study of SPG

- 11/22/2020 – time to come back to SPG? Simon stock is down 46% this year

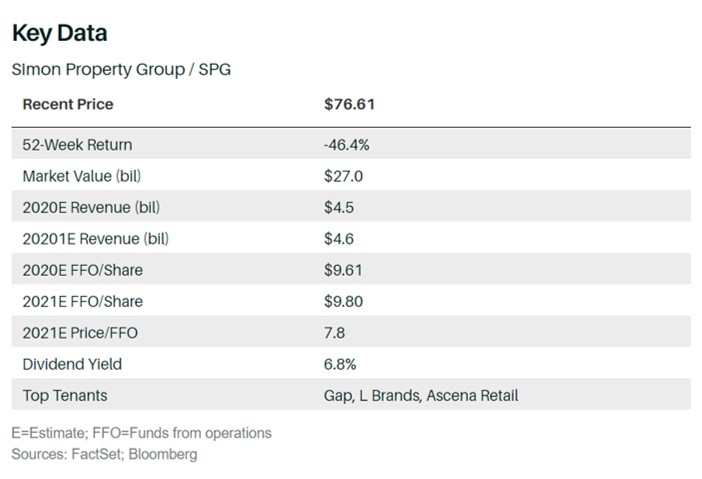

The Mall Isn’t Dead. Why It’s Time to Buy Simon Property Stock

With coronavirus cases soaring, retailers suffering, and local officials slowing or halting business reopenings across the U.S., it might seem like an odd time to invest in luxury shopping malls.

That’s what makes Simon Property Group (ticker: SPG), the largest mall operator in the U.S., worth a closer look. Simon might come through the pandemic in surprisingly good shape. It’s using its unusual financial strength to buy both other mall operators, like Taubman Centers (TCO), and tenants, such as bankrupt apparel retailers Brooks Brothers and Lucky Brand, which will operate in its key malls.

The stock is deeply discounted and is trading at about half the valuation of other mall real-estate investment trusts. And it has a dividend that yields almost 7%.

Piper Sandler’s Alexander Goldfarb says credit trends and rent payments are improving, and recent vaccine news makes Simon “among the top winners” of stocks he covers. “While tenant credit remains a concern, the winds are blowing in SPG’s favor.”

Still, recent trends are bleak, as the pandemic again hits in-person shopping. Third-quarter profit and revenue disappointed Wall Street, with net income plunging 73% from the level a year earlier. Simon stock is down 46% this year, compared with the 11% gain in the S&P 500 index. But the shares spiked on news of the revised terms for Taubman and successful vaccine tests.

But David Simon told analysts that he expected the investments, and others like them, to be worth $1 billion over time, with a minimal outlay of capital—he said $50 million. There aren’t deals like them on the immediate horizon, he added, but that doesn’t rule out future investments.

Once the coronavirus is tamed, people will again shop in stores, attend movies, and eat in restaurants—all things offered at Simon malls. Until then, the nearly 7% dividend yield is “one heck of a great cash flow” for investors, Smead says.

Simon has weathered the crisis, David Simon told analysts, noting, “We’re pleased with the cash flow we’re generating…I want to thank my colleagues for busting their hump, and things are looking up.”

- 08/11/2020 – another great idea of using malls

Grocery stores might be the next big thing to move into malls

- The biggest mall owner in the U.S., Simon Property Group, hints at opening more grocery stores in its malls.

- CEO David Simon said about working with more grocers: “Yes, I am hopeful that we can certainly do more business with that category.”

- He also noted that retailers are recognizing the benefit of using their stores to help fulfill online orders.

- 08/10/2020 – positive news for mall business, need more time to study

Simon shares jump on reported talks with Amazon. But converting stores to warehouses may face hurdles

- Shares of Simon Property Group jumped Monday following a report that said the biggest U.S. mall owner is in talks with Amazon to turn shuttered Sears and J.C. Penney stores into warehouses, as it looks to salvage vacant space at its properties and collect more rent.

- Simon is set to report earnings after market close.

- Real estate analysts say a deal with Amazon could be positive for Simon in the near term, but there would be hurdles.

Mall owners like Simon, in turn, are scrambling to find new uses for retail space when few retailers are still growing. The Covid-19 pandemic has only exacerbated challenges, by hurting movie theaters, entertainment venues, gyms, co-working facilities and restaurants. These types of businesses had, up until recently, been considered alternative uses for retail space, by Simon and other mall operators.

“In this environment, it will be difficult to fill boxes of that size in the short-term,” said Joseph Malfitano, founder of turnaround and restructuring firm Malfitano Partners. “A deal with Amazon provides a quick fix as these locations would likely need to subdivided, which would take time and money.”

Another potential obstacle would be how a mall property is zoned by local governments.

Warehousing is considered an industrial use, not a commercial one. This means the former department stores may need to be rezoned, and the surrounding community and other retailers and restaurants at the mall might not welcome the change. Another factor would be the number of trucks and traffic in and out of mall parking lots, especially overnight, analysts said.

An Amazon warehouse could also bring in less rent per square foot than a typical department store tenant would. Warehouses typically pay between $5 to $10 per square foot in rent, whereas department stores can pay closer to $20, Sandler O’Neill + Partners real estate investment trust analyst Alexander Goldfarb said.

But right now, “any community wants tax revenues … malls are huge tax drivers to the community,” Goldfarb said.

The dire situation that the coronavirus pandemic has inflicted might make a community more willing to accept an industrial tenant moving into the local shopping mall, he said.

Another hurdle for Simon would be co-tenancy clauses, which can be triggered when one or a number of anchor tenants at a mall leave the property. This legal provision essentially gives tenants within the mall power to renegotiate their leases, potentially paying less in rent, when a major department store chain goes dark and traffic drops off.

“A tenant like Amazon … could trip co-tenancy provisions for other tenants, which will also cost landlords money,” Malfitano said.

Regardless, the need for e-commerce fulfillment hubs is clearly spiking across the country, oftentimes outweighing supply in markets, as consumers are buying more and more online.

Demand for industrial real estate could reach an additional 1 billion square feet by 2025, according a July report from the commercial real estate services firm JLL. Prior to the Covid-19 crisis, about 35% of its industrial leasing activity was related to e-commerce, JLL said. But now, as much as 50% of that leasing activity has already been tied to the online retail industry in 2020.

Simon has partnered with rival mall owner Brookfield Property Partners as one of three bidders looking to salvage Penney from bankruptcy, CNBC previously reported. Penney’s lenders have until midnight Tuesday to select a winning bidder, according to court documents.

It is unclear whether Simon Chief Executive David Simon will mention the Penney deal or other potential transactions (including one with Brooks Brothers), during Monday’s earnings conference call. Analysts also are eager to hear how mall rent collections are trending since stores have reopened, and how the real estate company is faring in trying to get out of its deal to buy the high-end mall owner Taubman. It terminated the $3.6 billion transaction in June. But Taubman is still pushing ahead with it.

Simon shares have fallen about 54% this year. The company has a market cap of nearly $21 billion.

- 08/09/2020 – Good for Simons, SHLD and JCP, but might not good enough. Need time to study more in depth

Amazon and Mall Operator Look at Turning Sears, J.C. Penney Stores Into Fulfillment Centers

Hookup between Simon Property Group, Amazon would show how retail and logistics are converging more rapidly