrade could trigger contractual obligations from business clients of NYCB who require the bank to maintain an investment grade deposit rating, according to analysts who track the company. Consumer deposits at FDIC-insured banks are covered up to $250,000.

New York Community Bancorp’s credit grade was cut to junk by Fitch Ratings, and Moody’s Investors Service lowered its rating even further, a day after the commercial real estate lender said it discovered “material weaknesses” in how it tracks loan risks.

Fitch downgraded the bank’s long-term issuer default rating to BB+, one level below investment grade, from BBB-, according to a statement Friday. Moody’s, which cut the bank to junk last month, lowered its issuer rating to B3 from Ba2.

The bank’s discovery of weaknesses “prompted a reconsideration of NYCB’s controls around adequacy of provisioning, particularly with respect to its concentrated exposure to commercial real estate,” Fitch said.

The bank’s announcement Thursday that it needs to shore up loan reviews reignited investor concern about the firm’s potential exposure to struggling commercial-property owners, including New York apartment landlords. The stock plunged 26% Friday, even as the company said it doesn’t expect that control weaknesses will result in changes to its allowance for credit losses.

“Moody’s believes that NYCB may have to further increase its provisions for credit losses over the next two years because of credit risk on its office loans,” the credit rater said in a statement. It also pointed to “substantial repricing risk on its multifamily loans.”

NYCB’s stock ended the week at $3.55, bringing its decline this year to 65%.

“The company has strong liquidity and a solid deposit base,” Chief Executive Officer Alessandro DiNello, who took over this week, said in a statement earlier Friday. “I am confident we will execute on our turnaround plan to deliver increased shareholder value.”

A month after shaking the regional bank industry with a surprise provision for loan losses, New York Community Bancorp rattled nerves again by announcing a $2.4 billion December quarter earnings hit. At the same time, it said it identified “material weaknesses” in its loan review process and abruptly changed CEOs—causing its stock to tumble.

Of most immediate concern is whether the bank’s run of disconcerting news will contribute to a run by its core depositors, Wedbush analyst David Chiaravini told Barron’s Friday. The bank has previously said it has access to plenty of brokered deposits, but said nothing about deposit levels in Thursday’s announcement. Chiaravini is one of the few analysts who’s been right on NYCB NYCB -25.89% stock, downgrading it to a Sell last year.

The bank said it needs more time to file its annual report. In a securities filing, it said that while its review of internal controls continues, it expects to report that its disclosure controls and procedures and internal control over financial reporting weren’t effective as of Dec. 31. The weaknesses resulted from ineffective oversight, risk assessment, and monitoring activities, it said.

Of most immediate concern to the bank’s fortunes are its flow of deposits, Wedbush analyst Chiaravini said, and the bank said nothing on that score in its recent announcements. He hopes to get more information when the bank finally files its 10-K, which it has promised to do within the next 15 days.

When DiNello spoke with analysts last month, he said that deposits had grown by $1 billion since the year began, and that NYCB could acquire plenty more, in the form of brokered deposits.

DiNello didn’t say at the time how much of that $1 billion were regular customer’s ”core” deposits and how much was brokered, Wedbush’s Chiaravini points out. Banks must pay higher rates to get brokered deposits, making them more expensive than core deposits. Replacing core deposits with brokered ones would hurt NYCB’s net interest margin and its earnings, the Wedbush analyst says.

And NYCB’s funding costs are already under pressure because credit-rating firms downgraded its debt rating last month to junk status.

Given the bank’s admission that its loan reviews were weak, the new executives may review NYCB’s portfolio and regrade loans in a way that would require new reserves and further charges beyond the half-billion dollar reserve boost that set off the bank’s spiral, on Jan. 30.

“That fresh pair of eyes could lead the bank to take a more conservative tack,” said Chiaravini,” and more reserve building.”

Regional Bank Stocks Drop on NYCB News. It’s More Caution Than Fear. – Barron’s (barrons.com)

Treasury Secretary Janet Yellen said last month that “regional banks have concentrations of commercial real estate lending” and “office properties in some cities are of special concern because vacancy rates have increased.” Yellen is chair of the Financial Stability Oversight Council.

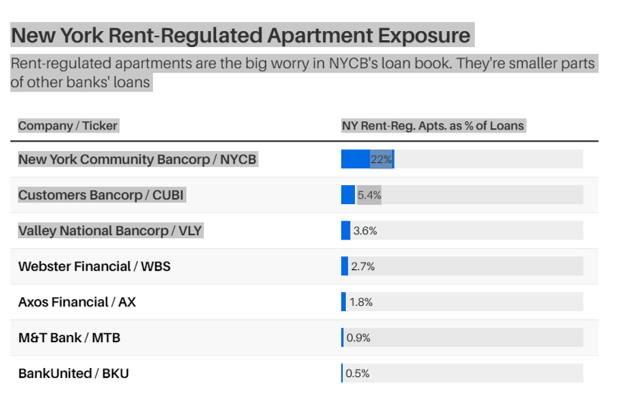

Wedbush analyst David Chiaverini recognized NYCB’s problems early and downgraded the stock to a Sell last year. In a Friday note, he looked at other banks’ exposures to rent-regulated borrowers in New York. His table, reproduced below, shows that NYCB’s loan book is far more exposed than other lenders.

“NYCB’s problems are mostly idiosyncratic to itself, because of its outsize exposure to rent-regulated multifamily loans,” says Chiaverini. “But as long as interest rates remain elevated, commercial real estate will be a headwind to these banks, when their borrowers need to refinance.”

Bank stocks dropped Friday, led by a 23% decline in

, after more signs of trouble at that lender and a smaller peer revived fears about the stability of the sector a year after a string of high-profile failures.

NYCB disclosed late Thursday that management had identified “material weaknesses” in internal controls related to the way it monitors and assesses risk in its loan books. Those loans have been under scrutiny because of the bank’s high exposure to commercial real estate that has fallen in value.

“That language is particularly troubling,” said Steve Moss, a director at Raymond James. “That creates a lot of risk and uncertainty.”

Hours before the disclosure, a deal to shore up a smaller regional bank based in Philadelphia collapsed after the bank revealed its own internal-control issues. That bank, said earlier this week its auditor had found “material weaknesses” in its controls at the end of 2022, including for key credit measures.

“There’s going to be a world of hurt in 2024,” said Leo Leyva, co-chair of the litigation, real estate and real estate special opportunities at Cole Schotz.

Still, bankers and regulators have said depositors aren’t panicking this year and there is less reason to fear a widening crisis.

Wall Street worries about NYCB’s loan losses and deposit levels (cnbc.com)

NYCB Downgraded to Junk by Fitch, as Moody’s Goes Even Deeper (yahoo.com)

New York Community Bancorp’s credit grade was cut to junk by Fitch Ratings, and Moody’s Investors Service lowered its rating even further, a day after the commercial real estate lender said it discovered “material weaknesses” in how it tracks loan risks.

Fitch downgraded the bank’s long-term issuer default rating to BB+, one level below investment grade, from BBB-, according to a statement Friday. Moody’s, which cut the bank to junk last month, lowered its issuer rating to B3 from Ba2.

The bank’s discovery of weaknesses “prompted a reconsideration of NYCB’s controls around adequacy of provisioning, particularly with respect to its concentrated exposure to commercial real estate,” Fitch said.

The bank’s announcement Thursday that it needs to shore up loan reviews reignited investor concern about the firm’s potential exposure to struggling commercial-property owners, including New York apartment landlords. The stock plunged 26% Friday, even as the company said it doesn’t expect that control weaknesses will result in changes to its allowance for credit losses.

“Moody’s believes that NYCB may have to further increase its provisions for credit losses over the next two years because of credit risk on its office loans,” the credit rater said in a statement. It also pointed to “substantial repricing risk on its multifamily loans.”

NYCB’s stock ended the week at $3.55, bringing its decline this year to 65%.

“The company has strong liquidity and a solid deposit base,” Chief Executive Officer Alessandro DiNello, who took over this week, said in a statement earlier Friday. “I am confident we will execute on our turnaround plan to deliver increased shareholder value.”

- 02/29/2024 NYCB stock slides after disclosing $2.4B charge, CEO replacement (NYSE:NYCB) | Seeking Alpha

the company completed its goodwill impairment assessment on Feb. 23, it noted. With GAAP accounting requiring a goodwill impairment charge for Q4 2023, NYCB recorded a $2.4B hit to Q4 and annual earnings linked to the value of transactions prior to the 2008 financial crisis. The impairment charge did not result in any current cash expenditures, nor does it have any impact on the company’s regulatory capital ratios.

And, in navigating the turmoil, the regional bank said in a separate release that Alessandro DiNello, has been named its CEO and president, after serving as executive chairman for less than a month to help the bank improve business operations.

- 02/26/2024 – is the market top?

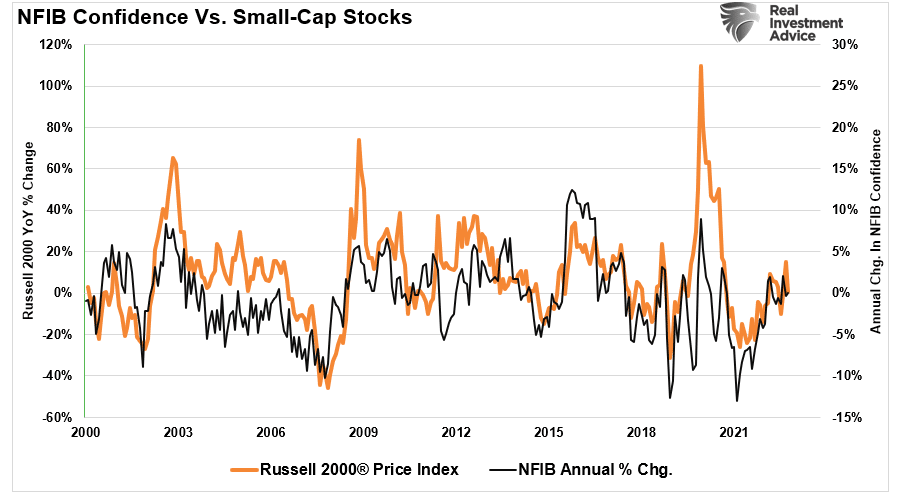

02/25/2024 – Small-Cap Stocks May Be At Risk According To NFIB Data | Seeking Alpha

- Retail investors have started chasing small-cap stocks in hopes of a rate cutting cycle by the Fed and avoiding a recession.

- The primary economic data points continue to be very robust. Low unemployment, strong economic growth, and declining rates of inflation.

- There are risks to assuming a solid economic and employment recovery over the next couple of quarters.

The hope of a “catch-up” trade as a “rising tide lifts all boats” is a perennial bet by investors, and as shown, small and mid-cap stocks have indeed rallied with a lag to their large-capitalization brethren.

However, some issues also plague smaller-capitalization companies that remain. The first, as noted by Goldman Sachs, remains a fundamental one.

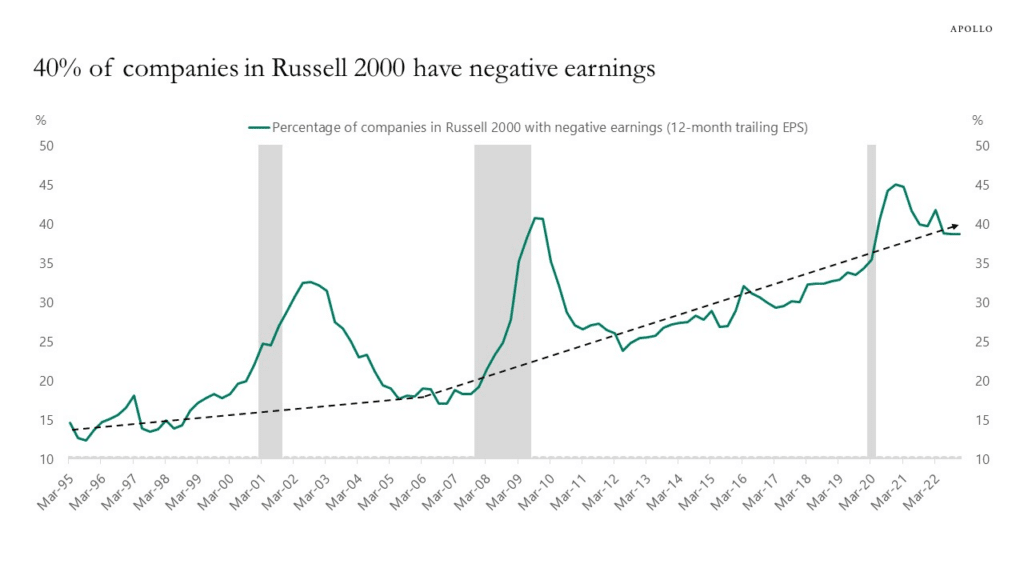

“I’m surprised how easy it is to find someone who wants to call the top in tech and slide those chips into small cap. Aside from the prosect of short-term pain trades, I don’t get the fundamental argument for sustained outperformance of an index where 1-in-3 companies will be unprofitable this year.”

As shown in the chart by Apollo below, in the 1990s, 15% of companies in the Russell 2000 had negative 12-month trailing EPS. Today, that share is 40%.

Besides the obvious that retail investors are chasing a rising slate of unprofitable companies that are also heavily leveraged and dependent on debt issuance to stay afloat (a.k.a. Zombies), these companies are susceptible to actual changes in the underlying economy.

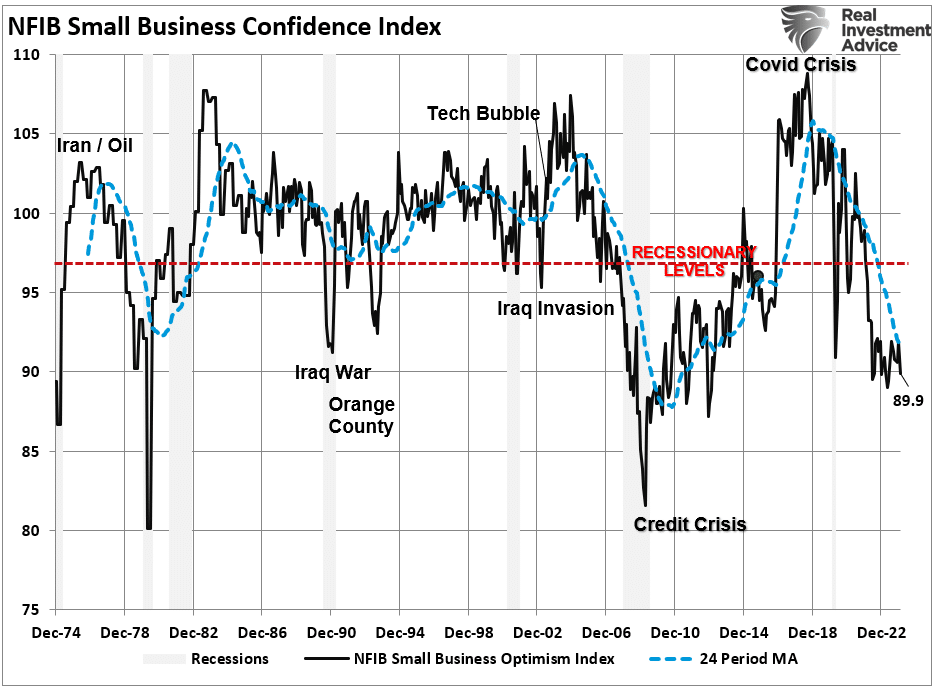

So, is there a case to be made for small and mid-capitalization companies in the current environment? We can turn to the National Federation of Independent Business (NFIB) for that analysis.

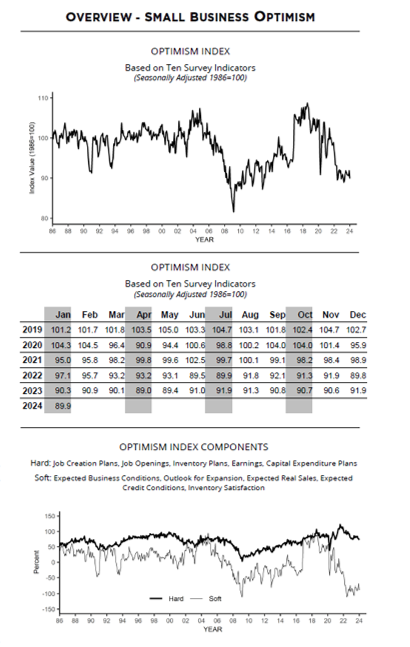

For example, despite government data that suggests that the economy is strong and unlikely to enter a recession this year, the NFIB small business confidence survey declined in its latest reading. It remained at levels that have historically been associated with recessionary economies.

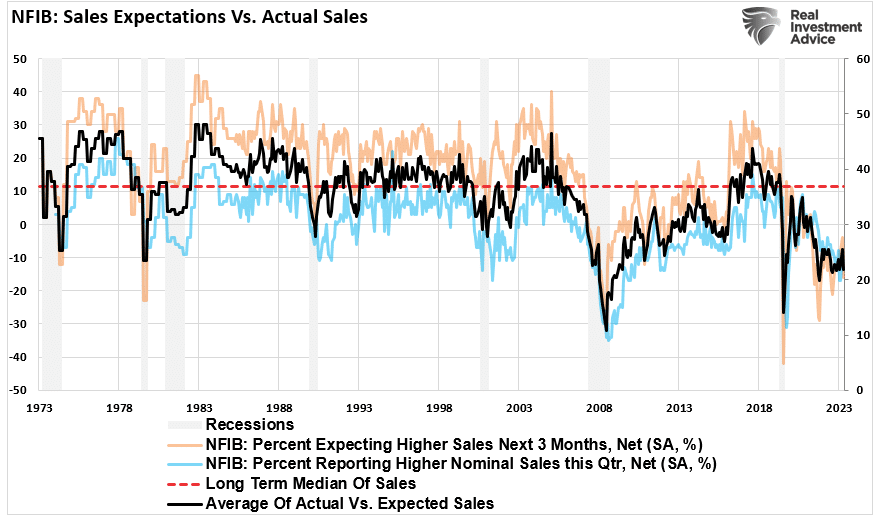

Unsurprisingly, selling a product, good, or service drives business optimism and confidence. If consumer demand is high, the business owners are more confident about the future. However, despite headlines of a strong consumer, both actual and expected sales by small businesses remain weak.

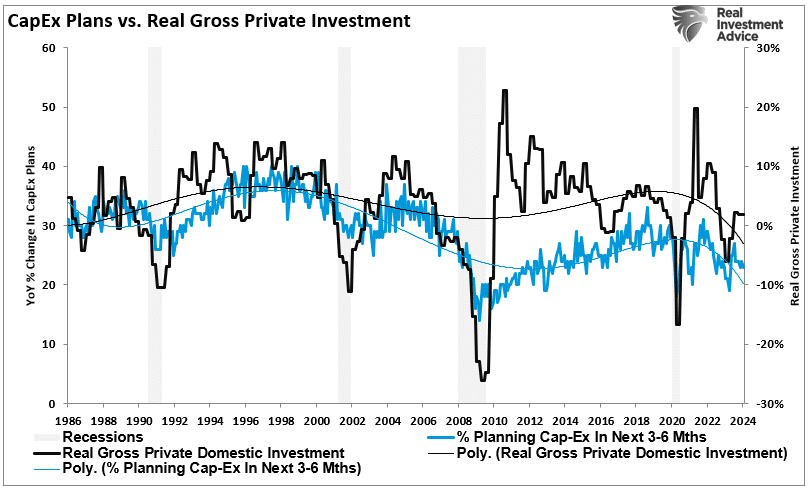

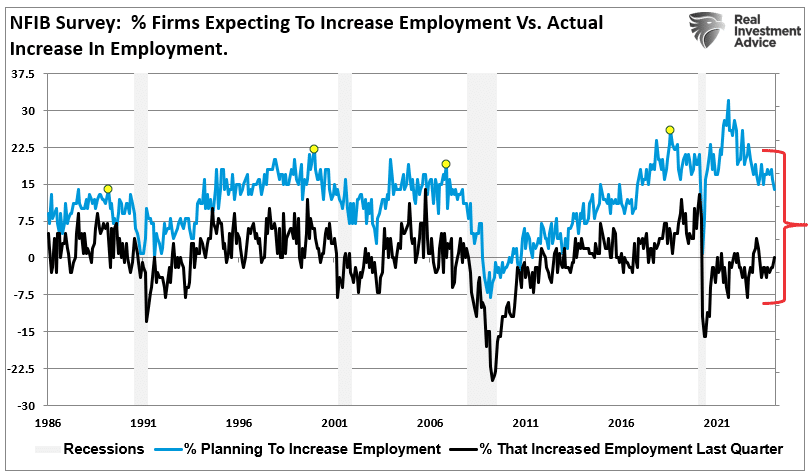

Furthermore, if the economy and the underlying demand were as strong as recent headlines suggest, the business would be ramping up capital expenditures to meet that demand. However, such is not the case regarding capital expenditures and actual versus planned employment.

There is an essential disconnect between reported economic data and what is happening within the economy. Of course, this brings us to whether investors are making a mistake by betting on small-capitalization stocks.

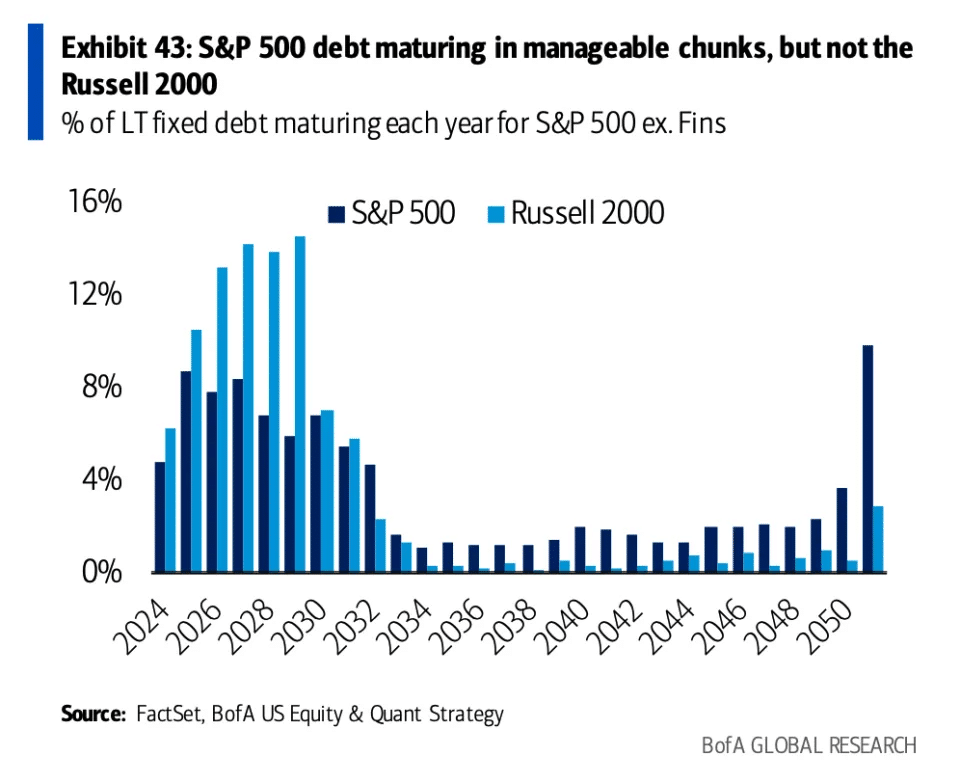

Unlike many companies in the S&P 500 that refinanced debt at substantially lower rates, many of the Russell 2000 were unable. If interest rates are still elevated when that “debt wall” matures, refinancing debt at higher rates could further impair profitability.

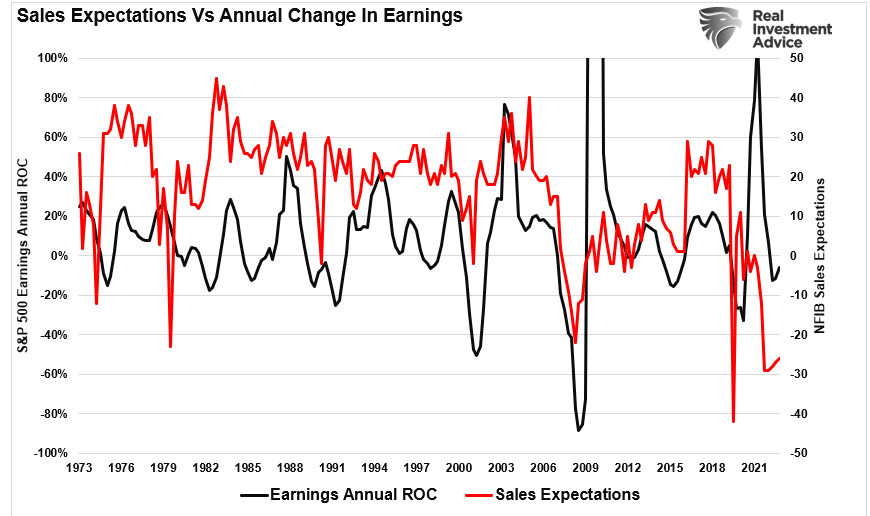

Furthermore, the deep decline in sales expectations may undermine earnings growth estimates for these companies later in the year.

Of course, there are arguments for investing in small-cap stocks currently.

- The economy could return to much more robust rates of growth.

- Consumer demand could increase, leading to stronger sales and employment outlooks for companies.

- The Federal Reserve could cut interest rates sharply ahead of the debt refinancing in 2024.

- Inflation could drop sharply, boosting profitability for smaller-capitalization companies.

Confidence Matters

Yes, any of those things are possible. If they emerge, such should quickly reflect in the confidence of businesses surveyed by the NFIB. As shown, there is a high correlation between the annual rate of change of NFIB small business confidence and the Russell 2000 Index.

The apparent problem with the wish list for small-cap investors is that more substantial economic growth and consumer demand will push inflationary pressures higher. Such would either keep the Federal Reserve on hold from cutting rates or lead to further increases, neither of which are beneficial for small-cap companies. Lastly, the surge in economic growth over the last two years resulted from a massive increase in government spending. It is unlikely that the pace of the expenditures can continue, and as monetary supply reverses, economic growth will continue to slow.

detailed information on NFIB index, Small Business Economics Trends | NFIB (SBET-Jan-2024)

- 02/15/2024 – Soros ups stake in NY Community Bancorp as stock claws back from 27-year lows – MarketWatch

New York Community Bancorp’s stock rose Thursday, outpacing gains in other financial stocks, a day after Soros Fund Management disclosed an increased stake in the hard-hit regional bank.

Soros Fund Management acquired 1,036,180 shares of New York Community Bancorp to bring its stake up to just under 1.48 million shares, according to a filing made after Wednesday’s market close.

The sector is plagued by poor performing commercial real estate assets, recent bank failures, and expensive deposits. For this sector, I prefer the large-cap names that pay less for cash deposits, have less office space exposure, and actually benefited from the recent bank collapses as they grew their customer base after the fallout. As a result, I am maintaining my cautious outlook on KRE, and urge my followers to consider any positions in this fund very carefully as we navigate 2024. – more bank failure can come at any time which will give another buy in opportunity, and this process might on going for a couple of years

- The article evaluates the SPDR S&P Regional Banking ETF as an investment option at its current market price.

- Regional banks had a volatile year in 2023 and finished the year with a strong Q4. I am not buying the recent bullishness and see big headwinds clouding the investment case.

- I have been cautious on this theme and saw limited potential for KRE, which has been proven right in hindsight. This outlook is still my base case for the year ahead.

KRE has been a weak spot. Even with its run-up since late last year, this fund is dramatically under-performing the broader market. At first glance this could look like a buying opportunity – and I would understand that sentiment. However, I see a number of different headwinds that make me reluctant to put down my hard earned cash with this equity play.

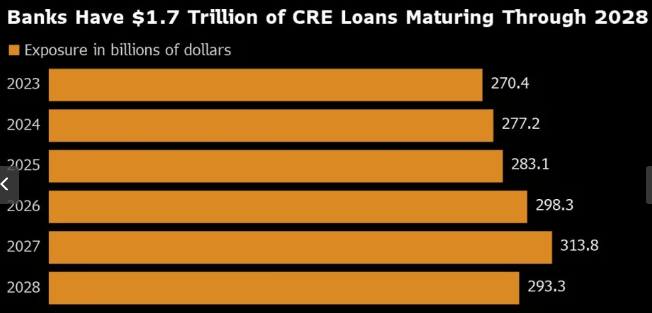

The Commercial Real Estate Headwind

regional banks hold a big percentage of the total amount of the $1.7 trillion in commercial real estate debt held by US banks as a whole that is coming due in each calendar year this decade:

Commercial Real Estate Debt (Bloomberg)

This means that the margins and profits of US banks large and small are impacted by the performance of these loans. Throughout 2023, this has not been a good thing, as regional banks like Silicon Valley Bank and First Republican bank failed.

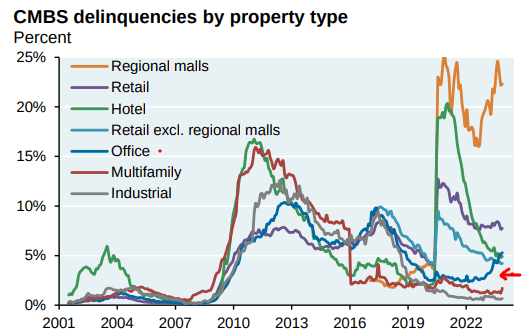

Looking ahead, this is a headwind that is impacted by multiple factors. One, as interest rates rise, this is pressuring the property values over commercial buildings, as well as other real estate assets. For office space in particular, vacancy rates have risen substantially. This means that values are dropping for two reasons – higher cap rates and also the fact that demand is down. This is not unique to commercial real estate by any means, as regional malls and retail space is also seeing an uptick in vacancy rates. But the acceleration of the office space vacancy rate in the near term is my big concern:

Delinquency Rates by Sector (JPMorgan Chase)

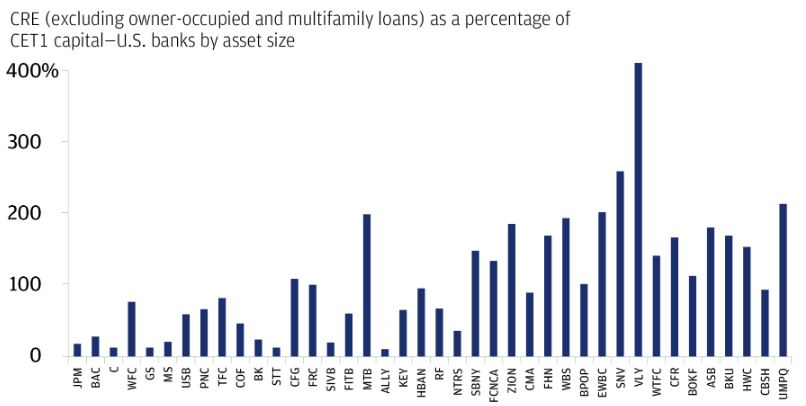

This is raising solvency risks for potentially hundreds of US banks, but as mentioned above, it has a disproportionate impact on smaller (regional ones). This is critical to understand because I am not a “bear” on the Financials sector in total. But for me if I want banking sector exposure, I will focus on the large-cap names rather than the regionals. Part of this determination was made because smaller banks are more exposed (as a percentage of total assets) to the woes of the commercial real estate sector than their large-cap peers:

CRE Exposure (By Bank) (Federal Reserve)

As you can see, with the exception of Wells Fargo (WFC), the largest banks have minimal exposure to this sector. Meanwhile, the regionals (at the far right of the chart) have substantial exposure here. I believe this is a major problem in 2024 because I see these challenges remaining top of mind and probably getting worse, not better. Even if interest rates decline they will be elevated for the first half of the year and office delinquencies are not going to suddenly reverse.

This is one of the key reason XLF reaches all time high, KRE is still quite low.

Banks Are Preparing For Losses

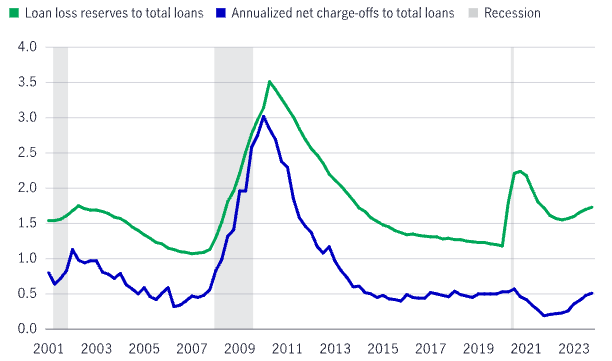

To start with, I want to illustrate that while declining real estate values are a major pain point, they are unlikely to cause more widespread panic. I see Silicon Valley and First Republic as exceptions, not the rule, and believe even smaller, regional lenders are prepared to handle some volatility in this space. The reason for this belief is that the banking sector has ramped up loan loss provisions aggressively in 2023 (on the backdrop of those bank failures). What this looks like in practice is that while charge-offs (losses) are on the rise, banks are capitalized well enough to absorb these losses:

Reserves & Net Charge-Offs (US Banks in Aggregate) (FDIC)

What this illustrates to me is that while losses are rising, banks have been anticipating this and should be able to handle it relatively smoothly. That is central to why I am not an outright bear on this sector – or the individual companies that underlie KRE’s portfolio.

However, just being able to “absorb” losses is not a real enticing investment case. I am differentiating from the fact that these companies can manage this environment against being a fundamentally strong buy argument. Will regional banks go bust because of commercial real estate loans? Based on their preparedness, it doesn’t seem likely. But not going bust isn’t how we find “alpha” – we find it some compelling growth stories. I don’t see that being the case here, so I want to manage expectations on how good this metric really is.

Priced For Trouble

I bring this up because KRE is priced quite cheaply. Looking at the current P/B and P/E ratios, I see a fund that has some bad news baked in:

Current Valuation Metrics (KRE) (State Street)

This is clearly much cheaper than the broader market (as measured by the S&P 500) and should limit some downside if market or sector volatility picks up going forward. While I think this cheapness is warranted to a degree and I don’t see this as a “value opportunity”, I would emphasize this is not an expensive sector to own. For a contrarian thinker who is more optimistic than me on the opportunity for regional banks in 2024, this valuation metric could be enticing. In my view, I don’t want to get sucked into buying struggling companies just because they appear cheap, but that is a subjective argument. Others may draw a different conclusion and it is important to give this metric some consideration.

Banks Now Want Lower Rates?

Another important headwind from 2023 that continues to this day is the fact that regional banks have seen their deposit costs rise as a result of higher benchmark rates from the Fed. While initially higher interest rates were seen as a good thing – and they were – some of that effect is wearing off with year-over-year comparisons getting difficult to beat.

What I mean is, as rates stayed high, regional banks were forced to increase what they paid in interest to draw in deposits. While large-cap banks kept deposit rates quite low, regional banks have to compete more aggressively for customers. But, simultaneously, the levels they were able to charge for loans hit a ceiling. The regional failures discussed earlier accelerated this upward deposit re-pricing activity as smaller institutions had to convince customers their deposits were safe – and pay them more to convince them!

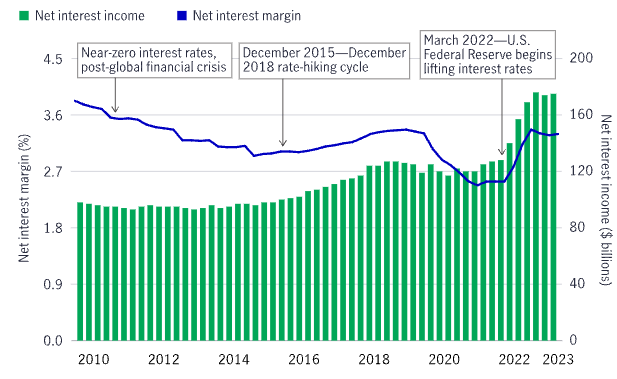

The net result of this is that now regional banks are actually hoping for the Fed to cut rates so they can begin to pay less to hold deposits. This is a far cry from the days when investors (and bank executives) were looking forward to higher rates because net margins would improve. While that initially did happen, margins have plateaued as I mentioned:

Net Income and Margin for US Banks (Aggregate) (Goldman Sachs)

This is why earnings reports haven’t excited investors. There has been an acceleration in costs related to layoffs, FDIC insurance, and deposits, but at the same time margins are stagnating due to credit losses and loan-interest ceilings. Similar to the credit loss provision metric I mentioned previously in this review, this is not an investment story that I can get behind.

And this is not just my opinion. During M&T Bank’s (MTB) fourth quarter earning’s call last week, CFO Darryl Bible was quoted:

Its CFO, Daryl Bible, told analysts that lower rates would help its commercial lending and investment banking businesses.

I get kind of excited, if the Fed just lowers rates just a little bit”

Source: M&T Bank Earnings Conference Call

My conclusion from all this is one that lacks confidence. We heard for years about how banks would perform well and generate alpha as soon as rates went up. Now, with an elevated rate environment, banks are under-performing the S&P 500 and the message from executives is that things will improve once rates go down. It is contradictory at best, and leaves me searching for a better sector to put my investment dollars to work.

Bottom-line

Regional banks, and KRE by extension, are up strongly from late October lows. The market has begun to price in rate cuts this year on the tide of declining inflation and resilient economic growth. Some analysts believe this will disproportionately benefit regional banks, but I have my doubts.

The sector is plagued by poor performing commercial real estate assets, recent bank failures, and expensive deposits. For this sector, I prefer the large-cap names that pay less for cash deposits, have less office space exposure, and actually benefited from the recent bank collapses as they grew their customer base after the fallout. As a result, I am maintaining my cautious outlook on KRE, and urge my followers to consider any positions in this fund very carefully as we navigate 2024.